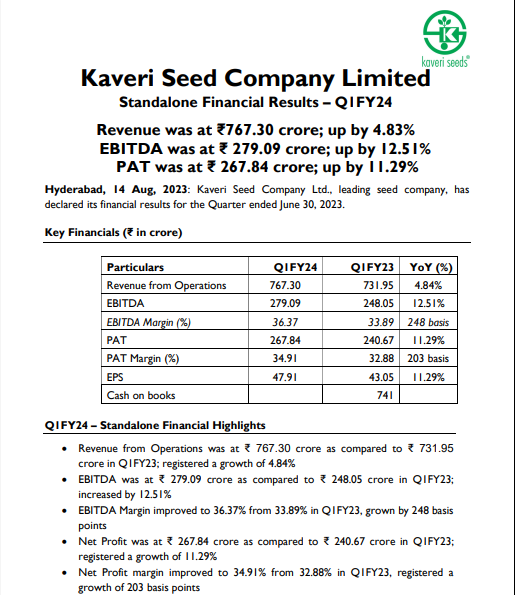

Quarterly results

Quarterly results

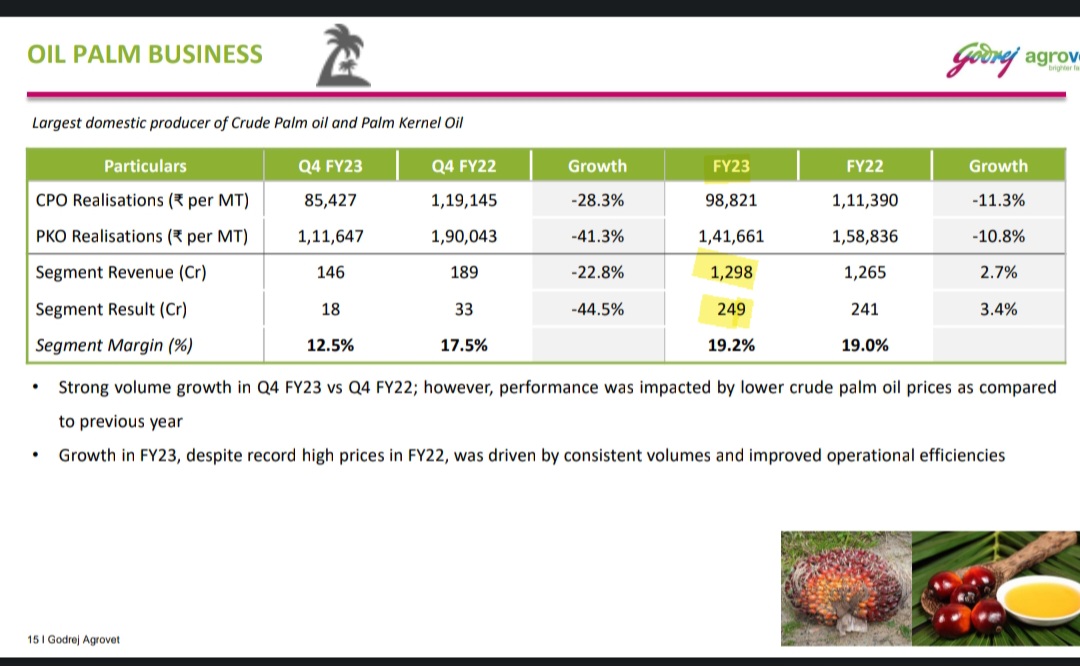

Godrej Agrovet

On Palm oil business – some interesting stats – from their concall.

Their existing Palm oil plantation of about 25k to 30k Hector

(45k Hector in total, but 60% mature )

This year Palm oil revenue: 1300 Cr, PAT of 249 Cr.

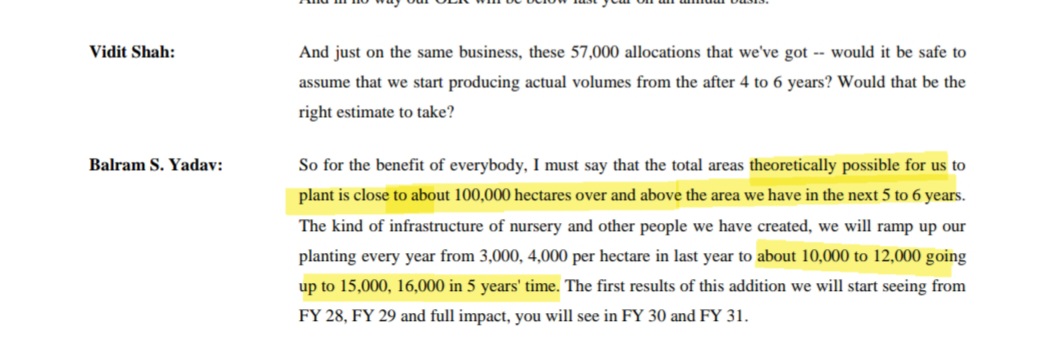

From new allocation ( in Odisha & Telangana )=Theoratically possible Plantation is close to 100k Hector

That’s about 4X from current levels ( 25-30 k Hector ) in next 5-6 year…

Moreover, Goverment is encouraging more palmoil production at home and thus, in my view, this allocation of land MAY increase going forward as well…

All in all, I am expecting significant jump in revenues from palm oil business going forward. Obviously not in short term but in long term.

Disc: Invested, biased views

@hitesh2710 bhai,

Can you share your views on Glenmark Life science (GLS)?

The company was listed two years back and haven’t crossed the IPO price yet. However, after making a low of around 360 in March 2023, the stock has run up close to 70% in 3-4 months. Results of last two quarters have been really good for both generic API and CDMO division of their business. They have been reporting good and consistent margins around 30% and with falling raw material prices the management is confident of maintaining the margins at least for this year.

Even after the recent run up the stock seems to be reasonably priced with Mcap/sales around 3 and PE around 16. Parent company Glenmark pharma is in talks with investor to sell their holdings.

Appreciate if you can share your views.

Regards,

Suhag

I understood the true meaning of this in 2023, thanks for this Sir

After the bull run of 2023

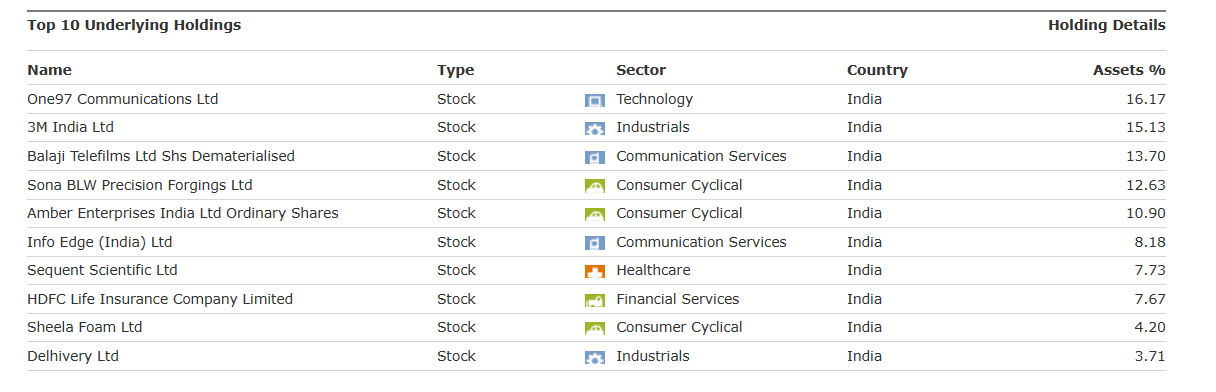

This is the long term portfolio of ASK

(post deleted by author)

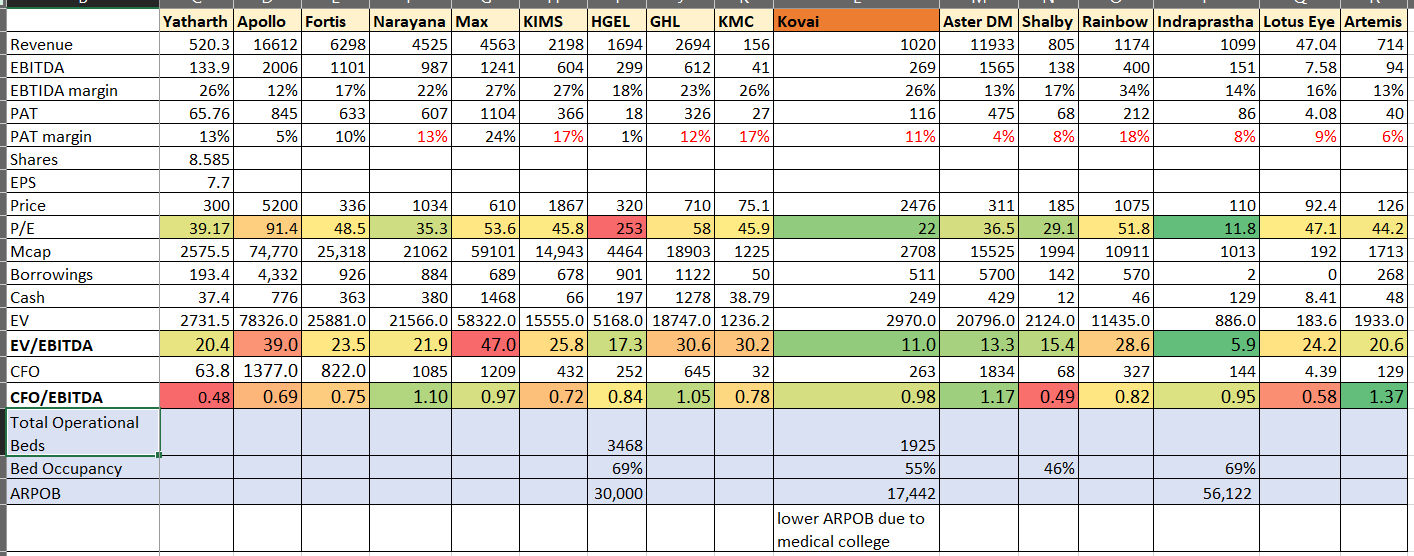

Thankful for the detailed analysis and notes mentioned above. Had done a small analysis on various hospitals during Yatharth’s IPO.

Considering the run-up of various hospitals, Kovai is the only one that seems reasonably priced. Indraprastha is stuck in legal issues considering their agreement with Delhi govt. for providing free-of-cost treatment in lieu of lease of hospital land.

Note: Data is from early Aug for other hospitals

The only issues I can see are:

Pros:

Happy to get feedback, insights from other people

Disc: Invested and averaging down

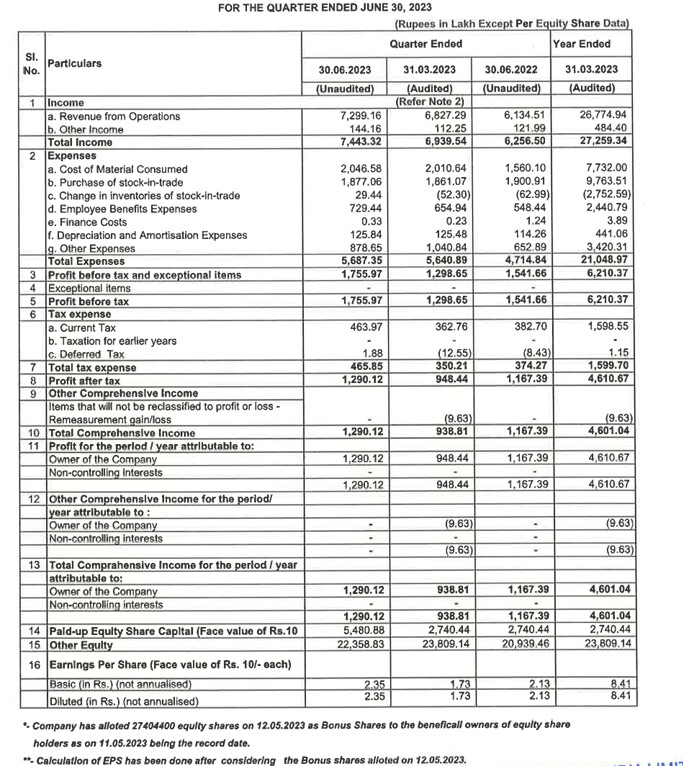

Good set of numbers.

Q2- 2024…investor presentattion

1…The US and UK economies have shown signs of improvement; inflationary pressures are gradually easing. However,

cautious consumption patterns persist due to precautionary measures. Meanwhile, Europe remains a point of

concern. Overall, the order book has improved and should result in positive impact on revenues from hereon

2…Destocking of Inventory in the

channel led to lower revenue

in FY23 compared to FY22

3…We are currently experiencing delays in machinery procurement, which has affected the timeline for commercializing the

first phase of the appliance

division. We now estimate this to take place in early H2FY24.

4…Looking towards our long-term goal, we aim to achieve Rs. 1,000 cr. in revenue by FY25. In addition to our strong position

in quartz sinks, we believe that steel sinks and the appliance division will play vital roles in accomplishing this objective.”

5…Commercial production of additional steel sinks capacity, commenced in July’23, bringing the total capacity to

1,80,000 units P.A

6…Acquisition of 43,379 sq. mt. additional land in Bhavnagar, Gujarat for Rs. ~9.07 cr for future expansion & new

projects if any

7…q1 2024

45%@Quartz sinks

30% appliances

11% steel sinks

8…We have expanded to

newer geographies –

Australia, New Zealand,

Gulf countries, Southeast

Asia, China, Singapore,

Turkey, Vietnam

❖ Witnessing huge traction in

business from these

geographies

9…Acqusiition and cross selling opportunity

•The acquisition of 100% stake in a

distribution company : Homestyle

Product Limited, in UK which outsources

sinks and sells to the top customers

• Another acquisition in UK : Tickford

Orange Limited, holding company of its

operating subsidiary ’Sylmar

Technology’. Leading player in UK solid

surface market

• Tap Factory acquisition.

• Vital access to key customers based in

markets in Europe and UK

• Current Domestic Market : 3200+

Dealers, 85 Galleries & 82 distributors

10…FUTURE GROWTH DRIVER

A…Strong Distribution Network

Strengthen the Distribution network by tie up with Homestyle and STL, UK and

plan to add new 100 galleries and 34 more distributor and increased dealer

network to 3200+ dealers in Q1FY24

B…Branding

Focused on capturing the Brand Mindspace of niche Consumers

C…New products

Entry into the kitchen appliances and bathware market with innovation, R&D and design

capabilities – Aim to become a major player

D…Export

Currently catering to 55+ countries strive to spread the wings to 70 countries in

next three years by exploring the uncatered geographies

E…Technology

… Only Quartz Sink Company

Only company in India and amongst the 4 global players manufacturing Quartz

Sinks

Disc…invested