I don’t think margins of this quarter will sustain as paper prices have started to fall as per JK concall but any way Sept margins were 20% so next quarter margins should be better than that as operational efficiencies have kicked in. In March they had paid more debt hence profit looks optically low so PE is less than 5 as of now. Avg PE is 8 as per screener and as they are trying to be efficient I think next few years should see the effect and if they maintain margins market will reward them.

Posts in category Value Pickr

Tracking the AI Disruption: Impact and Benefits for Businesses (13-08-2023)

What is the impact of Data protection Bill 2023 of Government of India on Machine learning application development?

This article delves into the challenges associated with the development of customer-centric machine learning applications due to the implementation of the Data Protection Bill 2023. The passage of this bill by the Government of India (GOI) is a significant step towards safeguarding clients’ personal data, which was much needed given the rampant mishandling and misuse of such data by companies and government bodies. However, the unintended consequence of its impact on the progress of machine learning applications cannot be ignored.

Functioning of machine learning applications requires delving into how these applications work. At the core of a machine learning application is the model, which is built using historical data. The effectiveness of the model is heavily reliant on both the quantity and quality of the data used to create it. While it is possible to create a model using synthetic data, creating the model with actual data is preferable for better functioning. The model must also be consistently trained with additional data to ensure its relevance.

Although the data used to create the model cannot be reverse-engineered to extract the original data, it cannot be disregarded that the model’s foundation lies in consumer data. The Data Protection Bill introduces two key rules that impact the process of model creation for machine learning applications. For simplification, let’s discuss this using the example of an insurance intermediary.

1. Limit the use of personal data to its intended purpose:

Under this rule, insurance intermediaries are confined to using collected personal data only for the purpose it was initially gathered. For instance, data collected to provide an insurance quote cannot be repurposed for any other objective, including the development of machine learning models. This presents a challenge wherein intermediaries would need consent from their customers’ customers to use their data for building models. Navigating this challenge for both existing and future models is a substantial hurdle, requiring careful scrutiny of the bill’s directives by legal teams. Considering that intermediaries are not using their clients’ (Agent) personal data but rather their agent’s client personal data adds a new layer of complexity. Obtaining consent across two nested levels while ensuring transparency as mandated by the bill presents a considerable challenge.

2. Delete personal data when no longer needed:

Insurance intermediaries bear the responsibility of eliminating personal data that has fulfilled its designated purpose or has become obsolete due to irrelevance, inaccuracy, or lack of necessity. Furthermore, in the event of a client’s data deletion request, intermediaries are obligated to comply. This raises the question of whether intermediaries need to revise their machine learning models by excluding the data that was originally used to create them but is no longer consented to.

If this is indeed the case, it introduces a significant shift in the dynamics of constructing and maintaining machine learning models. For instance, if an intermediary utilized my data, obtained with my consent, to develop a machine learning model, they must erase my data upon the expiration of my policy, my cessation as a client, or my request for data deletion. Should this necessitate the model’s recreation by excluding my data, such a task would demand substantial computational resources and a revised approach to data processing, model development, testing, and deployment, potentially requiring frequent periodic updates.

Ultimately, the delicate balance between data protection and the advancement of machine learning applications requires careful consideration. The path forward involves proactive adaptation to comply with the bill’s regulations while sustaining innovation in the ever-evolving landscape of machine learning.

Caplin Point Laboratories (13-08-2023)

The markets they serve is basically part of that strategy, Latin America and Africa

MSTC Ltd.: Growth through to E-Commerce (13-08-2023)

-: Order dated: 07/08/2023:-*

In the present case, the Appellant has been disputing the claim of the Respondent Bank on various grounds. The proceedings before the D.R.T. was questioned on the ground of territorial jurisdiction,

and also on the ground that the claim under the agreement between the Appellant and the Respondent could not be strictly construed as a ‘debt’ coming within the purview of the RDDB & FI Act.

The Appellant had challenged the claim of the Respondent before the civil court at Alipore. After having raised all these contentions in challenging the claim of the Respondent, it cannot be said that the mere mentioning of the claim in the balance sheets as liability would amount to an unambiguous, unequivocal or clear admission on the part of the Appellant. The notes accompanying the statements of account has to be read together with the description of the liability highlighted in the balance sheets. When the fact regarding the pendency of litigation before the D.R.T. and the Alipore court is

explained in the note attached to the balance sheets, it can definitely be not stated that the admission is unequivocal. There is no such admission in the pleadings of the Appellant. The mentioning of the

liability in the balance sheet with a rider that there is litigation pending between the Appellant and the Respondent would clarify that it is not a clear admission on the part of the Appellant. An admission can

always be explained by the party making it. In the present case, the explanation follows the purported admission. The explanation for the alleged admission in the balance sheets comes in the form of a notes attached to it. The intention for incorporating a provision to grant a decree on admission is to hasten the disposal of matters where is is no possibility of a contest arising in view of the admission. I n the instant case, the parties have been litigating for more than a decade now. Under the circumstances, I find that the Ld. Presiding Officer was not justified in admitting the recitals in the balance sheets as unequivocal admission of liability on the part of the Appellant to grant a decree on

admission. The impugned order cannot, therefore, be sustained and requires to be set aside.

Resultantly, the appeal is allowed in the impugned order of the D.R.T. dated 16/09/2017 is set aside and I.A. No. 302 of 2017 on the files of the D.R.T. is dismissed. The D.R.T. is directed to dispose of the O.A.(Original Application) as expeditiously as possible keeping in view the fact that it is more than a decade old.

DRAT Order Dtd 07.08.2023.pdf (571.4 KB)

Based on the above Judicial Pronouncement, it is highly probable that liability of Rs.221 crores in the books should be written back and considered as Income. Further the cash outflow of Rs.90 cr as an Appeal deposit should also be came back (cash inflow) to the company.

Eagerly waiting for the MSTC Management comments to the Shareholders ![]()

Steel Scrap Potential and MSTC Role

A tonne of steel scrap can save 1.1 tonne of iron ore, 630 kilogram of coking coal and 55 kg of limestone. The use of steel scrap in both major manufacturing routes (BF-BOF & DRI-EAF/IF) can substantially lower the carbon emission in the process. The Steel Scrap Recycling Policy mentions the role of steel scraps in reducing greenhouse gas emissions by 58 per cent.

In the Steel Scrap Recycling Policy 2019, the Ministry of Steel stated that as of 2019, the current supply of steel scrap is 25 million tonnes from the domestic market and 7 MT from imports. The aim of the scrap policy is to be able to harness this 7 MT from the domestic market itself to reduce dependence on imports. This would make India’s steel markets less vulnerable to global events in the sector.

The policy mentions opening 70 scrap processing centres with 300 collection and dismantling centres to fill up the gap of 7 MT. India also aims to generate steel production of about 255 MT by 2030 (according to the National Steel Policy 2017).

By that time, it is estimated that the demand for steel scrap may rise up to 70-80 MT. To meet this, India may require up to 700 scrap processing centres (shredders) that shall be fed by 2800-3000 collection and dismantling centres spread all over the country.

Potential of Steel scrap Market and MSTC share in the same (Estimation)

| Year | 2023 | 2030 | |

|---|---|---|---|

| Steel Scrap | 32 | 80 | in Millions |

| Rate | ₹ 20,000 | ₹ 30,000 | Per MT |

| Scrap Value | ₹ 64,000 | ₹ 2,40,000 | in Crores |

| MSTC Market Share % | 10% | 25% | Estimated |

| MSTC Market Share | ₹ 6,080 | ₹ 60,000 | in Crores |

| MSTC Commission% | 3% | 3% | Estimated |

| MSTC Commission | ₹ 167 | ₹ 1,800 | in Crores |

Sahil’s Portfolio (13-08-2023)

@sahil_vi -it been long you have not Posted any update on your portfolio or recent changes here …?? any specific reason?

Avalon Technologies – EMS Play with US heavy and Proxy to Clean Energy (13-08-2023)

Hi @kbsekhar

Nice write-up on the Concall with all the aspects covered.

Avalon technologies is an end to end PCB Box build company in the B2B segment.

The products of the company is applied into Clean Energy,Mobility,Transportation among others.

Just another thing to add is the Indian revenue contribution to sales would be at par in the coming years.

Company does not forsee itself foraying into the consumer durables as of now.

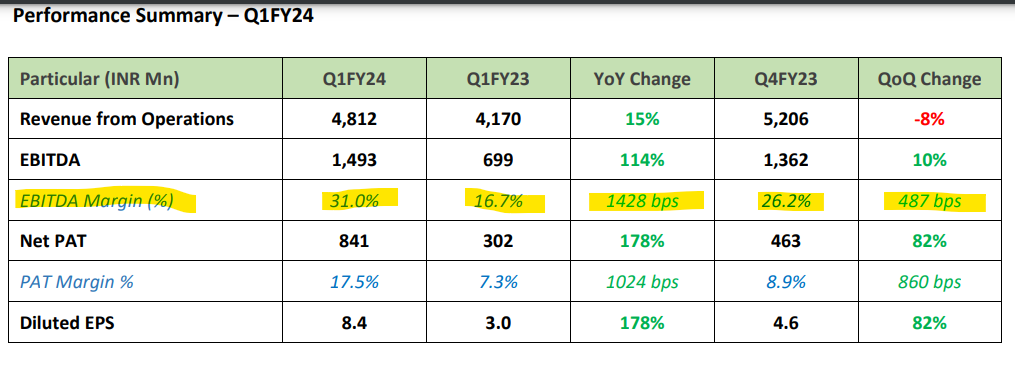

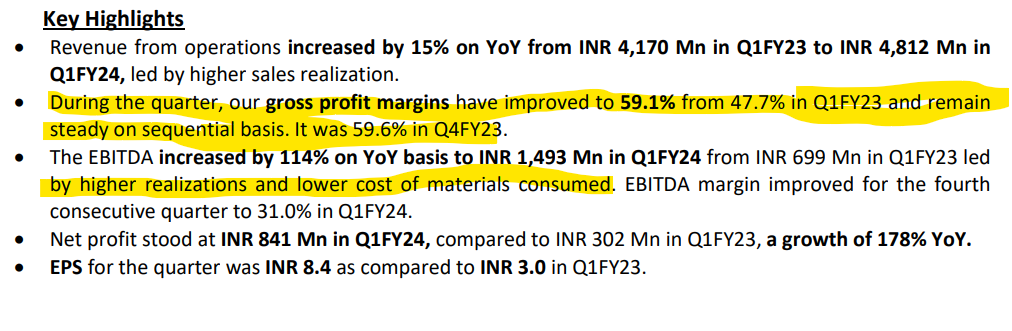

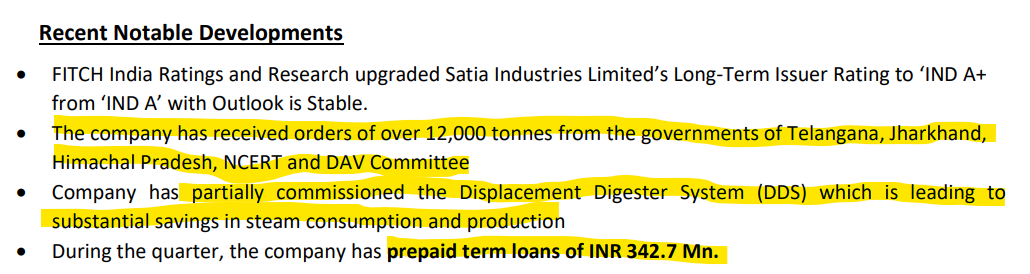

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (13-08-2023)

Super Improvement in Operational Efficiency. The key question in my mind is – if they will be able to maintain such operational performance in terms of gross margins – @Rafi_Syed or @kalpesh4430 can share view.

MTAR Technologies – A wager on innovation meeting economies of scale (13-08-2023)

Hello everyone,

There is seasonality in business in first quarters. What could be the reason of that?

@ankit_george

Disc: i have a tracking position.

Avalon Technologies – EMS Play with US heavy and Proxy to Clean Energy (13-08-2023)

Avalon Technologies Concall notes – August 2023

![]() Leading EMS, started 1997, 12 manufacturing units in India and US and two units in Chennai

Leading EMS, started 1997, 12 manufacturing units in India and US and two units in Chennai

![]() Offers services to Clean Energy, Industrials, Railways, Aerospace, EVs, Medical and Security Infrastructure

Offers services to Clean Energy, Industrials, Railways, Aerospace, EVs, Medical and Security Infrastructure

![]() Management acknowledges that Q1 results are comparatively subdued. However, in line with past trends, second half should do better than first half

Management acknowledges that Q1 results are comparatively subdued. However, in line with past trends, second half should do better than first half

![]() Growth in Indian Market is good but US market is going thru near term challenges.

Growth in Indian Market is good but US market is going thru near term challenges.

![]() In Q1, 45% business is from India and 55% is from US. India segment grew 50% increase YoY in revenues. Over all, for India, growth could be 35% in FY24.

In Q1, 45% business is from India and 55% is from US. India segment grew 50% increase YoY in revenues. Over all, for India, growth could be 35% in FY24.

![]() Haven’t lost a single customer in US during this slowdown

Haven’t lost a single customer in US during this slowdown

![]() 73% manufacturing done in India. Goal is to get to 80-20

73% manufacturing done in India. Goal is to get to 80-20

![]() US customers are rebalancing inventories. There is no clear visibility into how long this might take.

US customers are rebalancing inventories. There is no clear visibility into how long this might take.

![]() US market – Top line has come down, fixed cost remains same plus employee cost went up in US and hence, took a big hit on the margins and that hurt overall margins

US market – Top line has come down, fixed cost remains same plus employee cost went up in US and hence, took a big hit on the margins and that hurt overall margins

![]() Management hasn’t seen slowdown in US like this before

Management hasn’t seen slowdown in US like this before

![]() Had given a guidance of 25%-30% growth rate for FY24 earlier but now, we believe it will be 15-25% range

Had given a guidance of 25%-30% growth rate for FY24 earlier but now, we believe it will be 15-25% range

![]() To improve the profitability, management is doing two things: 1) Optimizing production allocations – Strategic relocation of some of the production activities from US plant to India plants and 2) Rationalizing costs in US operations

To improve the profitability, management is doing two things: 1) Optimizing production allocations – Strategic relocation of some of the production activities from US plant to India plants and 2) Rationalizing costs in US operations

![]() Added 3 Clean Energy customers (2 in US and 1 in India) with one of them being in EV space. Revenues from these customers may show up in H2FY24 to FY25 and some of our previous wins will translate into revenues in next 2-3 quarters.

Added 3 Clean Energy customers (2 in US and 1 in India) with one of them being in EV space. Revenues from these customers may show up in H2FY24 to FY25 and some of our previous wins will translate into revenues in next 2-3 quarters.

![]() Entered a new segment in Aerospace. Received first order in Plastic parts used in interiors of commercial aircrafts. Also entering into heat shields

Entered a new segment in Aerospace. Received first order in Plastic parts used in interiors of commercial aircrafts. Also entering into heat shields

![]() Adding seasoned senior management professionals across operations and business development

Adding seasoned senior management professionals across operations and business development

![]() Repaid about 200cr outstanding debt (from IPO and internal accruals). US subsidiary has about 100cr debt left as of Q1FY24. India entity is almost debt free now.

Repaid about 200cr outstanding debt (from IPO and internal accruals). US subsidiary has about 100cr debt left as of Q1FY24. India entity is almost debt free now.

![]() Working Capital cycle may fluctuate but planning to decrease it by 10-15 days by end of FY24 compared to FY23 (it was 117 end of FY23)

Working Capital cycle may fluctuate but planning to decrease it by 10-15 days by end of FY24 compared to FY23 (it was 117 end of FY23)

![]() Expecting to grow more in Railways Braking and Interlocking. No specific timelines or visibility is there as it depends on when Govt will release. But the customers are saying “Get Ready”.

Expecting to grow more in Railways Braking and Interlocking. No specific timelines or visibility is there as it depends on when Govt will release. But the customers are saying “Get Ready”.

![]() In the Communication and Networking devices(where PLIs are coming into picture), Avalon is working with two large entities/govt bodies but very early conversations.

In the Communication and Networking devices(where PLIs are coming into picture), Avalon is working with two large entities/govt bodies but very early conversations.

![]() On the win in Aerospace (Heat shields, Plastics components) for commercial aircraft – Working on it for couple of years. Big win and it’s a start. Ramp up make take 8-12 months. It might be $3-5 million per part per year of kind of opportunity. Avalon has done smoke detectors before and doing plastic components for the first time

On the win in Aerospace (Heat shields, Plastics components) for commercial aircraft – Working on it for couple of years. Big win and it’s a start. Ramp up make take 8-12 months. It might be $3-5 million per part per year of kind of opportunity. Avalon has done smoke detectors before and doing plastic components for the first time

Avalon Technologies: My interpretation of Q1FY24 concall

-

US Market slow down is real and no clear signs of how long the slow demand may last. Expect a weak Q2 as well

-

Avalon is adding more seasoned mgmt in business development space. While this is a good things for future years, it also means, employee cost will go up. Mgmt had already mentioned that, US employee played spoil sport in Q1 margins. So, I don’t expect any better for Q2 also.

-

They had given a guidance of 25-30% just couple of months and now revised it to 15-25% (the tone sounded more on lower side). To me, it looks like the scenario is changing quite fast. So, I would operate with the assumption that FY24 might be more like 15% growth and more of it coming from India.

-

But the fact that they haven’t lost any customer and actually won a few including one in EV and new orders in Aerospace builds confidence on the future. Plus, they are one of the large players when it comes to Railways.

Disc: I am personally holding it and will look forward to nibbling slowly as the stock price consolidates.

Control Print – Deserves attention? (13-08-2023)

Buyback tax is paid by co (~23% including CESS) and is tax free in hands of shareholders. Dividends are taxed at normal tax rate for investors. Most large investors (including promoters) end up paying 40%+ on dividends, thats why a lot of companies now opt for buybacks as it has become a more tax efficient way of returning cash.

Investors’ contribution in building the business has been an absolute zero. Promoters are entitled to bearing the fruit of their own work, and please keep in mind promoters are the largest shareholders. Indian laws are anyway very favorable for minority shareholders, we should try to keep our expecations at an appropriate level.