Recently covered a blog on how to judge management quality with some relevant case studies.

Posts in category Value Pickr

NILE Limited-Lead Supplier (21-08-2023)

Waiting for better valuation to enter. As of now not holding.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (21-08-2023)

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (21-08-2023)

Investing Basics – Feel free to ask the most basic questions (21-08-2023)

It would essentially be the same thing. The idea behind it being that in case of bankruptcy or liquidation (all liabilities are squared off by assets) how much of the value is to be returned to shareholders. Hope this helps

Investing Basics – Feel free to ask the most basic questions (21-08-2023)

It would essentially be the same thing. The idea behind it being that in case of bankruptcy or liquidation (all liabilities are squared off by assets) how much of the value is to be returned to shareholders. Hope this helps

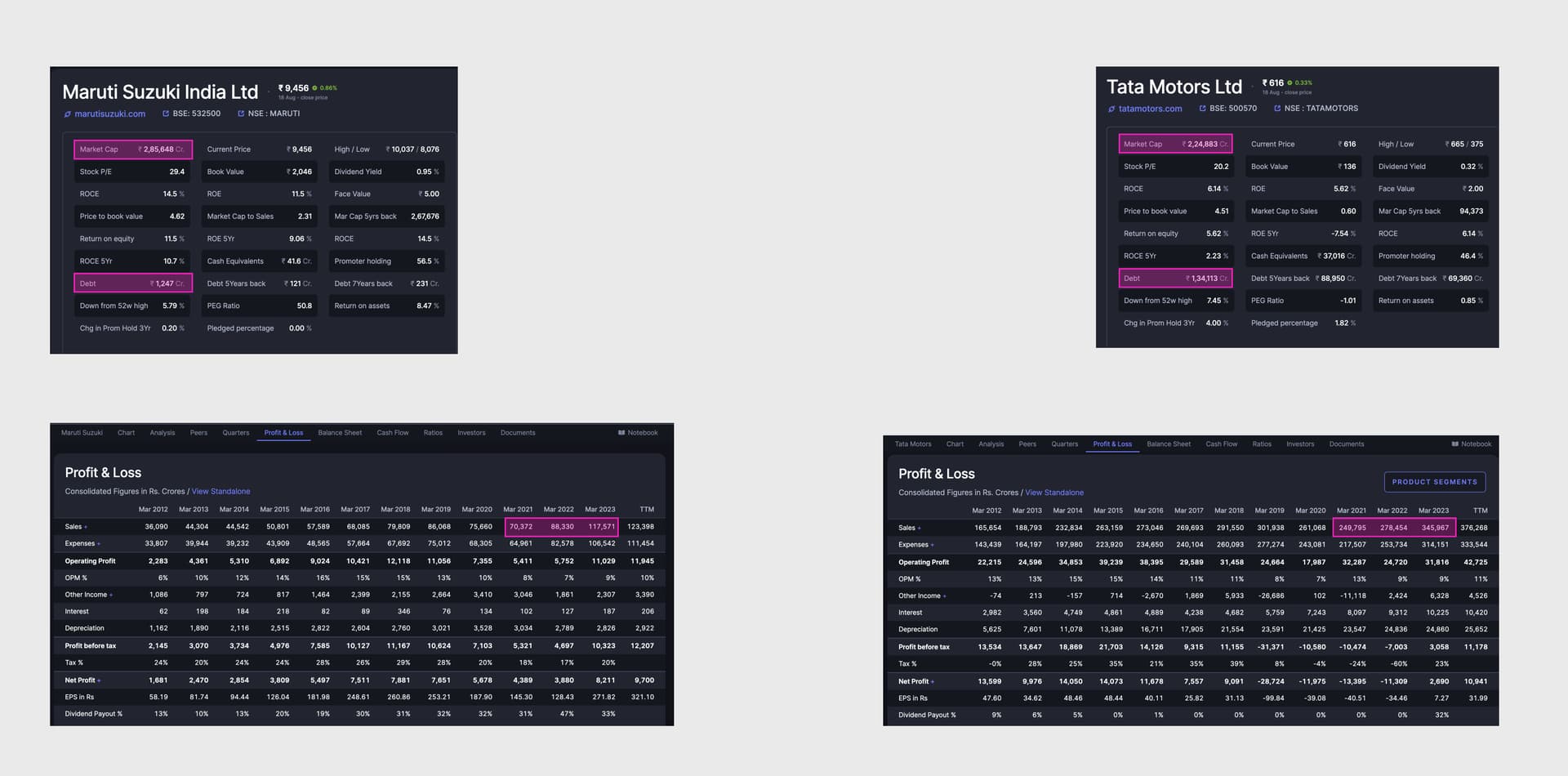

Tata Motors – DVR (20-08-2023)

Using this post to document my thesis for holding TaMO – DVR

(Other people have already written quality quantitative posts under this thread (eg: this one by @GourabPaul) – by repeating information I will pollute the thread and not add any value. Instead, I’ll write something that is not talked about a lot on this thread)

My reason: Value (even in this market).

a) TaMo does more than 2x sales as Maruti but has a lower Market cap (+20k for DVR). It does more sales every year than it’s Mcap.

b) Imo, if the debt were to go off, the real numbers would surprise everyone. Can the debt go off? I believe they are doing the right things and the trajectory is in the right direction (again, not going to repeat quantitative information since there is enough of it in this thread).

Risks:

1. Hydrogen-powered v/s EVs: If somehow Hydrogen vehicle scales up, I believe that government would prefer/push Hydrogen over EVs (especially how China’s dominance in the EV value chain is). I am unsure how long can I hold TaMo <I’ll use this space to expand more as I find hard evidences (or) frame my mind>

2. Is another pricing war coming?: There are new manufacturers coming up (and most likely more will come up for EVs) which could eventually cause a margin erosion. Be it pricing wars in telecom or making the world’s cheapest car, the group’s history of failing at “good ideas” is not unknown. So once again, I have doubts about how long I will hold TaMo.

Eros international (20-08-2023)

Amy one tracking this stock still can give comments

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (20-08-2023)

We were reading exact same articles about ITC an year back. Now the same analysts are extremely bullish.

Let’s say it this way: Analysts are always bullish when stock is in uptrend and find reasons why stock deserves premium and the reverse is true as well.

You make lot of money buying stock when analysts are pessimistic as long as business fundamentals are great and there is a scope for future growth.

HDFC will not get same valuations like it used and it is expected. You give premium valuations to the stock which is growing at rapid rates. HDFC with its size cannot match it’s past performance but I won’t be surprised if it is still trading 3X book value in 2030.

Shivalik Bimetal Controls Ltd (SBCL) (20-08-2023)

@rupeshtatiya Very interesting post. In my calculations I had taken domestic smart meters market share over a period of years for sbcl to be 50% even though the management had said they have 60-70% domestic market share for shunts in single phase meters and going forward expect similar market share in smart meters as well , specially with Genus,HPL etc already as their clients. In view of the post by @Simrat about the possibility of these smartmeters getting hacked a case for raising barriers could be made , but only future concalls can reveal where sbcl stands as regards lower cost shunts from Chinese competitors.(if such a ban fails to materialize for whatever reasons).