Posts in category Value Pickr

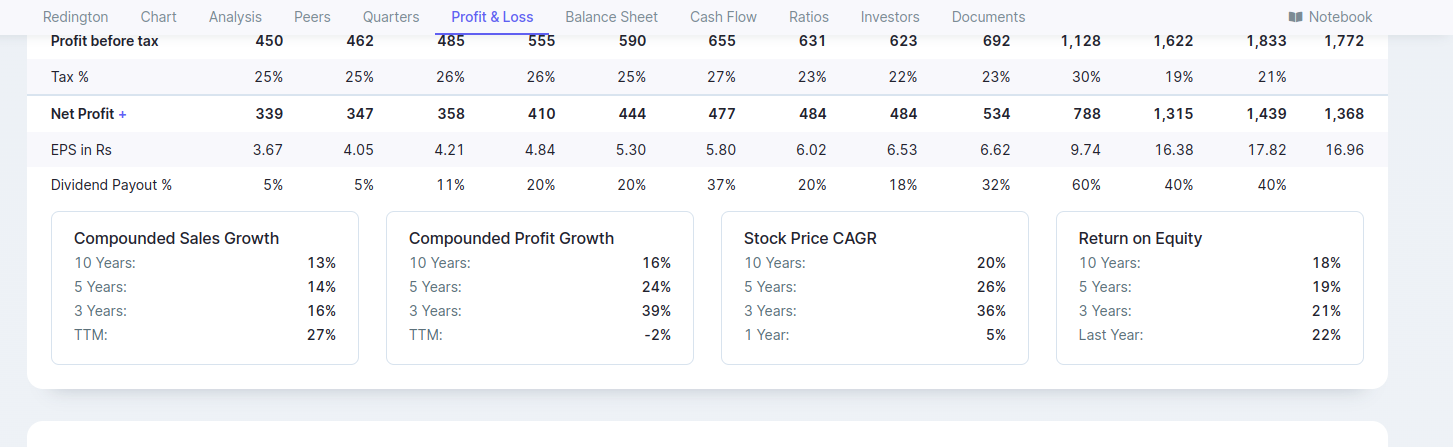

Redington India : Strong Performance history, re-rating candidate (18-08-2023)

As highlighted earlier in this thread, Q1 challenges are due to economical challenges across the geography and still management says they have displayed profitability in countries like Turkey.

Also increase in investments has impacted profits. Increased expenses will continue for next 4-6 quarters. In Q1 FY24 earnings transcript, mgmt has touched upon staying competitive and very clear on what they are doing. This sounds quite optimistic.

On other side, if we see long term, Sales, Profit, Stock price have all increased with not much of deviation. Looks more for long term investment.

Disclosure: I am invested a small % for last 2 years. Considering Technicals on a monthly charts, I am exiting my position.

StageInvesting +Elliot Waves (18-08-2023)

Hi @StageInvesting ! Any update on Mayur Uniquoters? You had posted the chart earlier but it is missing from your current PF.

Macfos Limited- A niche E-commerce Company (18-08-2023)

if their is regulatory shift towards India based manufacturing, surely Macfos will pivot (afterall they are running a business).

in my mind, for their B2C biz to grow, TAM has to expand. Are their enough tinkering hobbyists in India today? will this segment grow over a period of time? need to be researched. Can look at how Digilink grew their business in US.

Disc: studying, not invested

Hitesh portfolio (18-08-2023)

HI Hiteshbai,

What about Bajaj Finance? In the last two years instead of excellent performance from all fronts- increase in the number of customers, AUM, Deposit growth etc., the stock remains at the same level. Appreciate your technical analysis on that.

Krishca Ltd : A SME offering steel strapping Solution (18-08-2023)

Minimum 3 years from the date of lisiting.

Hitesh portfolio (18-08-2023)

Dear @hitesh2710 Hiteshji,

How do you see the overall markets now. Nifty and large caps looks like reversed the trend. BSE small cap index going up. 1 month basis nifty is 2.3% down and BSE small cap.index is 4.6% up. I was reading the thesis by Mr. Nooresh Merani @nooreshtech ?) that when ratio between the two trends above 1.8 and when a diversion between these two is danger zone.

Also, how do you see GAIL stock price movement. Looks like the stock price is sideways, but slopping down. The recent previous high is around 112-113 and currently the stock is trading there. Do you keep stoploss around 110-112 levels or will you give more leeway ? RSI below 50, stock below 20 day moving average, close to 110 which is 50 day moving average.

Thanks for your generous and expert views as one of the best informal teacher on stock markets.

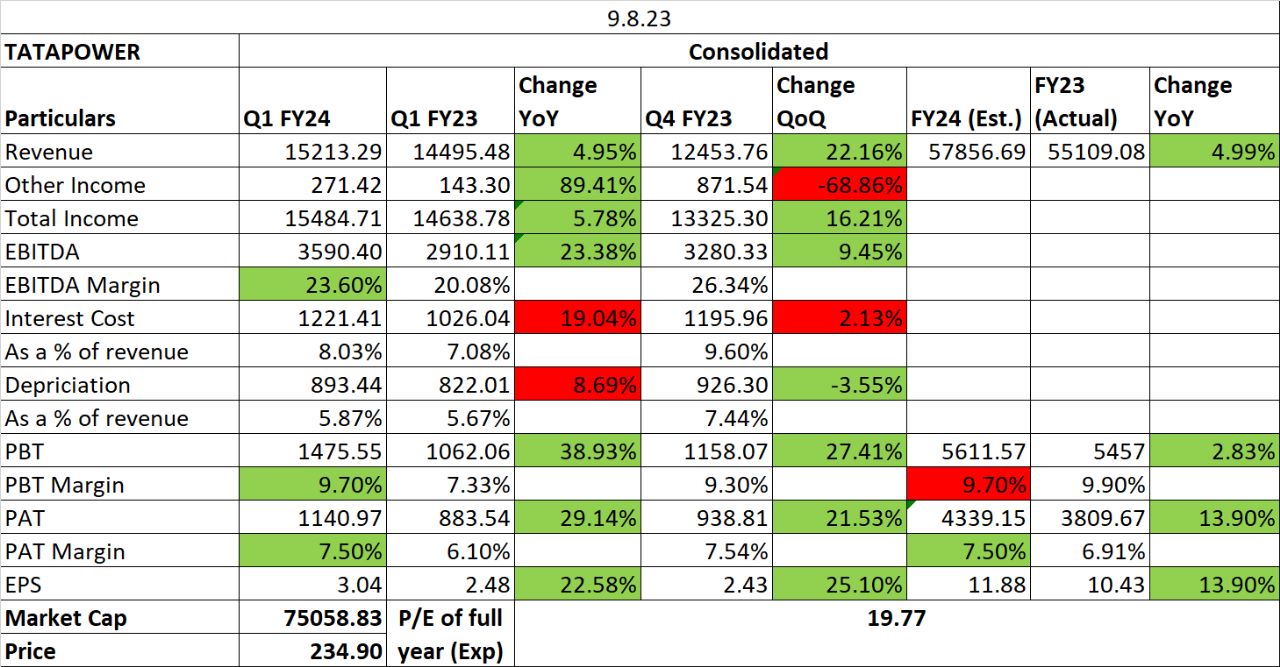

Tata Power Limited (18-08-2023)

Tata Power Q1 FY24 Results Update:

- Become carbon net zero before 2045.

- Become water neutral before 2030.

- Zero waste to landfill before 2030.

- Solar Rooftop, Pump Business Orders: Order Book (Incl. Group Captive) at Q1 FY24 end stands at ₹ 2,500+ crore. Strong traction seen in Group Captive with orders of 415 MW won in Q1 FY24. Installed 112 MW in Q1 FY24. Channel network crosses 480+ across 275+ districts.

- Solar cell and module manufacturing project remains on track: First module production expected by end of Sep-23 and first cell production by Q4FY24. The management emphasized towards improving the margins in solar rooftop and pump business. The prices of solar cells & modules and wafers reduced significantly, in Q1 FY24. The management expects with more capacity additions taking place in China and Southeast Asian countries, there would be an oversupply of cells & modules which would result in further reduction in prices, going forward.

- Tata Power maintained its FY24 capex guidance of Rs. 12,000 crore and aim to be below net debt/EBITDA of 3.5x.

- The company plans to add 2 GW to 2.5 GW of renewable capacity every year, with a focus on utility scale and group captive projects.

- Tata Power is also investing in pumped hydro projects, aiming to support 6 GW to 7 GW of renewable capacity for round-the-clock power.

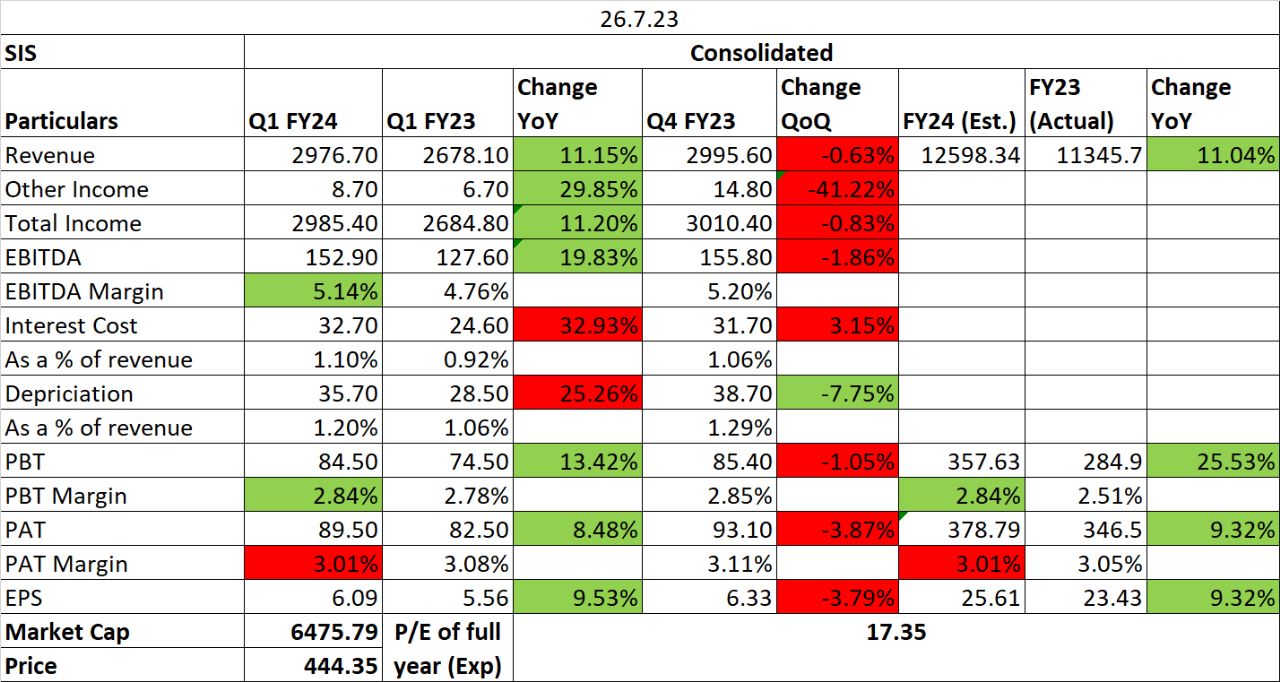

Security and Intelligence Services (India) Limited (18-08-2023)

- Industry is transforming towards more organized players. Rising compliance with laws and regulations. Rising demand for superior services and quality. Rising per capita income, urbanization and Infrastructure Growth.

- Our Vision 2025, which came into effect in FY21, outlines the goal of transforming our market leadership into market share dominance and transitioning from a Services Company to a Solutions Company.

- Margins in the FM business have improved but are still below pre-COVID levels, and the company is working on further improvements. Cash management business will see further improvement in revenue and profitability.

- OCF to EBITDA conversion was negative due to increase in DSO. Historically Q1 sees weak collections since Q4 has strong collections. Usually collections improve in June itself which didn’t happen this quarter. DSO for Q1 FY24 increased by 6 days.

- Elevated SG&A costs in FY22 and FY23 impacted margins, but actions have been taken to address this and improve margin profiles.

- The VProtect alarm monitoring business has the capability to deliver double-digit EBITDA margins.

- The Australian business is showing an uptrend, and the labor supply situation is easing, which is expected to have a positive impact on performance.

- SIS aims to build all its businesses and sees itself as a platform with separate CEOs and CXOs running each segment. The company is focused on returning to pre-COVID levels of margins for all businesses and expects substantial growth and market share uptick in the post-COVID world.

- Company has maintained 6% EBITDA margins guidance and has refrained from giving topline guidance.

The harsh portfolio! (18-08-2023)

Dear Harsh,

I have 2 questions for you

- What is your exit multiple in terms of Price to Book for Aptus Housing Finance.

- I see you are holding Amara raja since about 2 years. You still have the same level of confidence in Amara Raja as before ?

I have joined VP recently and its a delight to read your threads.

Thanks in advance