Posts in category Value Pickr

Hitesh portfolio (20-08-2023)

hi hitesh ji

Are you tracking lemon tree hotels?

Factor investing & available passive instruments in india (20-08-2023)

https://abimehrotra.wixsite.com/mysite/indices-return-probabilities

I have done a study on how factor indices have better rolling return probabilities than market cap based indices.

This should motivate you to move towards factor Investing.

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (20-08-2023)

Another interesting commentary from the new CEO. The thumbnail is highly misleading (typical of news channels) however looks like there are some green shoots emerging on the office space growth potential especially with GCCs coming in

Specifically on Embassy, the fact that they are Bengaluru heavy could be a double edged sword. As a unit holder i hope they diversify a bit out of just one micro market. However RTO is clearly an upward trend. Whether it will reach 90% levels is yet to be seen with WFH and flexi work

Disc. Significant holding

Office Space Requirements Will Increase 2x Over The Next Few Years: Embassy REIT | CNBC TV18

PGINVIT impairment of investments in subsidiaries and book value (20-08-2023)

All REITS/INVITS undergo a periodic exercise to determine the net asset value of their underlying investments in subsidiaries. Whenever there is a difference between the asset value on the balance sheet and the likely future cash flows the asset value gets revised and possibly there is impairment.

This is similar to depreciation, the difference being depreciation is more predictable and regular

If you see page 18 of the annual report you will notice impairment has been done across the board for all assets in PGINVIT. This could be a one off exercise and may not happen every year. Current cashflow will get a boost as impairment is a non cash activity (it should be balanced out in the balance sheet and income statement). However would be good to keep in mind the potential of future cash flows from these assets. Hope this helps

Goldiam International : A rare shareholder friendly and debt free Jewelry company (20-08-2023)

In the specific case of Goldiam, NO. We held the stock for a long period before the changes in buyback rules were in effect; and when the father of Rashesh Bhansali was around and running the firm. My experience was they were a very minority shareholder friendly family, extremely transparent in responding to my queries and with substantial disclosures in their reporting. They had done buybacks even earlier, and would commit to dividends too.

I don’t think that would have changed.

P.S: No investments

Moldtek Technologies (20-08-2023)

let’s add a different perfective to this co:

Driving factor: Their abnormal industry leading margins

Disclaimer: Invested and Intrigued.

They operate in two verticals

- Mechanical engineering services

- Civil Engineering services

About mechanical engineering services:

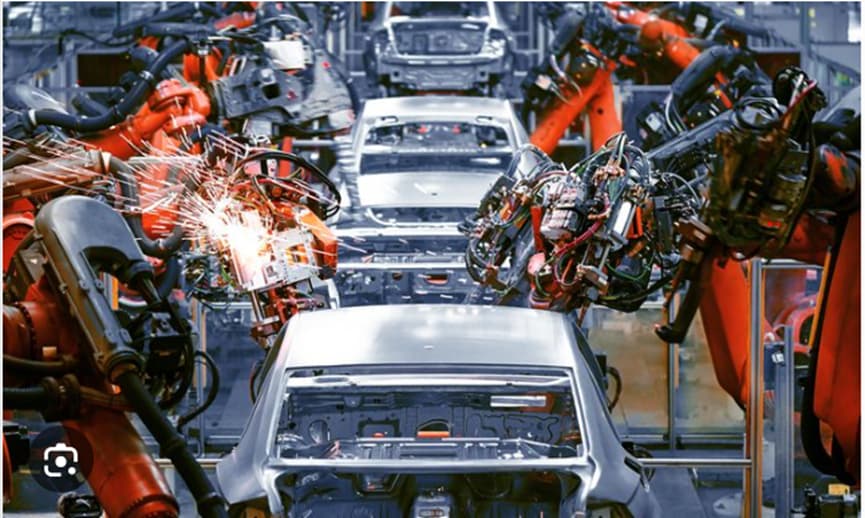

First of all, why do you need BIW fixture design and robotic simulation?

As everyone knows car manufacturing involves different assembly lines for different assemblies/sub-assemblies. For example, BIW assembly line, Door assembly line, Roof assembly line, Engine assembly line etc finally each sub-assemblies will be assembled to make a complete car. So, the total time involved to make a complete car is called “cycle time” (how many cars you produce per time considering you have all the sub-assemblies ready) for example Tesla model 3 cycle time is 64 sec which is half the Auto industry average our Indian TATA Harrier has cycle time 104 sec ( not an apple to apple Comparision) but tesla employees more robots (500+) and less manual intervention (95% automation). So, cycle time plays a very important factor in the overall manufacturing cost! that’s what we call “scale economies” (Ford invented it, Toyota mastered it, Tesla set the standard!) in Musk’s own words,

to each achieve a particular cycle time you need to design the production line and run a virtual simulation of an assembly line which consist of robots, fixtures and a conveyer belt to move the parts from one station to another as shown in the below picture to calculate whether you are actually achieving or not right!

That’s where the 3-D modeling tools like Catia and simulation software’s come handy (each license costs 10L up to 50L and A&M of 2L annually, pretty lucrative right! that’s the power of SW product companies!).

OEM’s gives these assembly line set up (design and simulation) to Tier 1’s such as FFT, VDL, KUKA etc and they will give to Indian or Mexican counter parts! (You know why!). Pls watch the below video to understand how it’s done. Which involves both modeling and robotic arm simulation. Don’t overimagine/overestimate when they use the term “Robotic simulation” because I’ve observed many people get overexcited when they saw the word in their concall report.

Tecnomatix Process Simulate – Event Based OLP

Let’s talk about Civil Engineering services:

Structural Steel Detailers: These professionals prepare detailed plans, drawings, and other documents for steel fabricators and erectors. Using engineering drawings and specifications from architects and engineers, they create detailed ‘blueprints’ for the fabrication and erection of the steel framework. The detailer’s drawings provide all the information needed to cut and weld all pieces together. Mold Tek majorly into detailing (low margin) and not into Engineering. Those are not my words management itself says “Let’s say, we are charging $25, $28 or $30 at the most in detailing, we can aim at $60 to $100 in design, member design. But currently, we are not doing member design.”

Now we will discuss operating matrix of the co, with such low billing rates in Civil engineering services ($25/hour) and Mechanical engineering services ($18/hour) they are clocking north of ~30% OPM that’s just Wow right!

Let me tell you before all of you assume that Co is addressing to “Niche” segments which no listing player is operating or left the field. Just look at their employee realization matrix, you will realize that they are grabbing low hanging fruits out there (in terms of type of work)

Moldtek is Rev155 cr/1200 employees = 13 lakhs per employee

Kpit is at Rev 3777 cr/8053 employees = 47 lakhs per employee

LTTS is at Rev 8,716 cr/23,392 employees = 37 Lakhs per employee.

that’s the very reason why KPIT and LTTS just ignored these verticals and focused on other verticals quickly big time. So we must be happy right ! biggies left and you set the prices! Unfortunately, no! There are infinite small/chota/meduim players operates in this space, if you don’t do it for $18 there are plenty who are ready to pick the work @ $15. Pls find few small players below to name few.

Satyam-Venture Engineering Services

Mechanical Engineering Services | Envision Integrated Services Pvt. Ltd. (envisionis.in)

[Group of Engineers] (https://www.groupofengineers.com/)

Two ways to look at the business:

First: You should appreciate the company and be more than happy as the Co is showing how a service company should run to other service co’s despite being having a very low billing rates ($ terms) still be able to maintain OPM north of ~30%. By using some ways like getting talent from Engg trainees by offering low pay + doing some “naughty license proliferation” things etc etc those are different matters altogether ![]() and that’s absolutely fine as long as you are doing great for us (investors) not for employees though!

and that’s absolutely fine as long as you are doing great for us (investors) not for employees though! ![]() )

)

Second: You should start feeling little uncomfortable about how long these type things can continue to work once the company scales up because they day you start doing business with direct OEM they will inspect your infrastructure physically and check your legalities etc.

A bit of overconfidence words from management, which taste sour to me, but you can totally ignore my views! ![]()

It’s fine if you are not aware of what others are up to, considering your busy schedule but don’t assume the things and paint a rosy picture for yourself and to investors. Which will hurt you and as well as investors.

Well, that is an outright lie, you spend three days a month on the company and come on concalls to give these blatant lies.

So, if you don’t spend your maximum amount of time on the company then don’t address the concalls and don’t assume that others are also at your level because they are clearly not! Nothing wrong in aspiring and competing with others but it’s foolish to assume that others are also at your level (you are doing $20 million rev and KPIT is doing $400 Rev and you are saying both are at same level pls take a look at their employee realization and avg billing rate they charge to the client).

Things I’m looking forward to as an investor:

-

The company must expand into other verticals because both the current verticals have very limited TAM, I know this being an industry person but if you still looking for confirmation from the management here it is

-

Getting into wire harness and plastic molding tools etc is fine they bring the revenues, but they can’t put the co on par with other E&RD service companies’ capabilities.

-

You just can’t get into the embedded electronics or other tech verticals with this existing team you need different set of leadership and sales team at different scale levels of the company. That’s what differentiates a $20million company and a $400 million or $1 billion service company.

-

It’s just their first concall so need to wait how they sound in subsequent concalls

Delta Corp – A huge but risky opportunity (19-08-2023)

Reading a.lot about this ’ killing’ type adjectives. In my humble opinion we need to ignore this noise. Why are cigarettes companies still around? So will Delta thrive.

PMS Funds – India (19-08-2023)

Same question. Has anyone invested with them? Team – Counter Cyclical Investments

The returns are crazily unbelievable! What do you guys think about this one?

Any opinion sir? @8sarveshg