CRISIL RATING UPGRADE AVL AUG 23.pdf (907.7 KB)

Posts in category Value Pickr

Pokarna Limited: (16-08-2023)

Latest con call has answered few of your questions /doubts Q1FY24 concall

Pokarna Limited: (16-08-2023)

Latest con call has answered few of your questions /doubts Q1FY24 concall

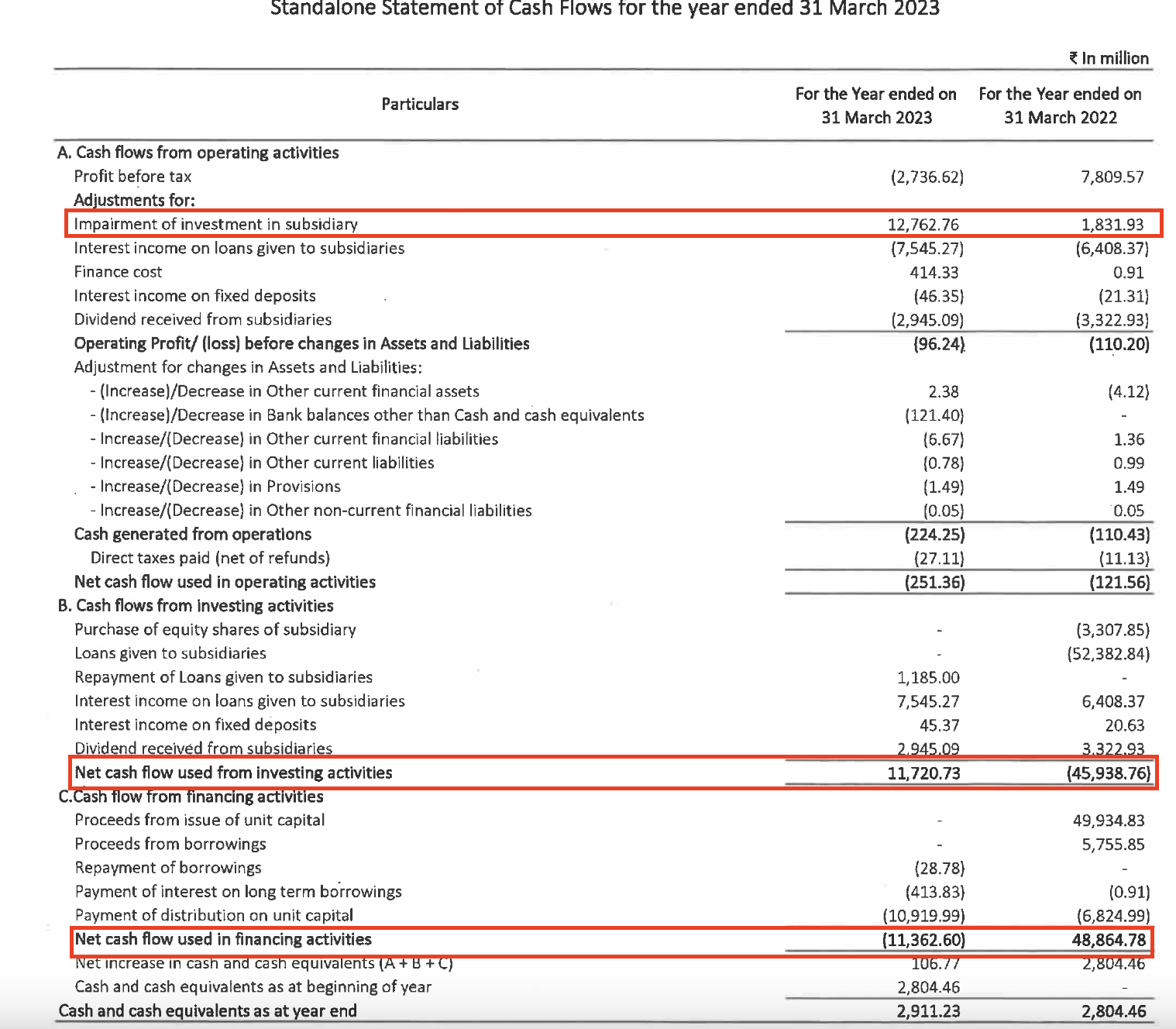

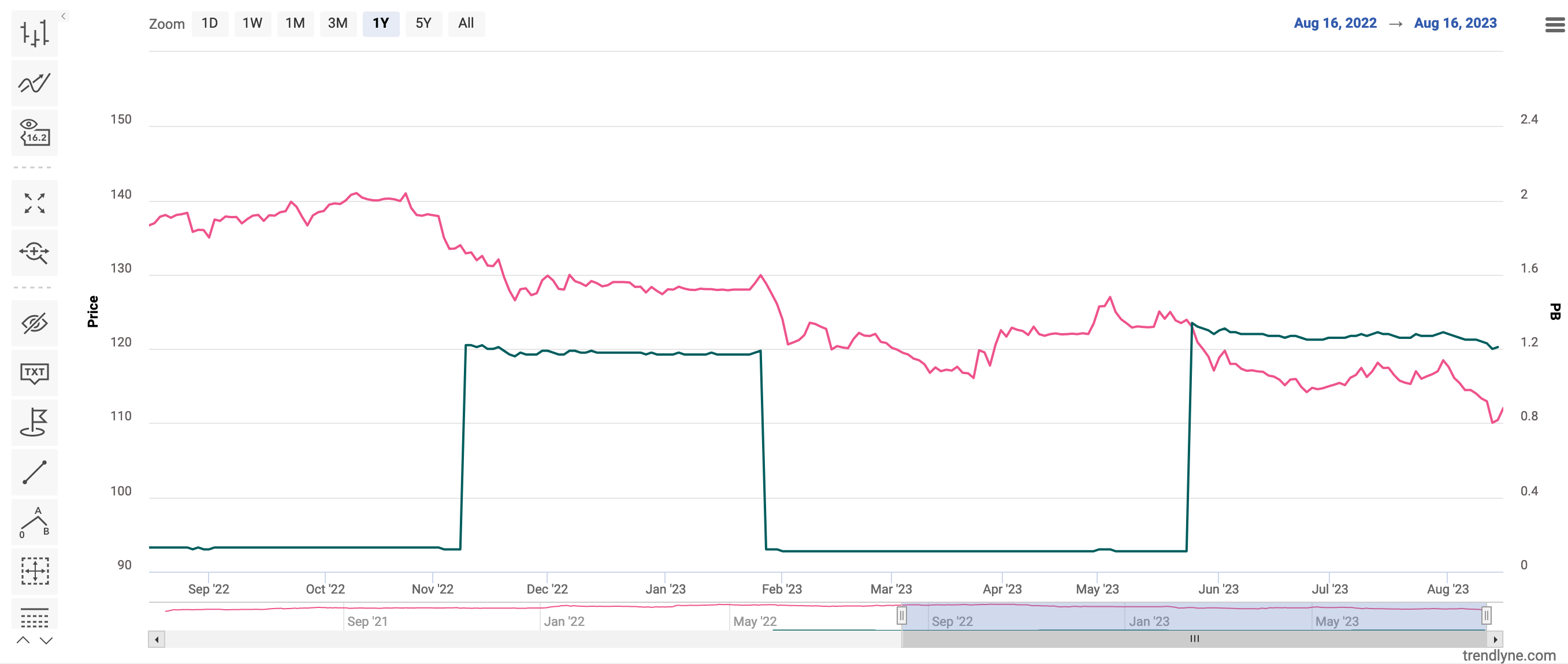

PGINVIT impairment of investments in subsidiaries and book value (16-08-2023)

I have difficulties in understanding the cash flow statement of PGINVIT.

-

The item “Impairment of investments in subsidiary” seems to be extremely high compared to last year. How do we know what led to this and in which subsidiary?

-

Do the numbers inside brackets like (11362.6) mean negative values?

-

In spite of the huge impairment, we still see the cash flow is positive and better than last year. Is my understanding correct that (45938.75) invested last year is an outflow of cash and this has given returns, a positive inflow of 11720.73 in 2023?

Also, I noticed that the book value is alternating between a high and low, like a square value. What could be the reason for this?

Ambika Cotton Mills (16-08-2023)

What prompts you to guess that the promoter is not going to be shareholder friendly ?

If your view is that 300 Cr cash on book is too much for 800 cr networth company, it should be noted that most of this cash is accumulated in the last 2 financial years due to huge profits compared to historic average. The company has consistently maintained dividends of 20%(which is ok for a company which had no excess cash but some debt till FY20) and RoE of 16%.

I find the management very sensible in deploying some of the cash when they decide to go for 8.4MW rooftop solar power capacity in their Dindugal manufacturing plant.

@alokinvestor is right. At 1 X P/B, 1 X P/S, 3 X EV/EBITDA, 2.5% dividend yield, it is undervalued.

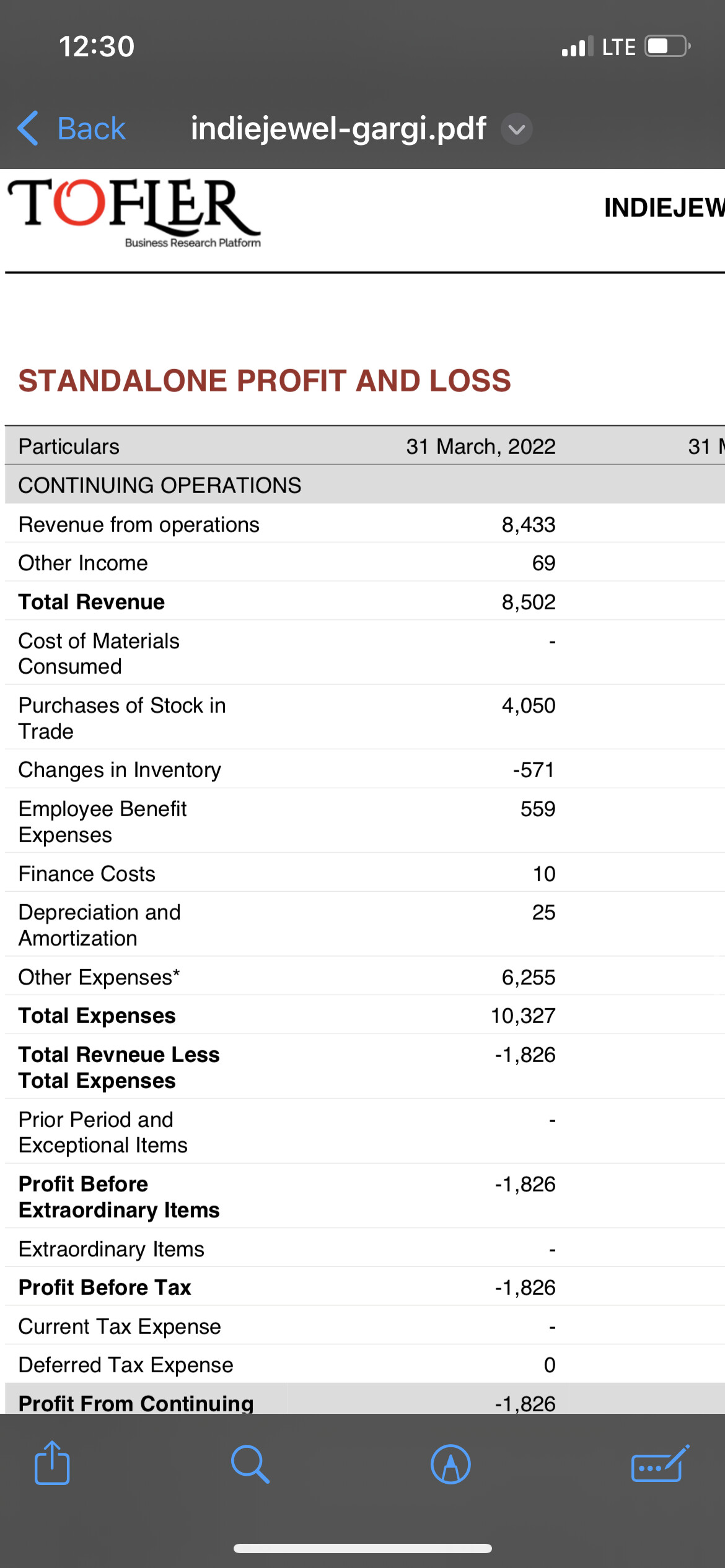

PNGS Gargi Fashion Jewellery Limited (16-08-2023)

COMPETITION:-

The closest competitor of Gargi is a brand called Giva. Giva is a startup from Bangalore, with a revenue of 80cr and a loss of 18 cr, key thing is they have a great gross margins compared to Gargi.

Adani Power: Beyond ‘Adani’ (16-08-2023)

GQG is going all-in investing in Adani group stocks.the article states that GQG has already madev70-80% returns on its investment

Indiabulls Housing – A compounder from here? (16-08-2023)

I only hope they don’t turn out like DHFL. I might be comparing apples to oranges but finance companies have always been hard to evaluate because we don’t really know how their loans turn out.