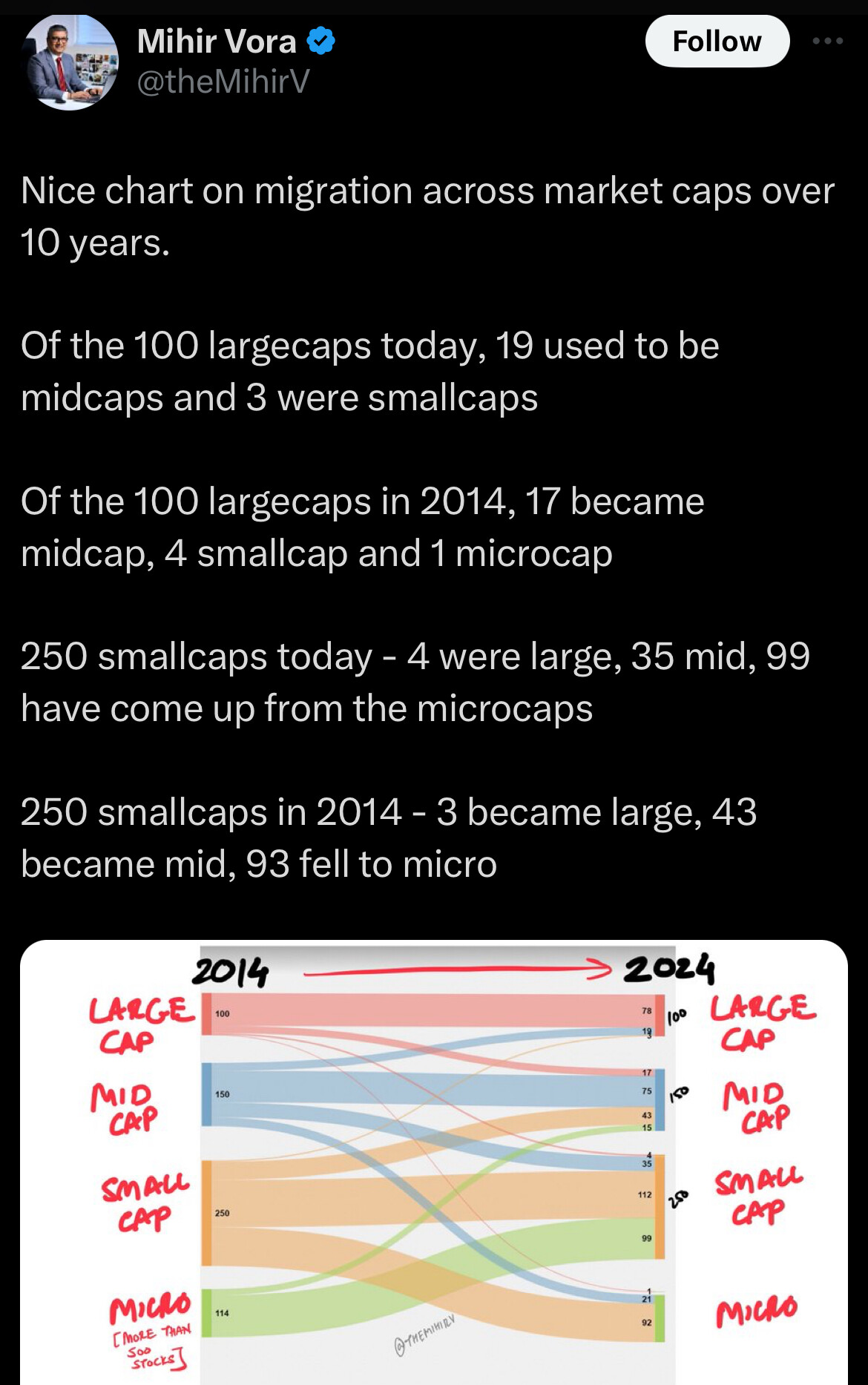

This chart is very interesting. it shows the risks of investing in small caps.

Out of 250 small caps in 2014, 3 became large, 43 became mid, and 93 fell to micro

This chart is very interesting. it shows the risks of investing in small caps.

Out of 250 small caps in 2014, 3 became large, 43 became mid, and 93 fell to micro

History of BLS

Not exited, reduced position size to fund other opportunities.

I am thinking as a mean reversion bet. Other yarn/spinning cos have reported decent nos in recent quarters because of lower raw material prices and better finished material prices. While share prices of other yarn cos picked up, same was not the case with Ambika. Plus, Ambika’s dividend yield is quite decent. In their recent AGM, they mentioned about outsourcing most yarn manufacturing and improving their free cashflows. I feel its a lower risk bet.

AGI Infra

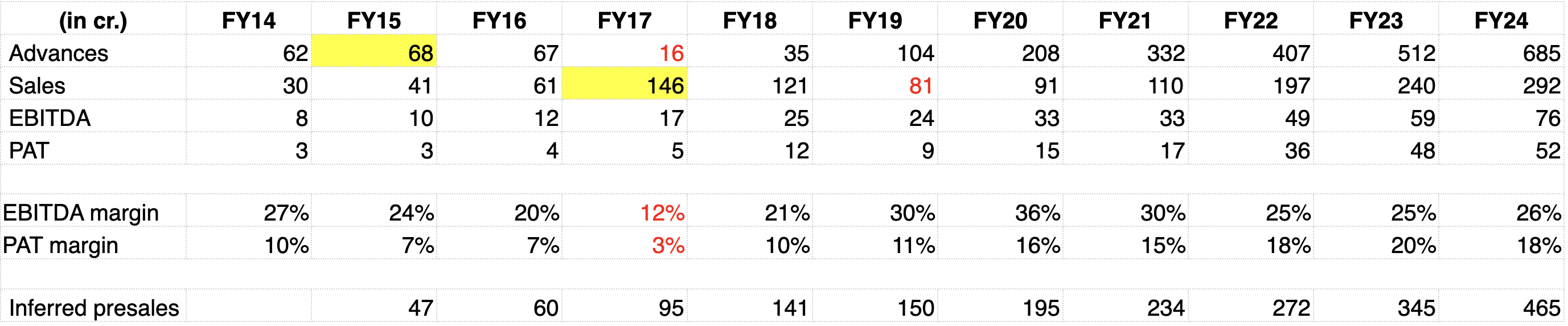

I have recently been working on AGI Infra and have been very impressed with their growth, while maintaining high margins and low debt (see their growth charts below). Its not very common for real estate companies to fund their growth via internal accruals. I am sharing some of my work on AGI as we dont have a dedicated VP thread.

History: Incorporated in 2005 as G. I. Builders Private Limited, jointly promoted by Mr. Sukhdev Singh Khinda and Mrs. Salwinderjit Kaur, providing “premium housing at fair prices”. The name was changed to AGI Infra Limited in 2011

AR24 notes

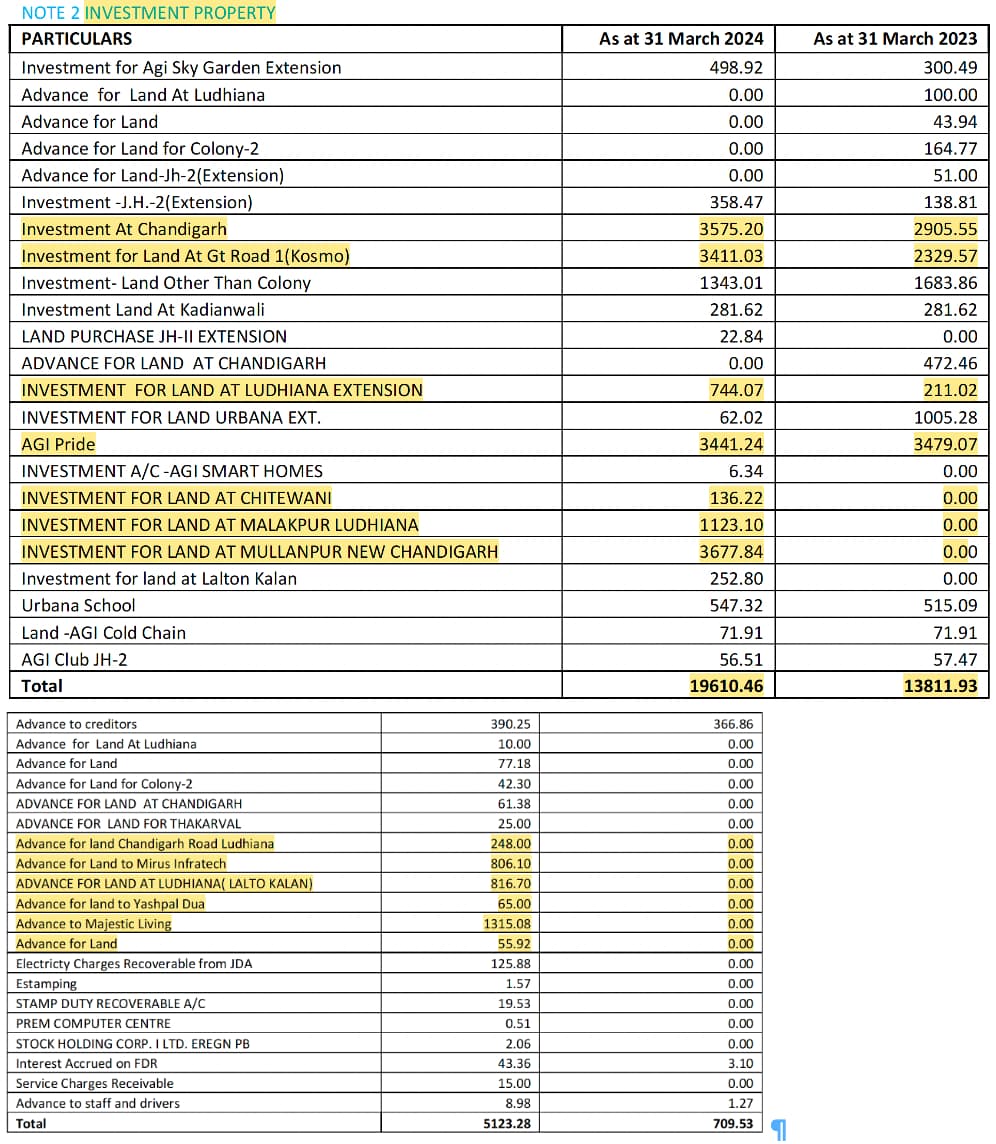

Financials

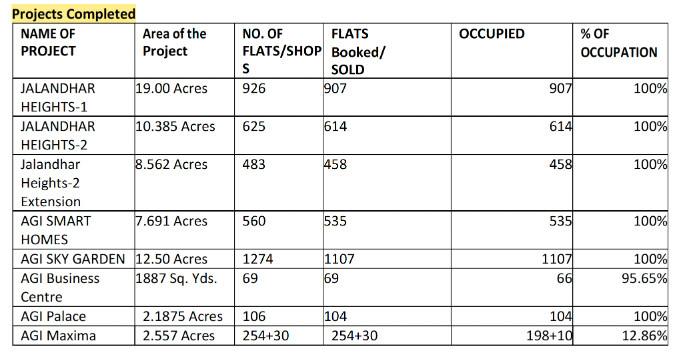

Completed projects (4,327 units, unsold: 249 units)

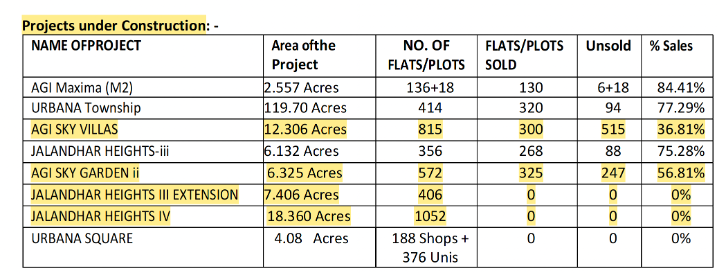

Under construction projects (4,333 units, unsold: 968, unlaunched: 2,022)

Miscellaneous

AGM notes

Miscellaneous

Upcoming: 7 projects

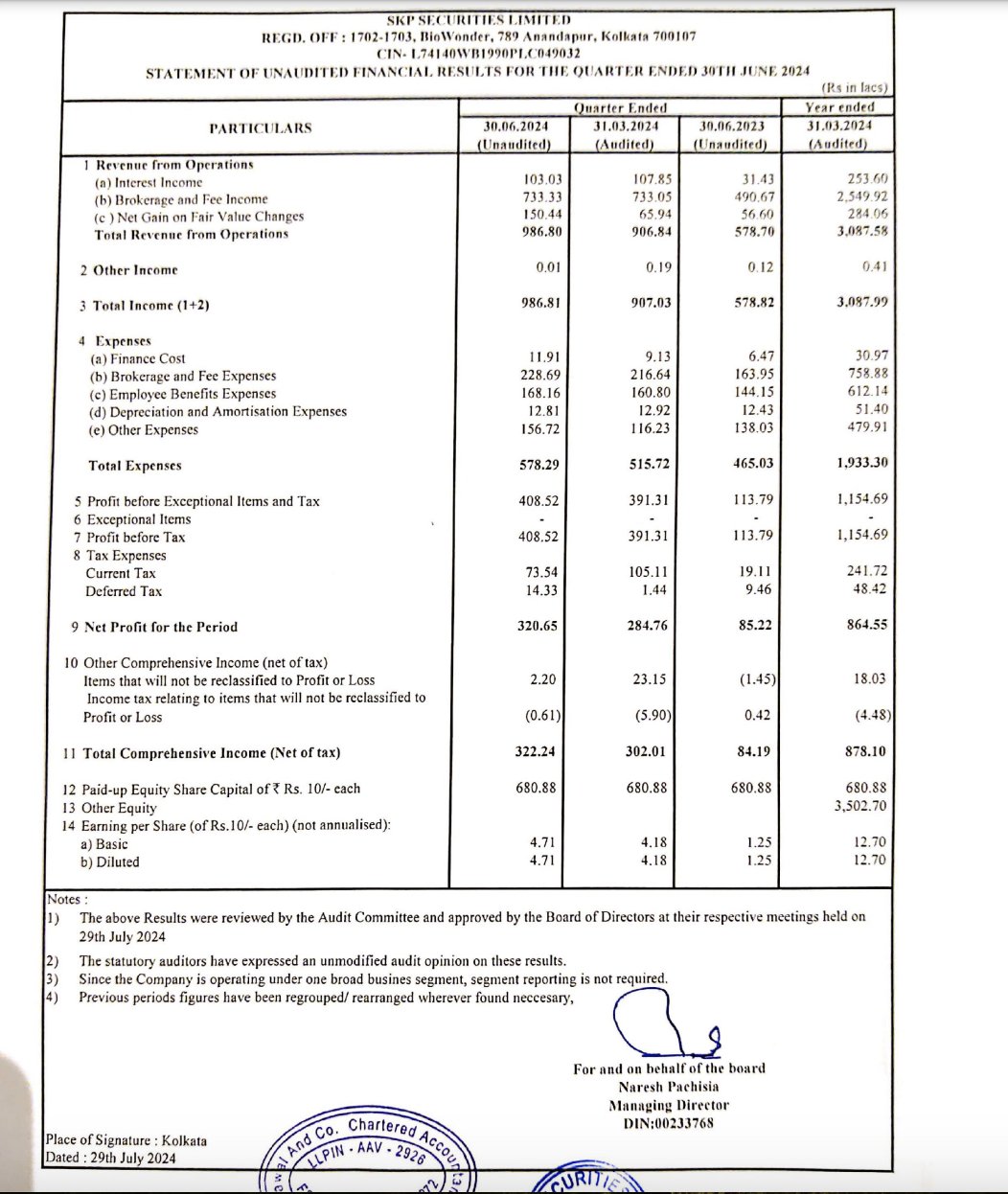

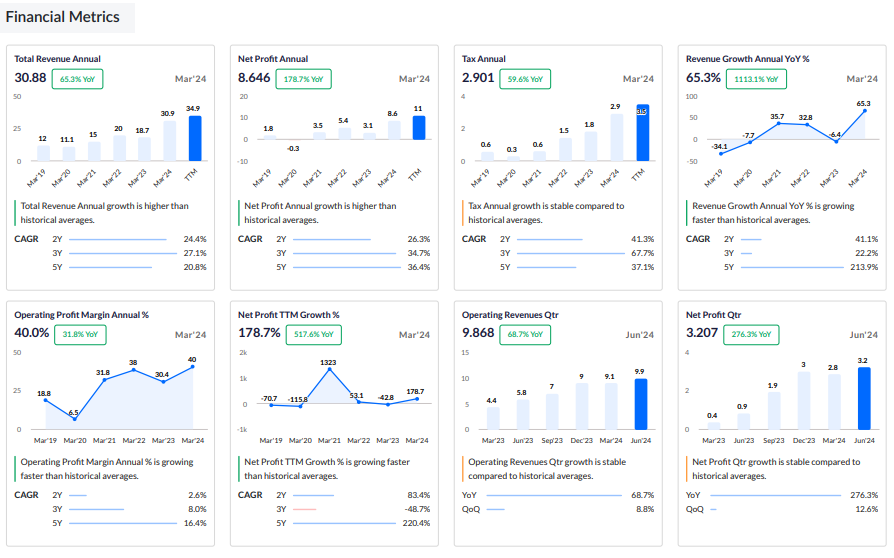

Latest Results:

Sales up by 69% YoY to 9.87 CR

Profit up by 278% YoY to 3.2 CR

Earnings per share increased by 277% to 4.71 rupees.

Amazing growth story in last 3 years.

It has Intrinsic Value of 328 Rs., while trading at 175. Is it really undervalued?

Company Info: SKP Securities is primarily involved in financial services, including stock broking, investment advisory, and asset management. The firm caters to retail and institutional investors, offering services such as:

The company aims to provide a range of financial solutions tailored to the needs of its clients, helping them navigate the complexities of the financial markets.

Mcap – 119 Cr

P/E – 10.8

Promoter holding – 75%

ROE – 22.9%, ROCE – 30%, ROIC – 26%

ICR – 40

Sales growth (3 Years) – 27%

Debt to equity – 0

OPM – 44%

Market Cap/Sales – 3.5