(post deleted by author)

Posts in category Value Pickr

Hindware Home Innovation Ltd on to rapid growth post demerger? (16-08-2023)

Hindware home will scale business easily due to strong branding, current quarter is one off and gives opportunity for new investors. Its cheap seeing growth plans, sales/Market cap, EV/EBIDTA levels. Fair valuation of market cap should be 5500-6000 cr. I entered this at 75 levels in 2020 and moved out at 470, today got opportunity to enter again:joy:![]()

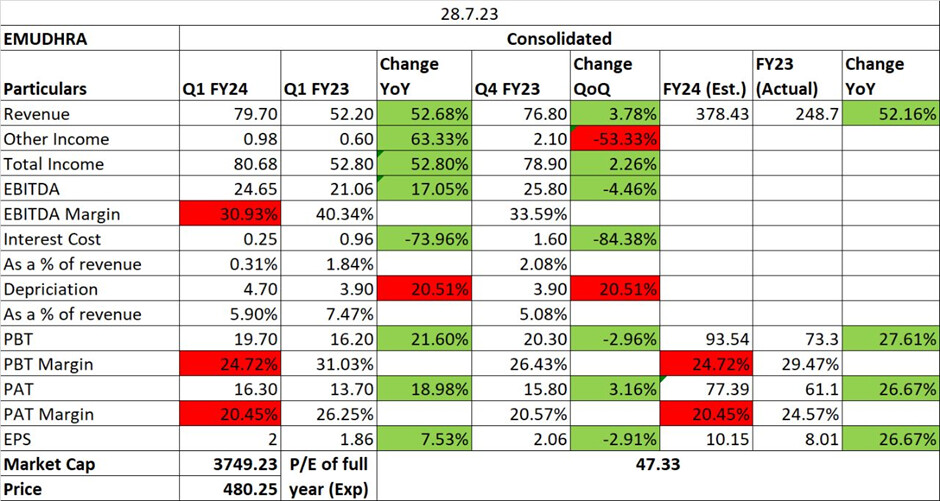

eMudhra – building seamless digital and paperless experiences (16-08-2023)

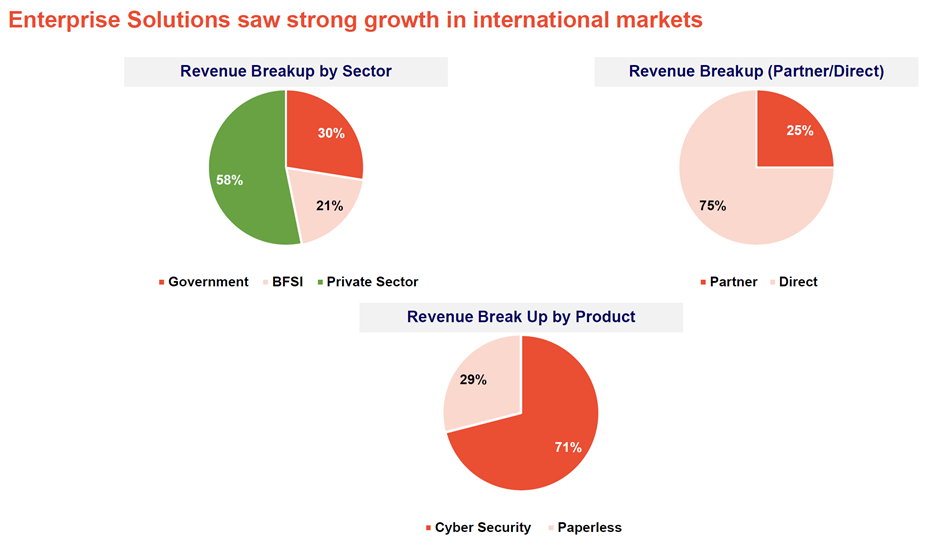

- Revenue growth driven by Enterprise Solutions in overseas markets.

- Despite investing in overseas markets for future growth, we have achieved strong EBITDA and Net profit growth.

- Sustained Net profit margin.

- The growth in the international business was supported by significant deals in North America, the Middle East and Africa regions for Enterprise Solutions.

- Cash flow operations, as a percentage of PBT, stood at 65%, slightly lower than the 66% reported in the last financial year.

- Channel pricing for Trust Services remained stable throughout the quarter.

- The company’s strategic shift towards retail business and eSign has proven to be successful.

- Completed acquisition of Ikon Tech LLC, a company headquartered in Houston, TX providing solutions focussed on cyber security and digital transformation.

- In India, the trust services and enterprise solutions segments have shown an upward trend on a year-on-year basis.

- The order book for enterprise solutions in India remains robust, and they anticipate an uptick in the enterprise business as new government and BFSI projects are executed.

- They are optimistic about sustaining their growth trajectory and reinvesting margins into driving further growth.

- Revenue growth guidance of 25% will be achieved. Margins will be maintained at the same level. May increase by 50-100 bps.

- Moat of the business: Company has almost 1/3rd of its employees in R&D currently, so there is a high chance that they will keep developing a niche.

- Attempting to expand the certification products in the private sector market of the US.

- The company is also working with AWS to expand their network and help gain momentum in the upcoming quarters.

Hindware Home Innovation Ltd on to rapid growth post demerger? (16-08-2023)

Thanks for a detailed response. Much appreciated.

I think that Astral would be a good benchmark for steady state Operating Margin. However, Hindware as of now is more focused on revenue scaling being in growth mindset.

I like that each of the division has a seperate CEO. Also, I am impressed by the commentary of the group CFO around strategies and funding of the business.

New CEO is onboard. He mentioned in Q1FY24 call that products need to be rationalized in CAB division.

Piramal Enterprises Ltd (16-08-2023)

why company classified wholesales loans into old wholesale and Wholesale 2.0. ?

Hindware Home Innovation Ltd on to rapid growth post demerger? (16-08-2023)

1…EBITDA

EBITDA margin of Hindware business

A…Bahthware@16.7%

B…Plastic pipe@6.6%

C…Consumer@1.3%

Cera opm is 16%

…We can not compare opm of hindware to cera as hindware has other businesses also like plastic pipe and consumer businesses

=Bathware segments of both companies have similar OPM

2…Hindware want to leverge hindware brand for plastic pipes and consumer segments.These are high turnover/low margin business

=Many of these products are outsourced ,so they can grow into these segments by leveraging hindware brand and less capital.

3…I have done scruttlebutt for their chimney.I can definately say that hindware is among top 5 for chimney

I have also installed hindware chimney at my new home and we are happy for this product.

There is some noise but function is superior than glen chimney that i was using previously.

4…They are aggressively branding Truflow, as i had posted in my earlier posts

5…I dont know about other products performance

6…I had not found anything wrong about managent .Instead most of top positions are outsiders.They may be overoptimistic.

7…Only one thing i donot like is they have over diversified their business ,perticularly in consumer segment.(DIWORSIFICATION !! Fan, air cooler, even AC in future😀)

Rather ,they should limit consumer segment to kitchen products.

Disc…invested

Sinclairs Hotel (16-08-2023)

I recently started to read about Sinclairs Hotels as part of my hotel industry study. It looked interesting as it had no debt and had a good margin compared to pears. When I looked deep I could not get clarity on following

- As the company has partnered with STAAH Technology as channel manager which is already used by Lemon tree from 2017 – what is expected for company revenue? Can they go up from mid range pricing?

- Companies spend ~1% of revenue Advertisement and Sales Promotion out of that I see Pressman Advertising Limited name in related party transactions for Advertisement. Is this common practice common to have ads spent from the related party ?

- In Annual report 2023 they have mentioned that they are now looking to acquire property on lease which enables to grow faster with lower capital investment. If so, what do they want to do with cash in the form of investment in the MF in the balance sheet?

Appreciate your input.

MTAR Technologies – A wager on innovation meeting economies of scale (16-08-2023)

Mr. Srinivas Reddy delves deeper into the company’s performance and future projections:

Bloom Hot Boxes and Sheet Metal: In Q1, they produced 950 Yuma hot boxes with 32 electrolyzers. They have a clear dispatch plan from Bloom for the current financial year. In Q2, they plan to produce 418 Yuma hot boxes, 440 Yuma Santa Cruz hot boxes (an advanced version of Yuma), and 66 electrolyzers. In Q3, they aim for 1,144 Santa Cruz hot boxes and 44 electrolyzers. In Q4, they target 1,718 Santa Cruz hot boxes. They also anticipate new orders for electrolyzers by the end of the year.

Santa Cruz: This is an advanced version of Yuma that generates 65 kilowatts as opposed to Yuma’s 50 kilowatts. They’ve worked with Bloom over the past quarter to make design changes to increase the output of the Yuma unit.

Ebitda Percentage: They had given a guidance of 28% ± 100 basis points and continue to maintain this margin guidance for FY24. The EBITDA margin for this quarter is at 22.4% and is expected to improve quarter-on-quarter based on higher revenues.

Order Book: As of June 30, they have a closing order book of 1,078 crores. They received orders worth approximately 50 crores in the first quarter. They expect major orders from clean energy, nuclear space, and defense in the upcoming quarters.

Defense License: Their defense license has been cleared by the Ministry of Defense’s committee. They expect to receive the license by the next week, allowing them to supply directly to the Air Force, Navy, and associate with multinationals for major defense projects.

New Collaborations: They have two significant collaborations in the pipeline: Fluence Energy and Enerven. Fluence Energy is in the final stage of releasing a letter of intent for 1,000 units with prototypes, which will be executed in FY25. They expect to export to Asian countries, Australia, and New Zealand. They are also in discussions about establishing branches in Europe and the USA, which could generate substantial revenues for the company.

Energy Storage Systems: They are in discussions with two companies, Fluence Energy and Enerven. Fluence Energy is in the energy storage system sector and is close to releasing a letter of intent for 1,000 units with prototypes. Enerven uses nickel-hydrogen batteries instead of lithium, offering another exciting prospect in the energy storage system.

Product Development: They have submitted the first articles of Road exclusively to DRDO, which has been tested under various conditions. They are also supplying four different types of Electromechanical Actuators (EMAs) this financial year, amounting to about 7.5 crores. The business of EMAs will grow year-on-year. They are also starting a new product called “dielectrics” this quarter, which has a potential business of about 250 crores per year.

As a value investor , when do you sell? (16-08-2023)

It isn’t exactly that per se but you can also look at it differently. The total return you can expect from your stock investment is from three components. This is from Value Investing and Beyond by Bruce Greenwald. He talks it through in Value investing lecture Bruce Greenwald briefly. I have adapted some stuff to this as well. Accordingly, the Total return you can expect from your stock is the sum of:

- Shareholder’s Yield – (Cash used to pay dividend + Cash used for Buybacks)/ Market Cap

- Growth in Earnings – Historical EPS growth/ FCF growth or ROCE * (1- Dividends)/ Total Earnings

- PE rerating – Seeing how low or how high can go to your terminal PE multiple (based on historical average or your estimated multiple)

An example to walk you through this is:

Let’s take the case of Pidilite as of today.

- Shareholder return – 0.43%

- Growth in Earnings – 12.2%

- PE rerating – Let’s say I hold the investment for 10 years and the PE will half, the PE rerating if you see by the rule of 72 will be about -7.2%. Of course, the longer you go, the lower its effect will be on the total return i.e for 20 years it will be – 3.6%, for 30 years it will be – 2.4%, etc.

So the total return of the stock can be estimated as 0.43% + 12.2% -7.2% = 5.43%. Of course, this is conservative, and assuming there is no PE rerating it will be the total return will be 12.63% per annum. If this is more than your required rate of return then it would be a good investment for you. But the assumptions for this to work out are that the stock will not have a significant rerating, and the stock will grow its earnings at 12.2% or more throughout your investment period.