I think it will trake 2-4 qtry when investor will see consistent returns their perception will change regarding management. I think managemetn has leared their lession in 2017-18 and taken very objective approach towards Business and their focus. I think it has started yieldign results for company & few more qtr investors confidicen will improve & will rerate it .

not to forget this is good ESG story as well. ESG at this valution is very attractive in long term.

note: I am invested inthe share from lower level and recently also accumated some qty so my opinion might have some level of biased.

Posts in category Value Pickr

Va Tech Wabag (22-08-2023)

KPI Green- Turning Sunshine Into Cashflows (22-08-2023)

One of the very important questions asked in the con call was that while other companies in this business are making losses how come KPI Green is so highly profitable. The management glossed over this question without offering any substantial justification.

Will definitely like to know more on this.

Yash Pakka – (Previously Yash Paper) – Rising from ash (22-08-2023)

Any link for latest concal …

BSE (Bombay Stock Exchange)- Bet on Financialization? (22-08-2023)

How much BSE charge on Cash and F&O and what was the revenue contribution from these segments in FY23?

E2E Networks Ltd – Listed small Cloud computing player (22-08-2023)

With reference to the con call and points raised here.

- Exclusivity with Nvidia – in a market where demand-supply dominance keeps alternating, exclusivity isn’t necessary a good thing and flexibility to source from wherever available is the right strategy.

- Capex – loosely put couple of hundred crores; they have not thought out this wanted to communicate the 30-40% growth as the key theme.

- Infra utilization – they rent DC and invest in GPUs, Network, etc. They couldn’t give sense on utilization, but given they are looking for growth and investing in Capex utilization is likely to be high

- Churn – They didn’t give a number and mentioned how churn may not be a simple metric to calculate. Next time, let’s push for a 1-year retention number as that will take care of anomalies of lumpy demand across quarter.

- USP is a tough thing to articulate for anyone. They spoke of their cost / price advantage (which is key) and customization for the target segment which is mid-market.

This company is tiny at this point in time, but a good acquisition target at some point provided they keep scaling. Given their market penetration, growth should be possible over foreseeable future.

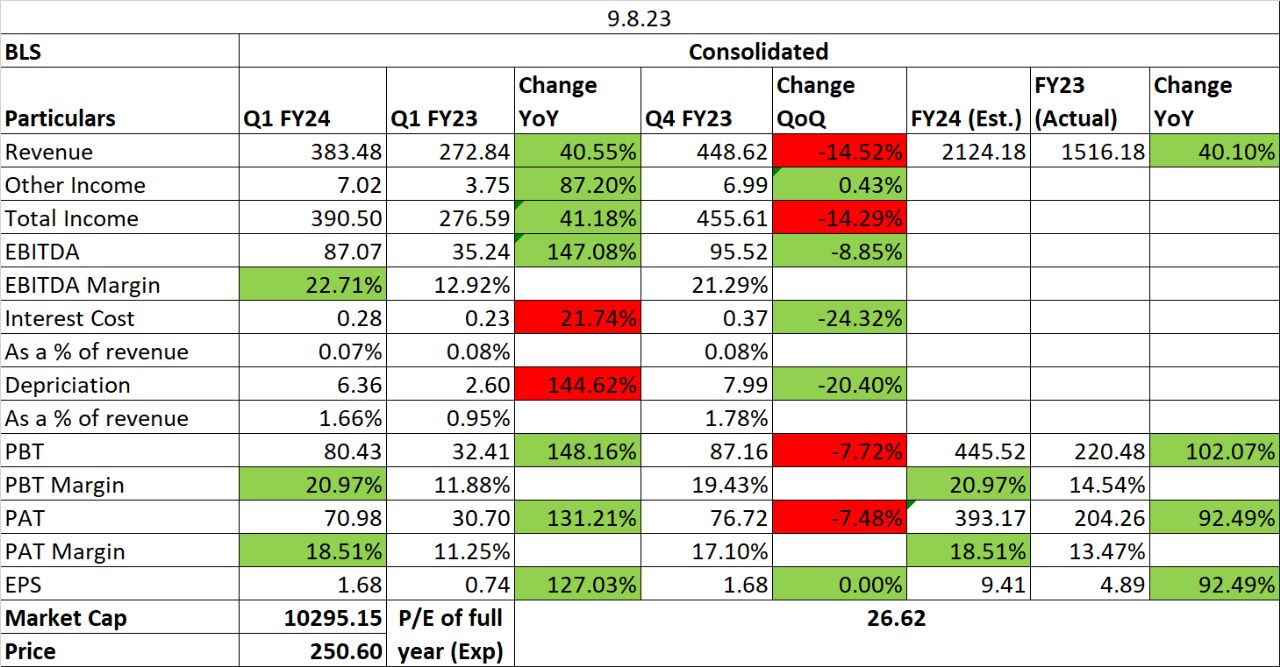

BLS International (22-08-2023)

- Annualized ROE stands at 37.3%. Company constantly strives to improve this by better utilization of assets and cost optimization, resulting in improvement of margins.

- The Group continues to remain debt free and have Cash of Rs 642 crores. BLS International plans to utilize its cash for acquisitions, opening offices in new geographies, and expanding existing businesses.

- Company announced IPO for subsidiary BLS E Services to raise funds to support growth strategies for Digital Services (e-Governance and Banking Correspondence) business.

- Cost optimizations and Value Added Services helped offset rise in employee costs, leading to better EBITDA margins.

- Looking for inorganic expansion opportunities in both verticals that is visa and digital services.

- The Ministry of Foreign Affairs, Spain has awarded BLS International the global contract for visa application outsourcing for the second time in a row. The contract covers Europe, the Americas, Latin America, the CIS, Africa, the Middle East, and APAC, amongst other regions. Company also won new contracts with the Italian government, Poland government and other governments.

- The growth is returning to pre covid levels. Company’s prices for both service charges and other services have increased, so company expects to maintain their current growth momentum going forward.

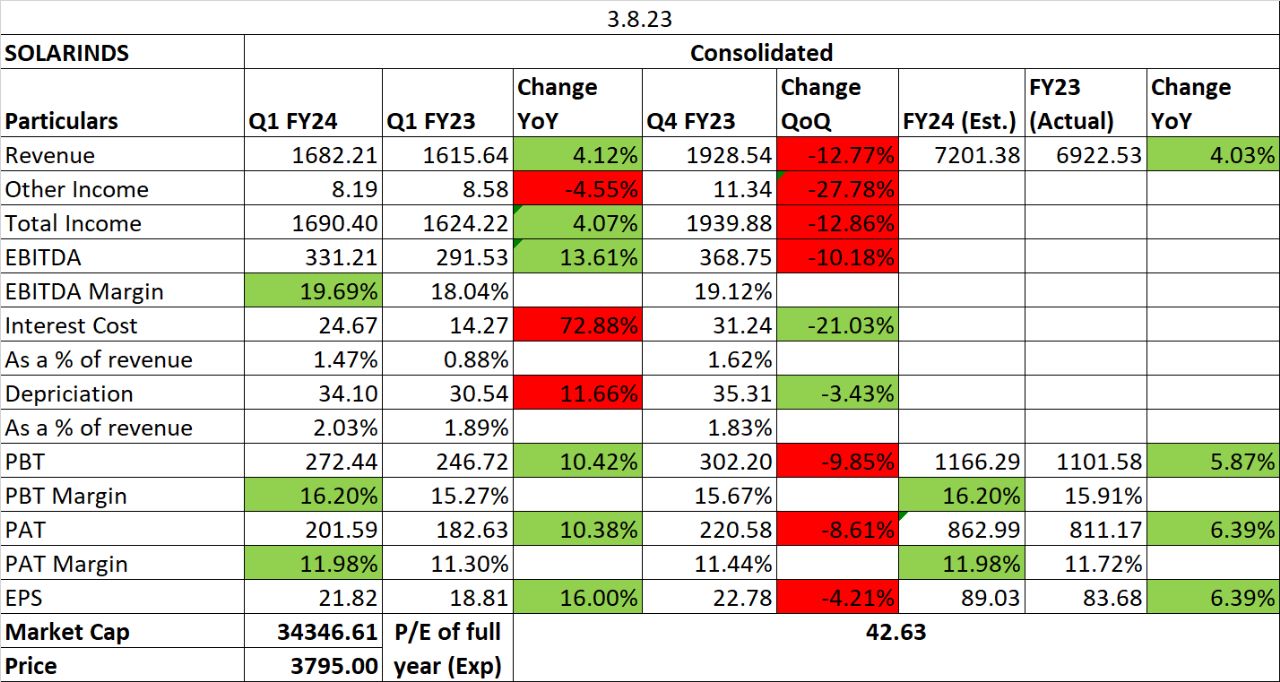

Solar Industries Ltd (22-08-2023)

- Net Debt has reduced from 910 cr in FY23 to 698 cr in Q1 FY24.

- WC days have also reduced from 95 to 72.

- Order book status is currently 2678 cr. Defence order book out of which is 1054 crores.

- Defence revenue reached a new high at INR 155 crores, with a growth of 142% YoY. Defence revenue expected to exceed INR 700 crores annually.

- EBITDA margins increase was supported by defence sales.

- Expectation of higher prices in the second half of the year for raw materials. This might affect margins in H2FY24. Need to check.

- Plans to increase global manufacturing presence from 8 to 12 countries. Expansion plans in Indonesia and Australia to contribute to volume growth. Expectation of breakeven in South Africa and profitability in Australia in FY24.

- Future Outlook: Expected annualized volume growth expected to be 15-20%. Margins should be maintained around 20-22%. Improvement in housing and infrastructure demand is expected from Q3 onwards. Capex plans of INR 750 crores for the year, funded by cash generation from operations.

Newgen Software (22-08-2023)

Nothing extraordinary has happened, these are markets, they punish sometimes on extreme downside and sometimes there is such euphoria on upside and it starts looking absurd. It was at 15 PE once now near 40 without much change in fundamentals. Disc: Invested and looking carefully on signs of euphoria ending.