Good Margine Gained!

Good Margine Gained!

Your point is certainly true. There is always a doubt regarding a government company that what will the government do! Just see the oil PSUs!! They had to pay extra taxes for supernormal profits, but all losses are for the company to bear (like the petrol and diesel price freeze causing 20-30k cr losses to ioc/hpcl/BPCL) ![]()

It’s true but at certain point the stock became to undervalued to overlook!! Like when it was quoting at 105-120 range by oct 2022.

It’s dividend has consistently risen and it was quoting at dividend yield of 10 percent at 105 (and 9 percent at 120) which was going to increase further. It was just distributing 25 percent of earnings! Psu or no psu we can see it was strictly better than FD. The same arguments can’t be made today. The dividend yield is 5 percent now, lower than 7.5 percent we can get easily in banks, I am not going to buy it as I am already carrying half the shares I bought at an average of 118

Dear Hitesh,

About a year ago, I read a good article about Abbott India in ET and bought a small quantity. I never expected the share price to jump the way it has. If you look at the sales record of the company, its nothing spectacular, ranges from 5-10% annual growth in most years. Dividend yield at current price is < 1%. So, I cannot fathom why the share price has moved from, 18k to around 23k now, even touching 24k. Is it because of some new proprietary products from the parent’s portfolio to be launched in India? Or is it a case of rising tide lifting all boats? Appreciate if you can provide your perspective.

I believe I’m over-diversified and need to have not more than 10 stocks to properly build wealth.

What makes you say so?

There’s no standard rule. You’ll need to find your own. The first step to finding your answer is to figure out what truly is driving your need to reduce the stocks and how you define over-diversification.

You’ll not find one framework on which every investor agrees. Eventually, everyone customizes their allocation/strategy according to themselves {takes iterations I belive}.

I think its the PSU overhang why many of us missed the bus on this one and even PSU banks. Its more like ‘PSU discount’ rather than ‘value trap’, because these stocks have always sold at a discount to private players, and even today.

It can also be called ‘PSU bias’, we think its normal for a great company to sell at a discount because its a PSU.

But those concerns are legitimate for many of us, even if a PSU is doing well, and the government overhang is a reality.

Even at 270, PFC sells at below one price to book. Will be nice to know how many of us are willing to buy it today.

Last couple months multiple things at personal front have kept me away from market activity.

Although, I kept checking what’s going on but did not have resources to be ready to carry out any buy/sell activity.

I think such detachment has made me realise few aspects and now I feel in between such periods maybe good.

One realization on checking my current portfolio value now is that over last few months, although my portfolio performed better than NIFTY/Sensex but could not beat the BSE Midcap index.

So, HDFC Midcap opportunities growth fund did really well and so would have all other midcap funds as well…

My portfolio specific – No great performances in this current bull run…some major events have been Trent entering Top 5 and United Spirits entering Top 10 at number 8 spot…

I cleaned up quite some trash from my Portfolio few months back when needed some capital for personal needs…Probably that also contributed to getting detatched feeling…

I dont know if this gradually getting detached from being too active is a part of my evolving Investor psyche or it is temporary…I need to really think what strategy & approach I should follow now as I do not feel putting incremental capital in existing names, do not like any new names & neither have inherent discipline within me to do an SIP in Mutual funds…

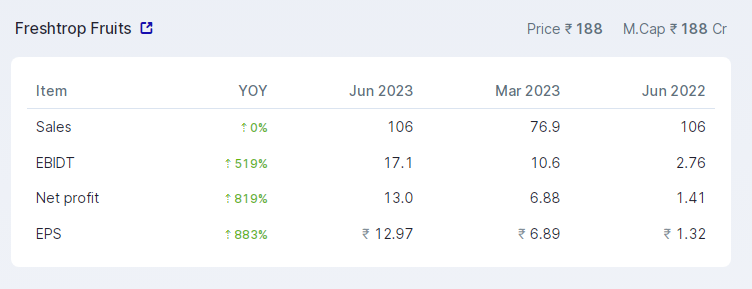

I have been looking at this company as the E-waste news started making buzz.

I believe in the opportunity given the govt push to manufacturers as well as users to better handle E-waste, but not sure if Eco-reco has a right to win here.

There are 10+ organised players.

India’s largest player “Cerebra” has a capacity of 96,000 TPA and holds five ISO certifications for recycling – the only company in Asia to hold all five ISO certifications.

In comparison the company has capacity for just 7,200 TPA with utilisation of ~25%. Further, company is doing a capex to raise capacity.to 25,000 MTPA

Cost of Capex is also not material, company is spending just 50cr.

Notably, there is a definite opportunity for capacity as Frost & Sullivan research notes India has 400 registered e-waste recyclers with an installed capacity of recycling 1.07 mn TPA

India generated 1.6mn tonnes in FY21 which is growing at 27% CAGR.

The other angle that needs to be tested is the falling cost of sourcing. Mgt noted that India is moving towards the Developed market economics where manufacturers pay for the recycling instead of recyclers purchasing E-waste from them. But local scuttle butt indicates kabaddi walas still pay good money for E-waste, so why would these manufacturers start paying to Eco reco?

Let’s revisit this discussion from June 2020. To @smallcapvaluefind analysis of PFC, everyone here was quoting it’s a value trap without understanding the real meaning of value trap (on value pickr at that!!)

Most of us were saying value trap for it because the stock was not moving and now see where it is!! But the fact is that if you just ignore the stock and see the fundamentals, you see a company with a historical 10 year ROE of 16-21 percent which has 5xed its profits in 10 years!! Such a company cant be value trap. A value trap is a company with good looking financials but no growth (or degrowth), which cant make use of the money it earns (might end up being used in things necessary to keep company running!!) and doesn’t give it as dividends either!! Not a company that is doing both, giving dividends and growing its profits!!

The fact is that it was never a value trap at all!! Even those who were stuck in it as a value trap were making 8 percent cagr+ due to dividend alone!! How is that a value trap? And it was also growing fundamentally

Sometimes we miss the obvious growth happening fundamentally because we are stuck seeing a cyclical stock price chart!!

Some shameless self-promotion ![]()

https://twitter.com/Shubham45856917/status/1472918992742277128?s=20

Just went through the Valuepickr forum for Rajest Exports, and the company is shady to a T!!

The financials are good, but how much can be trusted is the question. Please let me know if

I made a mistake in above 3 points.

I had pointed out in my Application that I will be providing research on Indian and US listed equities.

During SEBI interview, I was asked to explain how I am qualified to do research on US stocks and how I am planning to charge for it.

Hope this was helpful, No idea about Crypto.