- Company has reduced debt.

Company has delivered good profit growth of 18.7% CAGR over last 5 years

Debtor days have improved from 40.5 to 28.6 days.

Company’s median sales growth is 19.0% of last 10 years

Company’s working capital requirements have reduced from 57.5 days to 35.0 days - PE and PB very low. Very lucrative price and consistently making profit.

- Its chemical industry and very fluctuating profits due to demand and supply concerns. But it is giving profit consistently every year.

- Margin Volatility: The company’s operating margin remains volatile due to the supply issues of hydrofluosilicic acid. It procures it from distant sources, resulting in higher costs that periodically increase due to rising fuel prices.

- Client Concentration: In FY24, revenue from the top customer made up about 53% of total revenue, up from 39% in FY22. The second top customer contributed 23% in FY24, down from 38% in FY22.

- Geographical Split:

Odisha: 61% in FY24 vs 58% in FY22

Chhattisgarh: 23% in FY24 vs 13% in FY22

Madhya Pradesh: 12% in FY24 vs ~14% in FY22

Others: 4% in FY24 vs 15% in FY22 - Raw Material Arrangement

The top raw materials consumed by the company are Alumina Hydrate (~57%), and Hydrofluosilicic Acid (23%). - Its quarterly result of Jun 2024 was not good. Looking at the past trend, it seems Q1 of FY are cyclically down. Does it mean its good price to enter this stock before its Q2 result. Please provide your thoughts about this stock. Not an expert of the chemicals this Company deals with and this stock is falling so much.

Posts in category Value Pickr

Alufluride Limted (06-10-2024)

Happiest Minds Technology (06-10-2024)

There are better companies in market to invest than Happiest Minds. Its just not promising enough to put your money on. They werent able to give any returns for past 3 years. Infact I am in 30% loss. And as soon as stock tried to take stance at 900 Rs price, the Founder sold the stock and pushed it to 700s.

i think in 2 years the stock may again reach to 1000 and by then it will be time for Soota to sell another portion of its stock as stated by him. And boom! back to 700s. So for a good half decade this stock is going to give returns less than inflation.

Curious Case of Coal India (06-10-2024)

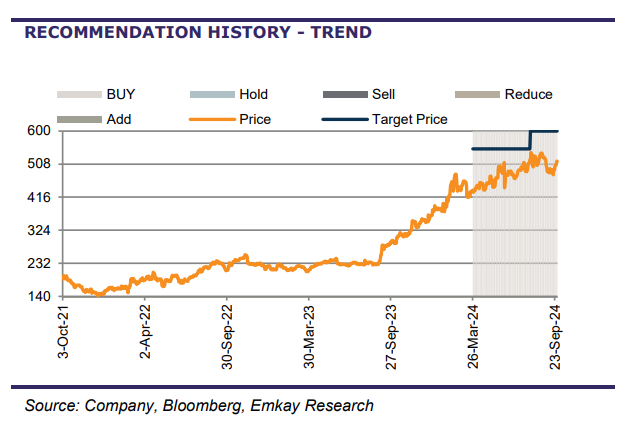

Emkay Research: Buy | TP 600 Rs. (Oct 1 Report)

“Coal India’s production volumes tend to be seasonal with the second quarter of any fiscal year softer than the rest of the quarters. The seasonality factor has averaged 41.4%/58.6% for 1H/2H, historically . Essentially, the production of 341mt in 1H implies full-year production of 825mt adjusted for seasonality , which is marginally lower than our estimate of 830mt and the company’s guidance of 838mt for FY25.” – Emkay Research

Emkay says dont worry about productionn coming down in monsoon months. Coal India is on track to achieve its ambitious target of increased coal prodution this year. The best is yet to come. Q3 and Q4 will be better.

Companies with 20%+ growth guidance for next few years (06-10-2024)

few inputs here:

Landmark: cash conversion is inexplicably low given 36% (& growing) of Merc business is at nil inventory.

Dream folks: Interesting business but have following concerns:

- Regulatory risk: Merchant discount rates revision by RBI.

- Governance: No CFO till 2021. Further CFO is paid just 30 lakhs annually vs 3 cr+, the company’s CMD draws annually. This highlights the lack of quality talent available to the company.

- no pricing power: No scope of GM% expansion. Through operating leverage, ebitda can improve though.

- Entry barriers: Very low. Nothing proprietary as a platform. Anyone can enter, anytime.

My Portfolio: Himanshu (06-10-2024)

Hi All,

I am sharing my portfolio below and the rationale behind my investing strategy. My portfolio is inclined towards the financial sector, now I want to add options where I can diversify it properly. Also, going forward I want to generate around 17-18% returns, so I would like your suggestions on how to change my portfolio and investment strategy.

Thanks in advance.

Federal Bank – A Turnaround banking Story? (06-10-2024)

Was comparing IDFC First Bank and Federal Bank Q2 Business Updates –

Both IDFC First Bank and Federal Bank have released provisional business updates for Q2 FY25. Here’s a comparison based on available data:

Key Metrics:

| Column 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Metric | IDFC First Bank | Federal Bank | |

| Loan Growth (YoY) | 21.3% | 19.3% | |

| Deposit Growth (YoY) | 32.2% | 15.6% | |

| CASA Ratio (Sep’24) | 48.9% | 30.07% | |

| Credit Rating | AA+ Stable (CRISIL and CARE) | AAA (CRISIL) | |

IDFC First Bank (IDFCFB):

● Strong Growth: IDFCFB witnessed robust growth in both loans and deposits during Q2 FY25

●CASA Focus: The bank’s CASA deposits surged by 37.6% YoY, contributing to a higher CASA ratio. This indicates a shift towards a more favorable deposit mix.

●Legacy Debt Repayment: IDFCFB is actively raising funds to repay existing borrowings, explaining the higher deposit growth compared to loan growth.This strategy aims to improve the bank’s financial health in the long run.

●Recent Merger: The merger of IDFC Limited with IDFC First Bank concluded on October 1, 2024, resulting in zero promoter holding. This transition positions IDFCFB as an independent entity, which could influence investor perception.

Federal Bank:

●Steady Growth: Federal Bank also exhibited healthy growth in advances and deposits, though at a slightly lower rate than IDFCFB.

●Retail Focus: The bank’s internal classification reveals a higher growth rate in retail credit (23%) compared to wholesale credit (13%). This focus on retail lending could imply lower risk and potentially higher profitability.

●Stronger Credit Rating: Federal Bank currently enjoys a slightly higher credit rating of AAA from CRISIL compared to IDFCFB’s AA+ Stable. A higher credit rating suggests lower credit risk for investors.

Conclusion:

●IDFCFB’s strong growth and improving CASA ratio are positive signs, as expected legacy debt repayment and the recent merger might introduce uncertainties.

●Federal Bank’s steady performance, retail lending focus, and stronger credit rating present a more stable picture.

IDFC First Bank Limited (06-10-2024)

Was comparing IDFC First Bank and Federal Bank Q2 Business Updates

Both IDFC First Bank and Federal Bank have released provisional business updates for Q2 FY25. Here’s a comparison based on available data:

Key Metrics:

| Column 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Metric | IDFC First Bank | Federal Bank | |

| Loan Growth (YoY) | 21.3% | 19.3% | |

| Deposit Growth (YoY) | 32.2% | 15.6% | |

| CASA Ratio (Sep’24) | 48.9% | 30.07% | |

| Credit Rating | AA+ Stable (CRISIL and CARE) | AAA (CRISIL) | |

IDFC First Bank (IDFCFB):

● Strong Growth: IDFCFB witnessed robust growth in both loans and deposits during Q2 FY25

●CASA Focus: The bank’s CASA deposits surged by 37.6% YoY, contributing to a higher CASA ratio. This indicates a shift towards a more favorable deposit mix.

●Legacy Debt Repayment: IDFCFB is actively raising funds to repay existing borrowings, explaining the higher deposit growth compared to loan growth.This strategy aims to improve the bank’s financial health in the long run.

●Recent Merger: The merger of IDFC Limited with IDFC First Bank concluded on October 1, 2024, resulting in zero promoter holding. This transition positions IDFCFB as an independent entity, which could influence investor perception.

Federal Bank:

●Steady Growth: Federal Bank also exhibited healthy growth in advances and deposits, though at a slightly lower rate than IDFCFB.

●Retail Focus: The bank’s internal classification reveals a higher growth rate in retail credit (23%) compared to wholesale credit (13%). This focus on retail lending could imply lower risk and potentially higher profitability.

●Stronger Credit Rating: Federal Bank currently enjoys a slightly higher credit rating of AAA from CRISIL compared to IDFCFB’s AA+ Stable. A higher credit rating suggests lower credit risk for investors.

Conclusion:

●IDFCFB’s strong growth and improving CASA ratio are positive signs, as expected legacy debt repayment and the recent merger might introduce uncertainties.

●Federal Bank’s steady performance, retail lending focus, and stronger credit rating present a more stable picture.

Laurus Labs – Can Business Transform to Next Level? (06-10-2024)

detailed explanation. Thank you.

SG Mart- Can it successfully create a marketplace? (06-10-2024)

I totally second with Raj but even if the discussion is about the steel/Metal trading part of their business, I’d like to clarify what I meant by regulatory oversight in my prev response. Look, It’s true that basic trading in steel (e.g., buying and selling steel products) does not require any special industry-specific government approval in most cases. Any business can trade in steel as long as it is registered under GST, and follows regular business compliance procedures. But at the same time it’s important to have clear distinction between general trading and trading at scale in regulated commodities like steel.

Your statement is only true for someone who’s trading on a small scale or when the trading does not involve import, export, or large-scale infrastructure projects where regulatory frameworks come into play.

The scenario changes drastically when steel trading reaches a large scale or is linked to key infrastructure projects (such as Bharatmala, Sagarmala, Smart cities to name a few like I also mentioned above), export-import, or strategic sectors. In such cases, the steel used must meet the specifications set by relevant ministries, such as the Ministry of Road Transport and Highways or Ministry of Shipping. So for a large-scale supplier like SG Mart, they’ll certainly face additional regulatory oversight.

Also recommend reading about quality certifications like BIS registration, IEC, DGFT etc. Hope you too take the help of GPT to understand these concepts better ![]()

SG Mart- Can it successfully create a marketplace? (06-10-2024)

Look, It’s true that basic trading in steel (e.g., buying and selling steel products) does not require any special industry-specific government approval in most cases. Any business can trade in steel as long as it is registered under GST, and follows regular business compliance procedures. But at the same time it’s important to have clear distinction between general trading and trading at scale in regulated commodities like steel.

Your statement is only true for someone who’s trading on a small scale or when the trading does not involve import, export, or large-scale infrastructure projects where regulatory frameworks come into play.

The scenario changes drastically when steel trading reaches a large scale or is linked to key infrastructure projects (such as Bharatmala, Sagarmala, Smart cities to name a few like I also mentioned above), export-import, or strategic sectors. In such cases, the steel used must meet the specifications set by relevant ministries, such as the Ministry of Road Transport and Highways or Ministry of Shipping. So for a large-scale supplier like SG Mart, they’ll certainly face additional regulatory oversight.

Also recommend reading about quality certifications like BIS registration, IEC, DGFT etc. Hope you too take the help of GPT to understand these concepts better ![]()