Google reviews are probably not that reliable in this case. Royal care probably does a better job of getting their patients to leave a review than KMCH. The number of reviews seem to be too small to make the average rating reliable.

Posts in category Value Pickr

Ambika Cotton Mills (14-08-2023)

An interesting case of this company with the honest promoter having nearly 800 cr Mcap, 400 cr inventory and nearly 300 cr cash or equivalent, is this company available for free of cast? Disc invested.

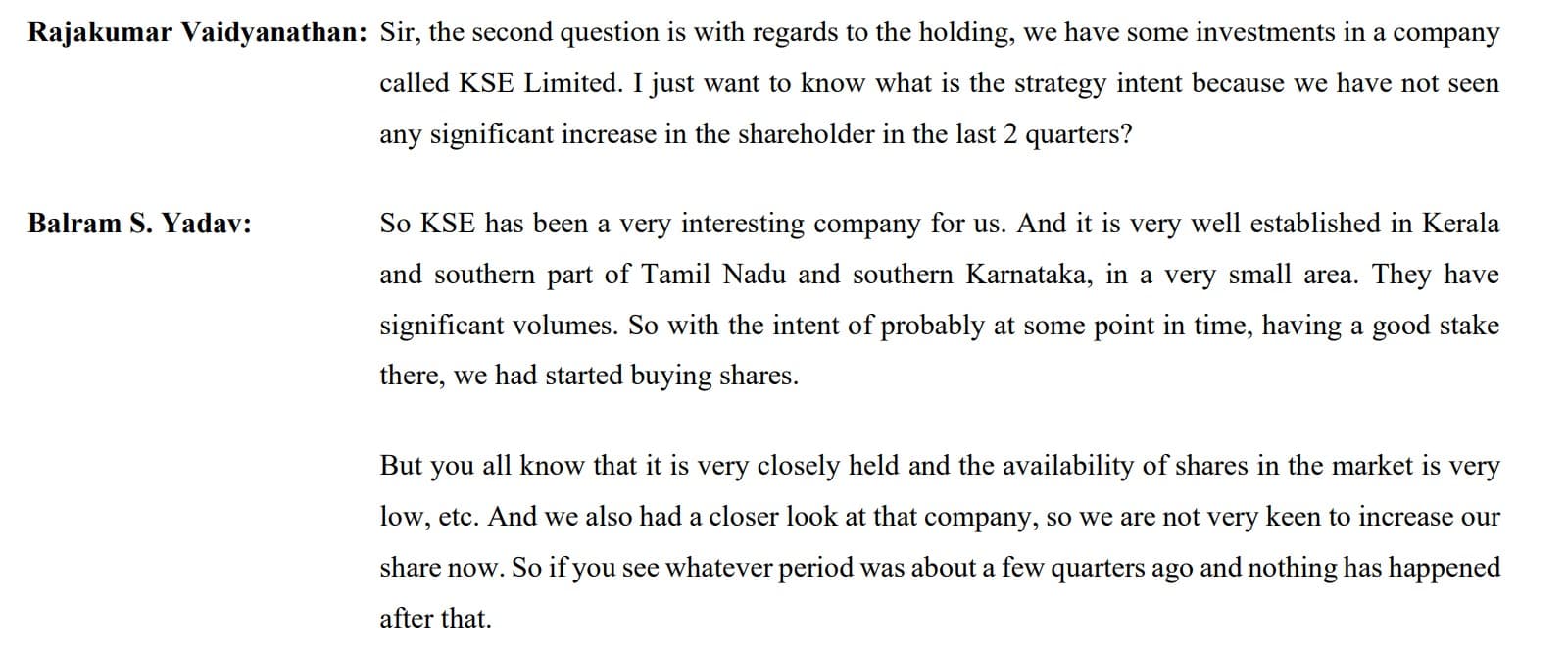

KSE Limited — Interesting Business (14-08-2023)

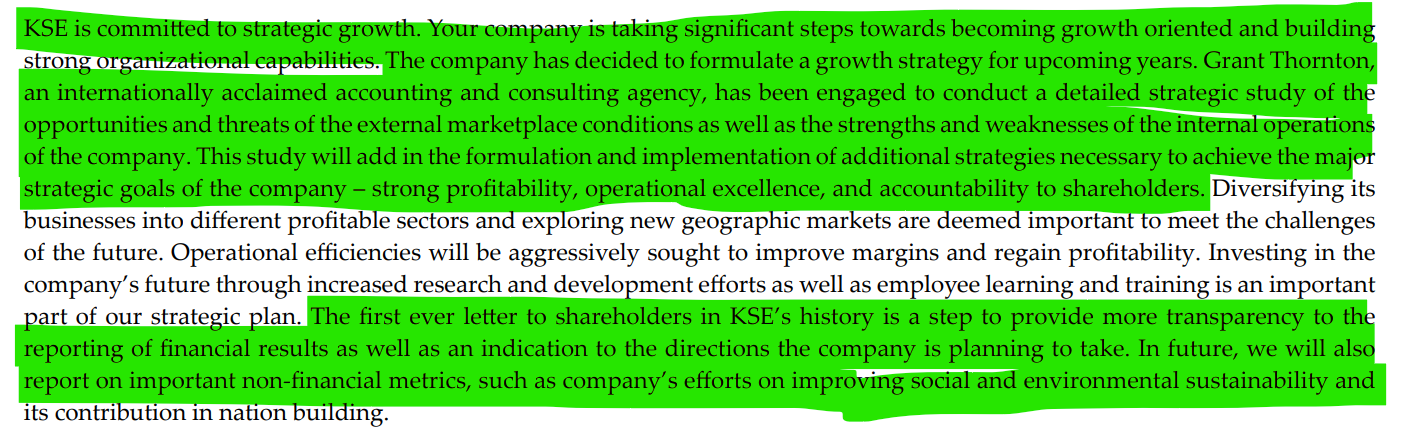

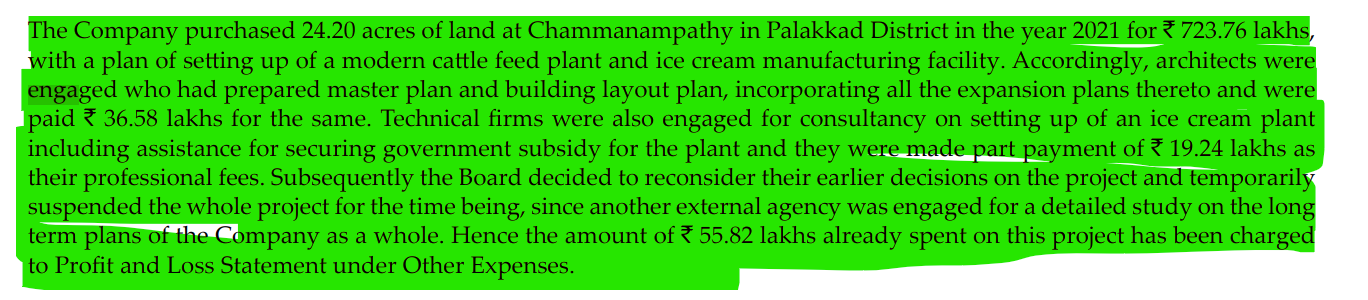

Some excerpts from 2023 Annual report – 2023 – https://www.bseindia.com/xml-data/corpfiling/AttachLive/88e75776-48ce-41ee-abbd-a28393521d8f.pdf

MD interview (bit outdated – 2022)

Disc: Invested

KSE Limited — Interesting Business (14-08-2023)

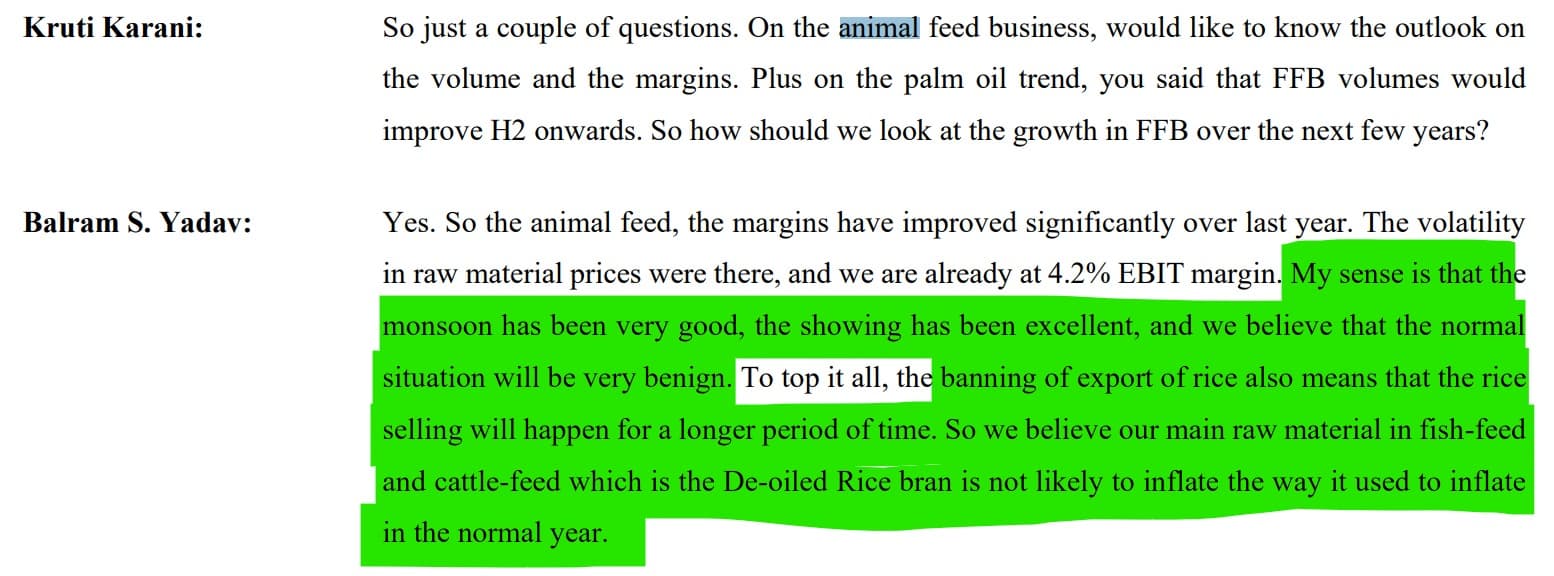

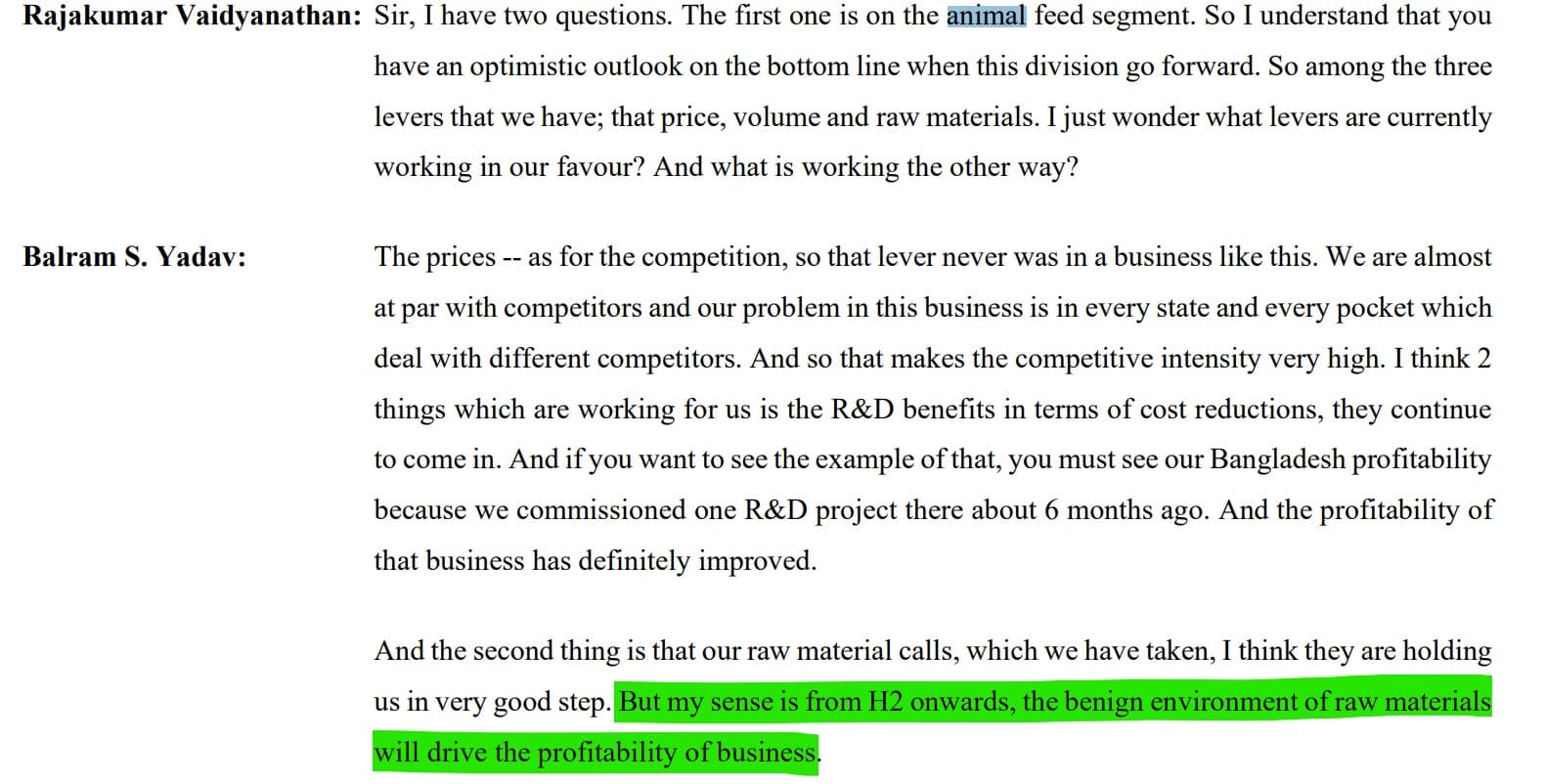

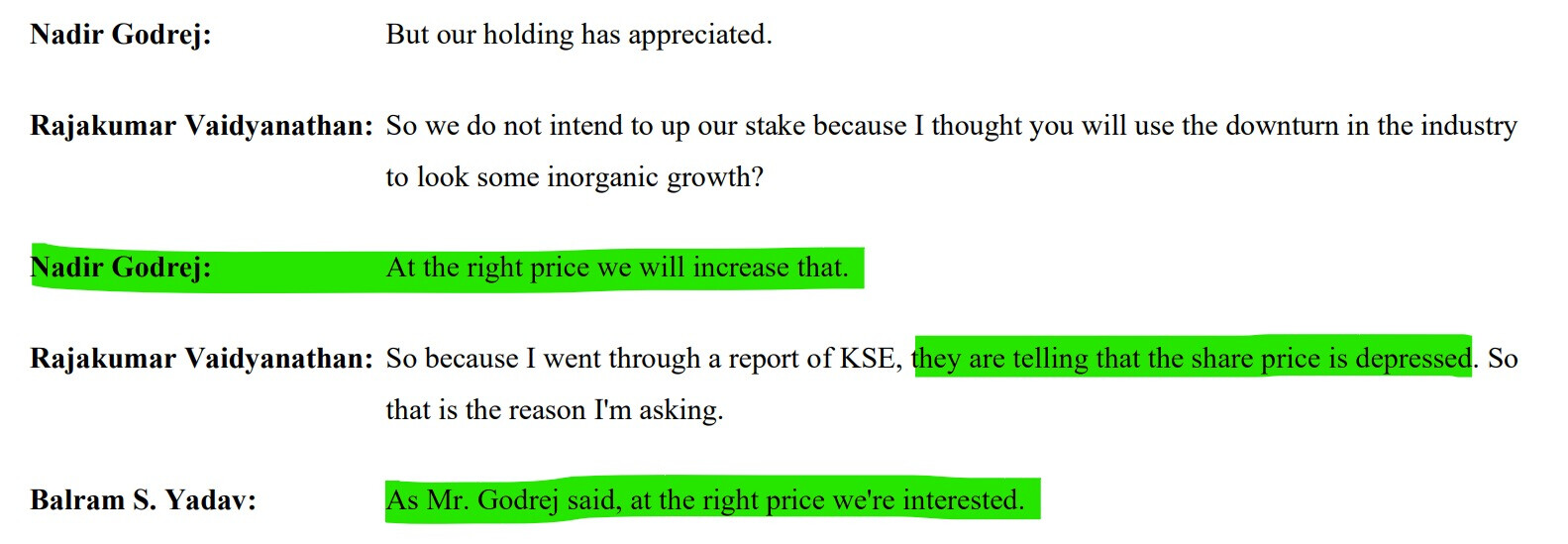

In Q1-FY24, cattle feed segment has turned profitable. As the company doesn’t do any concalls, we could get some insights from Godrej Agrovet concall.

Few excerpts from concall:

Godrej Agrovet talking about increasing stake in KSE Ltd

E2E Networks Ltd – Listed small Cloud computing player (14-08-2023)

Result for Q1 is out. Drastic jump in net profit due to lower depreciation amortization cost. Would like to view detailed notes on the cause of drop.

This has resulted in PAT and EPS to jump drastically. Projected PE for FY 23-24 based on Q1 now sits at just 17. It would depend a lot on whether the lower depreciation amortization cost is a one off or a reset.

Unfortunately, company’s also been put in ESM stage 2 list. So, 2% band and periodic call auction. Unclear to me whether it’ll be traded one day a week or everyday but just in time slots. First investment entering ESM 2.

Interestingly, company m-cap was around 467 cr yesterday and ESM stage 2 can only be applied on cos below 500 cr m-cap.

StageInvesting +Elliot Waves (14-08-2023)

Wave 3 cannot be smallest wave as compared to wave 1 and 5, so initially one can assume it will be at least be equal to wave 1.

This is another novice trying to explain.

Regards

StageInvesting +Elliot Waves (14-08-2023)

Hi @StageInvesting – Could you please elaborate on the special situation with Aarti Pharmlabs? I know it is demerger but what is the special situation here and what is the rationale for trading/ investing?

Gufic BioSciences Ltd (14-08-2023)

Q1-FY2024 call notes

- Indian first then world – better magins

- Criticare and exports growth this year – will drive 15-20% EBITDA growth

- Capacity in navasari will be finished by end of 2024

- Healthcare mkt is 2.1Lcr and will grow to 7-8L cr in 9 years . Even if international market goes for a toss, Domestic market will have enough demand for us.

- Capex and running cost most imp for any plant

- Expertise and exp in lyophilised is will allow us to handle the HUGE capacity inc

- 35% cap utilisation in Penem block

- Interest costs on capex have pulled down margins

- R&D focus: Biologics in vaccine and new botulinum drug delivery systems

- Criticare:

- made a comeback

- Handling all New age infectives

- Microcare – secondary line of oncology therapy

- Primacare- rural

- Increasing addressable mkt by new products^

- RM sensitive products (Sparsh too). Growth therefore should be judged by volumes not profits. Last year prices were really volatile

- 10-15% growth in value due to eventual erosion of prices and 30% growth in volumes

- Penem advantage

- Capacity is 40% of indian need (UNSURE if I heard that right)

- Lots of players produce powder penems but Gufic is unique as we have dual chamber bag, lyophilisation and powder filling machines. So offering is unique.

- Dedicated block at navsari unlike others.

- Will do backward integration to make bags as well for dual chamber bag

- R&D thought process: 4-5 core competencies in therapeutic, data analytics and medical experts forcast disruptive cahnge in 5-10 years. Info is international mkt. Try to create USPs like drug delivery systems . Back it up with with other factors: see what projects go off patents, new disruption, price pain points. Infra, marketing, sales must offer support to new products.

- In 3-5 years we bring down the cost to make the product affordable. Scale brings in financial viability.

- Indore will be the only major capex in next 2-3 years.

- 1024 docs have used Stunnox since launch 24 months ago

- GC margin in CMO: 30%

- GC 55% own business margin

- While one who controls API rules but Pricing in API is eroding so we are evaluating whether to drive deeper there or be happy with what we have.

Personal comment:

CEO Pranav is well versed with the pharma knowledge, strategy, and qualitative aspects of opportunities they are chasing. He refers Mr Rongta (CFO perhaps) for all questions that involve quantitative aspects. (No comments or judgement. Just an observation)

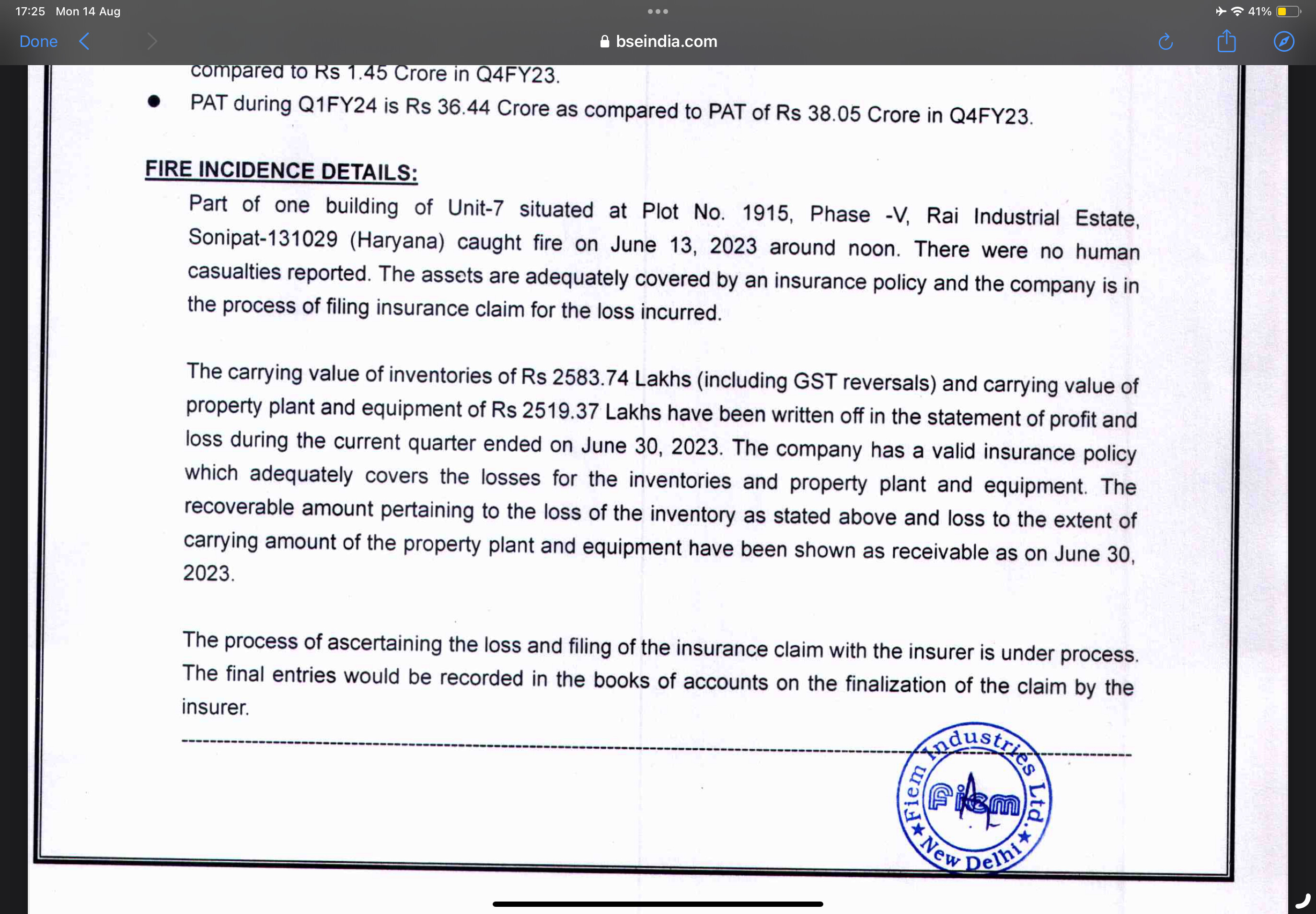

FIEM industries : auto ancillary player (14-08-2023)

Much of the components of PnL looks muted YoY, there was a fire incident, and insurance has covered it based on the details provided

Gujarat Automotive Gears – Play on auto anciliary (14-08-2023)

Hi harsh, Im sorry but I’m not tracking this company currently and its been long since i left following it so it would not be appropriate if i comment anything on it.