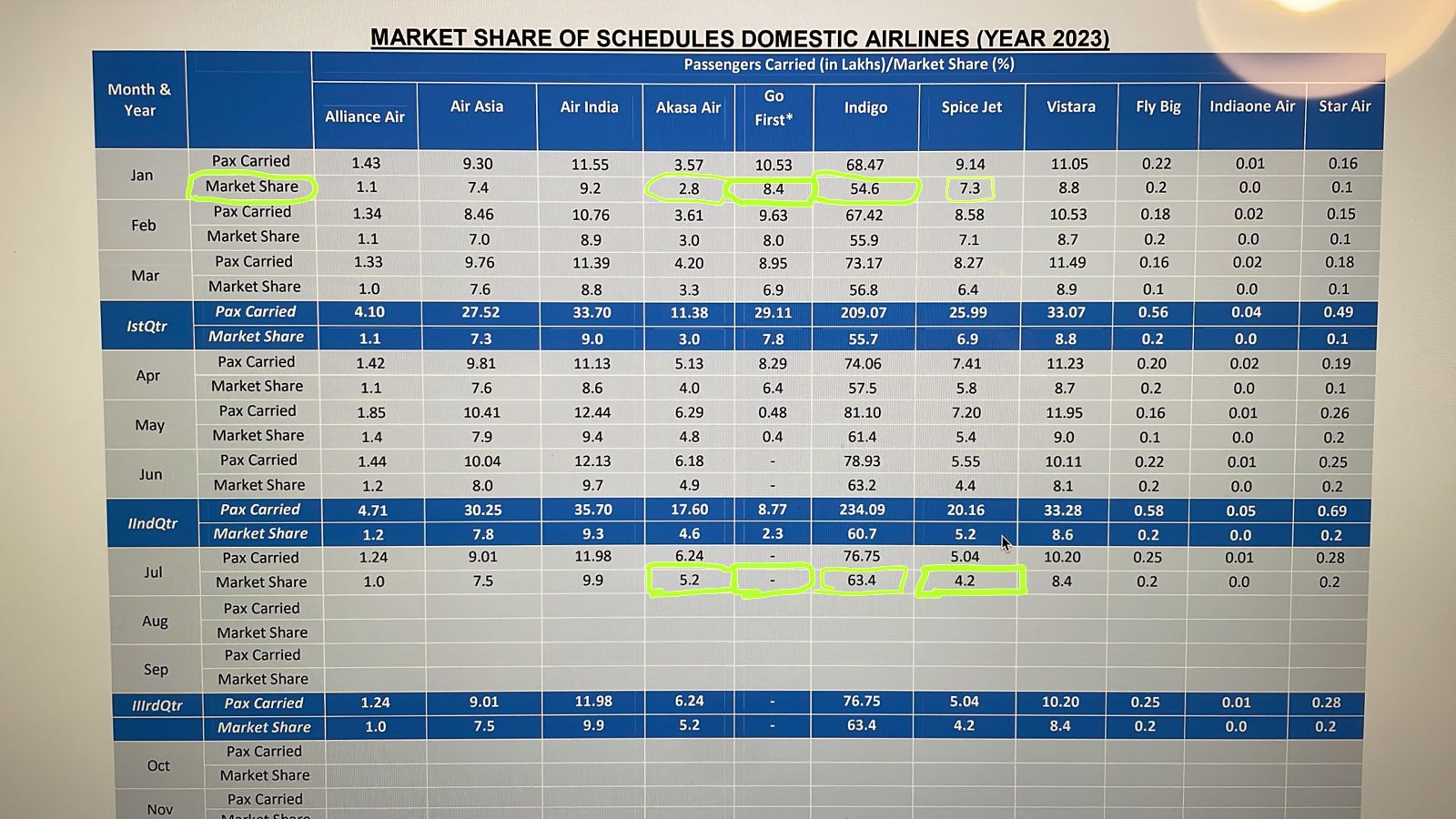

In the continuing Lollapalooza monologues-

Since the year began 11.5% market share has been ceded by GO(gone) & Masala Air. IndiGo vacuumed 8.8% & Akasa almost doubled its share.

In the continuing Lollapalooza monologues-

Since the year began 11.5% market share has been ceded by GO(gone) & Masala Air. IndiGo vacuumed 8.8% & Akasa almost doubled its share.

Tata Communications :

Summary of Q1 FY24 Earnings Call:

Strategy & Future Plans :

Financial Performance:

Business Segment Performance:

Subsidiaries Performance:

Margins and Profitability:

UCAAS : Unified Communications (Current Growth Driver)

Digital Portfolio and Growth:

CS : Connected Solutions

Media Segment Performance:

Tata Communications MOVE Platform:

Cloud

Cloud and Security Offerings:

Q&A Highlights:

Employee Count, Margins, and M&A:

Future Margin Expectations:

Aspirations for Revenue and Revenue Mix:

Sentiment Analysis:

Disc : Studying

Tata Communications :

Summary of Q1 FY24 Earnings Call:

Strategy & Future Plans :

Financial Performance:

Business Segment Performance:

Subsidiaries Performance:

Margins and Profitability:

UCAAS : Unified Communications (Current Growth Driver)

Digital Portfolio and Growth:

CS : Connected Solutions

Media Segment Performance:

Tata Communications MOVE Platform:

Cloud

Cloud and Security Offerings:

Q&A Highlights:

Employee Count, Margins, and M&A:

Future Margin Expectations:

Aspirations for Revenue and Revenue Mix:

Sentiment Analysis:

Disc : Studying

Looks like their capex is completely going into bulk manufacturing and they are not able to grow their IMFL segment even with a smaller base, only 5% growth is just not enough, unless and until they can’t ramp up the pace, I don’t think they deserve the valuation they have.

Disc: Exited today. Will see, what mngmt. will say in the concall.

Looks like their capex is completely going into bulk manufacturing and they are not able to grow their IMFL segment even with a smaller base, only 5% growth is just not enough, unless and until they can’t ramp up the pace, I don’t think they deserve the valuation they have.

Disc: Exited today. Will see, what mngmt. will say in the concall.

One more quarter Q24 with very good results … any insight any one have … con call in awaited for Jun Q … waiting to hear management commentry

One more quarter Q24 with very good results … any insight any one have … con call in awaited for Jun Q … waiting to hear management commentry

EIH Q1 concall highlights –

Sales- 498 vs 394 cr

EBITDA- 155 vs 97 cr ( margins at 31 vs 25 pc )

PAT- 106 vs 66 cr

Q1 occupancy rates at 70 pc. Corporate segment doing well

F&B revenues – 169 vs 163 cr

Flight catering and airport lounge revenues – 87 vs 45 cr

Net Cash position at 540 cr

Current corporate structure –

International Hotels- 07 ( All Oberoi Hotels, 05 owned, 02 managed )

Domestic Managed hotels by EIH- 06

Domestic Oberoi hotels- 06

Domestic Trident hotels- 03

EIH associated Hotels- 02 Oberoi + 07 Trident – all managed

Expansion plans for FY 24 – 02 hotels – 01 Vilas Hotel in MP ( 20 rooms ), 01 Rajgarh Palace also in MP ( 65 rooms )

LY – ROCE was 35 pc for owned Hotels, that’s where company’s focus continues to be

Currently do not have a beach front Hotel in India

As per capita income rises, will open the same. Also have a Site avlb with the company in Goa

Most of company’s overseas hotels are on the beachfront

Company gets a lot of its revenues from Intl travellers which often happens in Q3,Q4

Corporate ARRs are up 10 pc yoy

Have opened a new standalone restaurant and club. Initial response for both has been very strong

Company to soon share its detailed growth plan blueprint till 2030

Unlikely to take Debt/Equity beyond 0.2 to fund all expansions

ARRs in India for luxury hotels are a fraction vs international rates. As affluence in India grows, ARRs can only head higher. This shall also reduce seasonality as dependence on foreign tourists comes down

Company believes, the upcycle in Hospitality industry can last > 4-5 Yrs

One example-Oberoi New Delhi operates at ARR of around $200-250/night. Any comparable hotel in the west is not avlb at ARR< $ 1500-1800/night. Hence the headroom for ARRs in Indian luxury space is humungous

Imagine what will happen to profitability if ARR crosses $ 300/night !!!

Even Intl Oberoi hotels are averaging >$ 500 ARR/night

F&B revenues in Q1 were flattish as Oberoi Nariman Point drives a lot of banquet sales & most of its banquet rooms were under renovation. Will open in Nov 23

Moto GP Noida, World Cup, G-20 meet should add to demand this yr

Flight catering is shaping up well, growth prospects are strong

Company believes,there is enough space for growth in ultra luxury segment. Hence, not planning to venture into premium space by launching a new brand etc

Plus there is lesser competition here vs plain 5 star hotels

Disc: holding both EIH, EIH associated hotels. Biased

As to why it was sold at a price it was sold, looks like the deal would have been made a month or two in advance. That’s a guess.

Titan Eyecare, a division of Titan Company, has forayed into a new vertical with the launch of its audiology segment in partnership with WS Audiology.

.

As part of this collaboration, Titan has set up diagnostic tests at select stores aimed at assessing hearing capabilities and recommending suitable hearing aids (if needed).

.

Having specialised in optometry for the past 15 years, Saumen Bhaumik, CEO of Eyecare Division at Titan Company explained that the company’s research extended to other sensory organs, such as the ears. The amalgamation of audiology and optometry has demonstrated success stories, and certain progressive regions globally have already entered this domain, he added.