Yeah Manappuram, Axis and Indus looks compelling to invest in Finance category. Even HDFC Bank and Kotak Bank which have historically managed NPAs well are available at reasonable valuations. I have taken small positions in all of them (except Manappuram, was tracking it at 110-115 to buy, but missed buying it and couldnt make up mind to buy it at 120 seeing it at 110 once!!)

The only issue here is a. I am already overweight on financials, still have half the PFC, b.) Will NPAs start climbing? Loan growth was high, interest rates are high now, perfect receipe for NPAs, but we are not seeing any stress yet.

Posts in category Value Pickr

Deep Value Portfolio (22-08-2023)

Dreamfolks services limited( DFS) (22-08-2023)

Need to consider the fact that mgt commentary has been all over the place.

At the time of IPO, the commentary was gross margins are very stable and business will only compound.

Then the second quarter post listing, margins start to increase and mgt maintains it will be able to maintain these increased margins.

It was Mgt responsibility to point out seasonality in margins in earlier calls itself. Cant be that only in 1Q24 have they realised that there is timing difference as to when lounge operators raise their prices and Dreamfolk will take 2 quarters to pass it on.

The commentary in this call has broken the thesis that Lounge Operators will be price takers and hence Dreamfolks can continue to keep a higher share of the amount paid by Banks.

If there was one-time charges in a quarter, why were they not quantified in that very quarter itself.

Also, when Plaza Premium lounges in Hyderabad, Delhi and Bangalore were shut in November last year (for almost a month), which impacted a significant part of their business, mgt did not inform exchanges. Rather, it was vaguely pointed in earnings call that the quarter was impacted by lounge operator transition.

Deep Value Portfolio (22-08-2023)

Better to evaluate against other options available. There are many relatively quality cos like Manappuram. Even Axis bank is available at 2x P/B and 12x pe. It’s upto each one of us decide what we’re comfortable in the end.

Just wanted to highlight that there may be better opportunities.

Disc : No reco by any means

Nithin’s Portfolio (22-08-2023)

KAMO Paints : I like their revenue Guidance of 1000 crore by FY28 and currently they are doing revenue of 260 odd crores ![]() now investing is the game of probability do weigh your risk and probabilities accordingly.

now investing is the game of probability do weigh your risk and probabilities accordingly.

260 odd crores revenue now with 5x growth in next 5 years in no brainer for me, but again I might be wrong.

Portfolio has come to a size about 22-25 numbers, Whereas i did commit to stay between 10-15 ![]()

SUVEN has 2 molecules in Phase-3 now and likely SUVN-502 may pass the Phase-3 test, if they do then there will be huge runway for Suven. So SUVEN LIFE SCIENCE are into research and SUVEN PHARMA is into CONTRACT MANUFACTURING – so given which side of the coin is much heavier :

Most of the research based companies such as SUVEN LIFE : has demerged from the main company SUVEN PHARMA to value unlock – because the research expense are considered to be expense than asset.

So SUVEN LIFE sciences focuses on research or on contract research

Most of the value unlocking happens on SUVEN PHARMA for manufacturing and distribution.

Nithin’s Portfolio (22-08-2023)

Gentle Note :

The stock is tumbling down so I have cut down my holdings too – I would rather wait for breakout to pick back the stock.

Current Additions :

Mayur Uniquoters

Latent View

Gabriel

Added more to the allocation

DMCC

Orchid

Kamo Paints

Reduced

Sadhana (Waiting for breakout)

Fluorochem ( Waiting for approval & it will take minimum of 2-3 quarters)

Deep Value Portfolio (22-08-2023)

I think Rajesh export is a in Deep value category. its PE is 10.5 (at price of 520 as on today 22/8/23)

SJS Enterprises Ltd (22-08-2023)

Curios to know who is the buyer and the open offer price if 26% has been acquired by single buyer as per SEBI SAST Regulations.

Post this block deal, promoters will be left out with 21.8%. Any chance of hostile takeover by any big group?

Also would appreciate the view of fellow VP members, CNBC TV 18 has reported on August 11 that block deal will happen in SJS very soon (Watch from 1:45 )

https://twitter.com/i/status/1689936636812091392

Is this a price sensitive information which company has to disclose to stock exchanges. Company has also neither denied or accepted this statement of CNBC TV-18. How come such large block deals are getting leaked to media before it comes to public. Is there any CG issue over here?

Nithin’s Portfolio (22-08-2023)

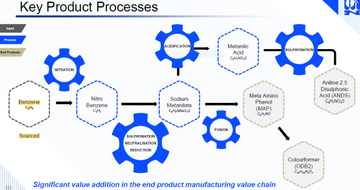

SADHANA NITRO CHEM

STRUCTURAL IMPORT SUBSTITION story, Green Chemistry via Nitro Benzene

PAP Stands for Para-Amino Phenol PAP is the raw material for manufacturing of Paracetamol – You know the Paracetamol is used Pain Relief and Fever.

Opportunity size for PAP :

The World demand for PAP before Pandemic has been at 1,60,000 TPA. Out of which 1,50,000 TPA (i.e. 94% of Total World demand of PAP) is sourced from CHINA. In India, there are players like Valiant Organics who make PAP but its not via Green Chemistry.

Sadhana Nitro got Process Technology using GREENER Technology(that means it is SUSTAINABLE in Future)

PAP Can be Produced using 2 Routes

1.PNCB Route (Valiant Organics exists)

2.NB Route(Sadhana exists)

Sadhana has been Awarded PLI Scheme by Indian Govt for PAP Plants of 36,000 TPA

They have completed all capex on the month of June 2023, and they will start commercial supply soon.

Now Granules is one of their clients and recently promoter has pledged his shares to issue warrants.

Nithin’s Portfolio (22-08-2023)

@manoopatil Chemical stocks are expensive for most of the names that you did mention – I will refrain them for buying now

Ambika Cotton Mills (22-08-2023)

Not a good company to own. Here’s why:

It’s cheap on valuation, but

-

Industry::Textiles is a cyclical industry, presently with high cotton (raw material) prices and muted export demand. The conditions are a strong deterrence to both earnings growth and multiple re-rating probabilities;

-

Company:their business is in a very competitive industry – they have had great double-digit margins bc. of their loyal customer base (compared to Nitin Spinners and so on), not their exceptional operational ability (i.e. page industries). This is an advantage they can lose easily, given brands do not particularly have high supplier loyalty.

-

Lastly, the management: is old and conservative. That is not necessarily a bad thing. But in an industry which is hyper-competitive and extremely vulnerable to demand and supply trends, I want to see management which strives for sectoral leadership by taking bold steps. The survival rates for textile mills are among the lowest (funeral homes being the highest). Thus, if they do not snatch market share, their share will always be eaten away by other sharks. Moreover, in an industry which has immense potential to draw investment out of China, Bangladesh, Vietnam and into India (mainly bc. India has close proximity to cotton as a raw material domestically and from Pakistan + cheap labour), I just do not see the management of Ambika taking the risk and trying to grow. They have been and always will be in survival mode.

In conclusion, the stock presents a limited downside due to cheap valuations and a strong balance sheet but does not present multi-bagger-like growth opportunities. Expect 10-15% earnings growth and equivalent share price growth.