I doubt that, Chemical companies are suffering due to destocking in Major Markets.

Some of them already did Capex or in middle of it. They are incurring increased interest cost as well.

New orders will take quite some time for GMM and GLE.

My Observations could be wrong, Pharma Revival Could be a side kick.

Bottom line is in Covid + 1.5 Years Lot of Capex happened hence Orders were booming.

Posts in category Value Pickr

GMM Pfaudler: A safe way to play the Pharma/Chemical cycle (16-08-2023)

KSE Limited — Interesting Business (16-08-2023)

Feed : Key ingredient is Copra along with other grains , this is the key variable that determines the margins. High Coconut oil price is the indicator, if oil price is high they can earn better margins.

Ice Cream : I think they are on the right track, I have checked their google reviews, for every review there is one standard response, a dedicated social media team to monitor these channels will help

Milk + Mil Products : Zero profit , Zero margin business. I am wondering how come other players (state players like KMF/ Nandini, Milma etcc… ) making good money ?

They appear to be serious by hiring a consulting firm to look into the bueinss but unless they conduct calls it is really hard to know what is going on inside.

I have asked around people based in Kerala, they said in feeds they are number one. Very strong brand recall.

Risks :

There are government players in the feed , who get substantial discounts so they sell the feed cheap

Same with Milk

Godrej Agrovet is into all the product categories Feeds, Milk Products including Ice creams (Creamline acquisition )

Promoters + One retial share holder has in total 51% stake , very illiquid stock hard to find decent quantitity to buy.

Discl : Tracking Postion

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (16-08-2023)

Well Satia”s performance is improving because of the following reasons:

-

A large portion of their production is contracted out to state education boards, here the effect of raw material price change is delayed. This was actually a negative when paper prices were increasing very fast. At that time Satia’s profits were lagging its peers. Buy now this is benefitting them.

-

Their utilisation of PM4 is continuously increasing leading to operating leverage benefits.

-

They have installed new pulp machines whose benefits didn’t fully materialise in the last quarter

Globus Spirits (16-08-2023)

Anybody who has attended the concall?

What is the guidance of the management for future?

Accelya Kale Solutions-Niche & Sticky Business (16-08-2023)

Accelya looks very interesting at this point. I have been tracking this company for over a decade. The first time I bought Accelya was way back in 2012 and exited completely in 2018. I started buying again in January this year and will continue to add.

Few points on why Accelya should do well:

- Valuations are cheap, be it historical or absolute.

- Recovery started in late 2021, and numbers have been decent since. My first target was matching 2019 numbers, which was done in this quarter.

- A new growth cycle is underway, I expect earnings growth to be around 20%, revenue growth around 15%. There are quite a few reasons for this –

(i) There’s a trend of new carriers emerging all over the world, so a lot of these incremental partnerships are higher margin in nature

(ii) There’s renewed energy in the airlines sector once again, which means there’s focus on getting a better price for their inventory and also reducing costs, meaning outsourcing of non core functions. This helps Accelya cross sell better. Recent examples are Frontier Air adding Accelya’s AirRM 2, and Thai Airways adding outsourced revenue accounting services 1 to their renewals.

(iii) The biggest driver of growth is this new distribution system launched by IATA, that is called NDC & ONE Order. Will expand more on this –

NDC (New Distribution Capability) is a travel industry-supported program (NDC Program) launched by IATA for the development and market adoption of a new, XML-based data transmission standard (NDC Standard). The NDC Standard enhances the capability of communications between airlines and travel agents and is open to any third party, intermediary, IT provider or non-IATA member, to implement and use.

NDC transition is underway, which means this will see more one time project spending on transition, which benefits Accelya and the other existing players. Accelya has already started working on NDC implementation, plus they’re getting more allied work. For example, one of their big customers, American Airlines engaged them on a different project to support sale of unused EDIFACT tickets exchangeable through NDC connections 3. For reference – EDIFACT is the old standard and NDC is the new standard.

Resources to understand NDC and ONE Order –

Interesting times for a monopoly player that has been sleeping for years!

CarTrade Tech – A Multi-Channel Auto Platform (16-08-2023)

Now, they have given more details on acquisition. It’s not that bad as it also include whole OLX classified (buy- sell for all other items than cars) so tech and products are good but I have only one questions after years of trying to make this work (if i remember correctly OLX has invented whole buying selling of second hand things (Olx (OnLine Exchange) was founded around 2006 as per google) and still revenue is only 177 crs (though 111 crs profit before product and tech cost) and it had one of the best backer of tech company (Prosus) and still they could not scale much. Now current management did not build most things as they have acquired most of the business.

They have also schedule concall on Monday for the same. Not sure if this has been planned after mail or they were planning to do it after closing transactions.

Thanks!

EPL – Essential Packaging Company (16-08-2023)

Hi,

The incumbent CFO, Amit Jain, has been in the company for over a decade. He went from a GM level position to CFO, and has served under both, the Essel group management and Blackstone. The new CFO, Deepak Goyal comes from a Pepsico background, last served Oyo as the CFO, has good experience in FMCG and M&A.

*Deepak Goyal’s Background: *

Mr. Deepak Goyal brings in about 22 years of experience across various industries including Consumer, Financial services and Hospitality tech.

In his earlier assignment, Mr. Deepak has served as the CFO of OYO Vacation Homes, one of the largest vacation home rental businesses in Europe. He successfully navigated the business through COVID-19 crisis, improved revenue realization, optimized cost structures, and enhanced overall profitability. Deepak also led multiple M&A initiatives for the company.

Prior to OYO, Deepak had spent 15 years at PepsiCo across multiple roles including Strategy, FP&A, Controllership, Operations finance and Commercial finance. ln his last role at PepsiCo, Deepak was the Category & Commercial Finance Director where he spearheaded strategic initiative to gain market share in potato chips segment, while maintaining profitability.

–

Spoke to a friend who works at a senior position in Oyo. This is what he had to say:

“On Deepak’s feedback, have heard good things about him after speaking to 3-4 folks over the last couple of days. He is super informed, driven,high sense of ownership and details oriented and had a good rapport with colleagues and sub-ordinates alike. Overall a well rounded personality.

I haven’t worked with him directly as he was heading Finance here for the Vacation Homes business in Europe where I wasn’t involved much .

But have heard good things about him only. I believe he was let go because of our cost structuring mode these days.”

Hope this helps clear all doubts.

Nithin’s Portfolio (16-08-2023)

There is a change in my PF

As its over a 2-3 month journey to really test my hypothesis of sectoral rotation with 15% of capital – I fairly do understand this is not my cup of tea or I would need to be better at it (Mentally).

Here are the key mistake

- Macro factors contribute much to sector – its not just companies, even if the company gives excellent result, there needs to a good background music for the stocks to dance

- You need to know fundamental, triggers, technical, momentum across multiple sectors & companies and be on toes to find out what’s the driving triggers – well this is not my cup of tea.

- I did wait for as long as 1-2 months in SECTORAL PF just to see that my CORE PF is risen about 30% and I could not just wait to sit in SECTORAL PF to just throw pebble in the pond and wait for something to happen.

- There will be a inverse ratio between the sectors too my observation when Chemicals/Pharma are at all time High the Banks would be on the opposite end now since my CORE PF is more inclined towards sunrise sector (Chemical/Pharma) in next 2-3 quarters making new moves is not advisable.

- Now if you find the running tiger you can invest big and make handsome returns in short term – and your PF may look temporarily well : but this is just a mental tickle for short term, what people miss the most is long term compounding. For example short term noise such as HPL Power, BIRLA Cable, APAR had made good returns however if I had been in that area of noise then I would miss NEULAND

- Now why emphasize long term compounding? has this happen before? will this happen going ahead? how sure are we on the right boat?

From most of the interview example : https://www.youtube.com/watch?v=8Y7BqPMIbA4 Uthpal & Ramesh Damani who are market veteran – their experience tells us that investing should be long term & secondly allocation. - Why I did not invest in Banks?

- Honest : I did not knew what was happening there

What did I Miss?

- Capital Goods

- Industry tools especially Mining

What I cannot afford to Miss?

- Pharma : Contract Manufacturing Opportunities

- Chemical – Specialty Chemical Opportunities mainly in Sulphur, Flavors & Fragrance, Agrochemical, Nutrition

- Banks especially – Small Finance Banks

- Consumption : Staple & Discretionary

- Telecommunication : Cloud | 5G

- Energy : Bio | Green Energy via Fluorination proxy

- Defense : Drone, Radar & Sonar

- IT sector : SAAS, Data Engineering especially Cloud, ERP Solutions on Cloud.

- Finance : I don’t know who are good here

- Railway : Exited HBL Power due to valuation :

- Fluorochem : Multiple applications

- Real Estate theme via – Home Improvement

Any themes that am missing here?

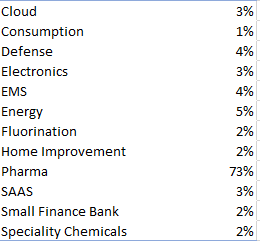

Here is the current snapshot of my PF

| Serial | Stock Name | Buy Price | CMP | Weightage | Return | Holding Days |

|---|---|---|---|---|---|---|

| 1 | LAURUSLABS | 344.2 | 387.75 | 43% | 12.65% | 15 |

| 2 | NEULANDLAB | 2100.01 | 4082.65 | 14% | 94.41% | 202 |

| 3 | SYNGENE | 682.35 | 799.5 | 11% | 17.17% | 174 |

| 4 | PRAJIND | 296.41 | 465.5 | 5% | 57.05% | 274 |

| 5 | AXISCADES | 452.44 | 579.7 | 4% | 28.13% | 89 |

| 6 | SYRMA | 346.72 | 455.95 | 4% | 31.50% | 139 |

| 7 | NEWGEN | 499.57 | 918.2 | 3% | 83.80% | 101 |

| 8 | SBCL | 146.02 | 537.15 | 3% | 267.86% | 174 |

| 9 | MASTEK | 2156.36 | 2173.1 | 2% | 0.78% | 0 |

| 10 | ORCHIDPHAR | 592.57 | 544 | 2% | -8.20% | 74 |

| 11 | DMCC | 308.19 | 308.6 | 2% | 0.13% | 124 |

| 12 | FLUOROCHEM | 2838.79 | 2825 | 2% | -0.49% | 13 |

| 13 | PATANJALI | 1306.83 | 1303.1 | 1% | -0.29% | 0 |

| 14 | SADHNANIQ | 85.47 | 85.15 | 1% | -0.37% | 117 |

| 15 | SIRCA | 365.31 | 404.5 | 1% | 10.73% | 97 |

| 16 | KAMOPAINTS | 175.25 | 174 | 1% | -0.71% | 0 |

| 17 | GUFICBIO | 274.08 | 280.1 | 1% | 2.20% | 15 |

| 18 | UJJIVAN | 517.1 | 514 | 1% | -0.60% | 15 |

| 19 | EQUITASBNK | 87.86 | 85 | 1% | -3.26% | 15 |

| 20 | JUBLPHARMA | 432.33 | 455.5 | 1% | 5.36% | 13 |

| 21 | TATACOMM | 1691.95 | 1698.8 | 1% | 0.40% | 0 |

Owning in Family PF :

| Story | Stock Name | Buy Price | CMP | Weightage | Return |

|---|---|---|---|---|---|

| Banks | IDFCFIRSTB | 36 | 88 | 1% | 144% |

| Consumer Discretionary | TATACONSUMER | 330 | 838.1 | 1% | 154% |

Sectoral Weights

Next Planned Move : This will be not like a slice of cake – It can never be the case that as I mention so shall that it will happen but am keeping my mental notes here :

- I have allocated high towards Pharma as the total Pharma Index is on move, with LAURUS being on 43% weightage on my Portfolio – expecting the next quarter to be slightly better – if price takes off to about 70-80% from the current holding levels, I will gradually reduce it to 20%

- Expecting Fluorination & Specialty to do well after that – so will allocate more to it later on the run

- Banks usually one needs to concise about current NPA and needs a careful watch

Planning for SIP :

Consumption Staple :

- Patanjali

Fluorination :

- Fluorochem

Energy :

- Praj

Pharma :

- Syngene

5G Telecommunication | Cloud | Datacenter :

- Tatacommunication

Banks

- Equites | IDFC

Consumption Discretionary

- Tata Consumer

Things that am interested

Consumer Discretionary :

- Titan : Brand exclusivity

- Manorama for Shea Butter

- Tata Consumer

- Metro Brands

- Brand Concepts

Speciality Chemicals

- Aether

- Privi

- Fairchem

Large Banks

- HDFC

Insurance

- Star Health

- PBFintech

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (16-08-2023)

I am not able to understand the deviance between industry dynamics and performance of Satia and West Coast Papers. As per industry reviews in links below, there is exptected downturn in industry and mill are being shut down. Any company operating in commodity business cannot outperform industry dynamics for long. But contrary Satia/ West Coast is improving sales/financial performance (?!)

Any thoughts on this?