I’m pleased that it could be beneficial. If you’re interested in further insights and techniques, you might want to think about joining my Quora space at: https://artificialintelligenceasymmetricbetbyhumans.quora.com/?invite_code=nM83dPHbUJpm2MecUsaG.

Posts in category Value Pickr

TARSONS products ltd (11-08-2023)

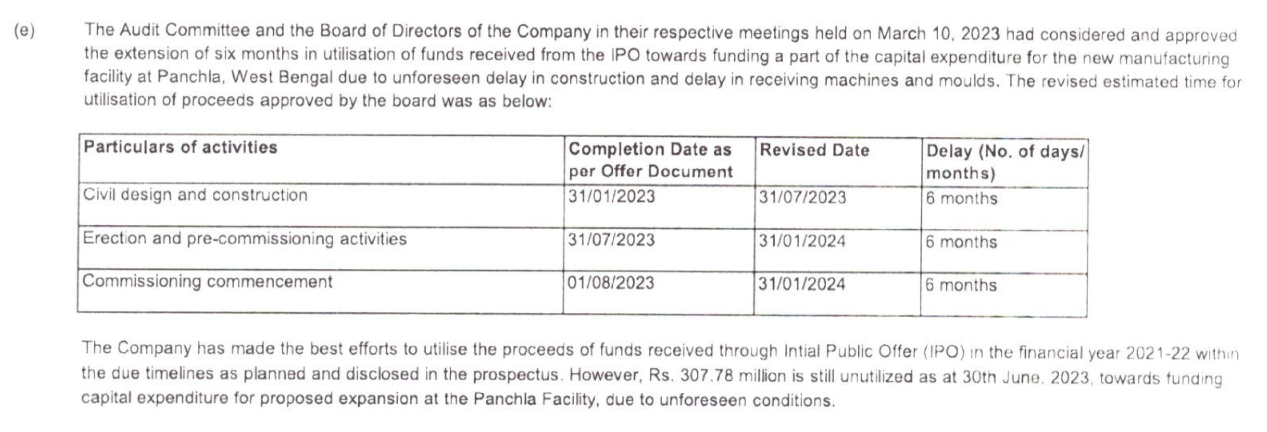

The company has ran into problems in construction and commissioning of the Panchala plant. Everything has been delayed by 6 months and the commissioning of the plant will be done at the beginning of Q4FY24, per the released details. Would have appreciated if they had elaborated the ‘unforseen’ circumstances due to which the construction and commissioning has been delayed.

Per technical analysis, the stock is in stage 4 decline. My perception is that it will take a long time to come back in stage 2 growth period, which, prima facie should come on the backs of increased topline and better margins from Panchla plant.

Hitesh portfolio (11-08-2023)

sir please share your view on MAHANAGAR GAS (MGL)

Mirza International – consistent performer but undervalues at present? (11-08-2023)

Many congratulations to all who waited & stayed put! I’m sure the Redtape listing must have warmed the hearts of all its shareholders! The fact that it closed on upper circuit after accumulation all day close to the lower circuit probably means that there is still some unmet demand.

My gut feel is that this one may have the legs for a long race, so guys it might be a good idea to not be in a hurry to rush out of the door!

Kovai Medical Center and Hospital – Health and Wealth (11-08-2023)

Q1 FY 24 results are out.

Revenue:

- 274 crores (Q4 FY 23 – 267 crores and Q1 FY 23 – 236 crores)

out of which:

- Health care revenue – ~256 crores

- Medical College revenue – ~18 crores

Net Profit:

- 31 crores (Q4 FY 23 – 30.5 crores, Q1 FY 23 – 24 crores)

Not much reduction in either interest costs(~10 crores) (or) depriciation( ~22 crores) compared to Q4/Q1 FY 23

StageInvesting +Elliot Waves (11-08-2023)

Dear @StageInvesting ,

Could you please give your view on Balrampur Chinni, It had a good Q1.

Thanks for all your help in this forum.

Tracking the AI Disruption: Impact and Benefits for Businesses (11-08-2023)

Awesome, Malay! Thank you so much! I will try playing with this. Please keep sharing such wonderful ideas.

TARSONS products ltd (11-08-2023)

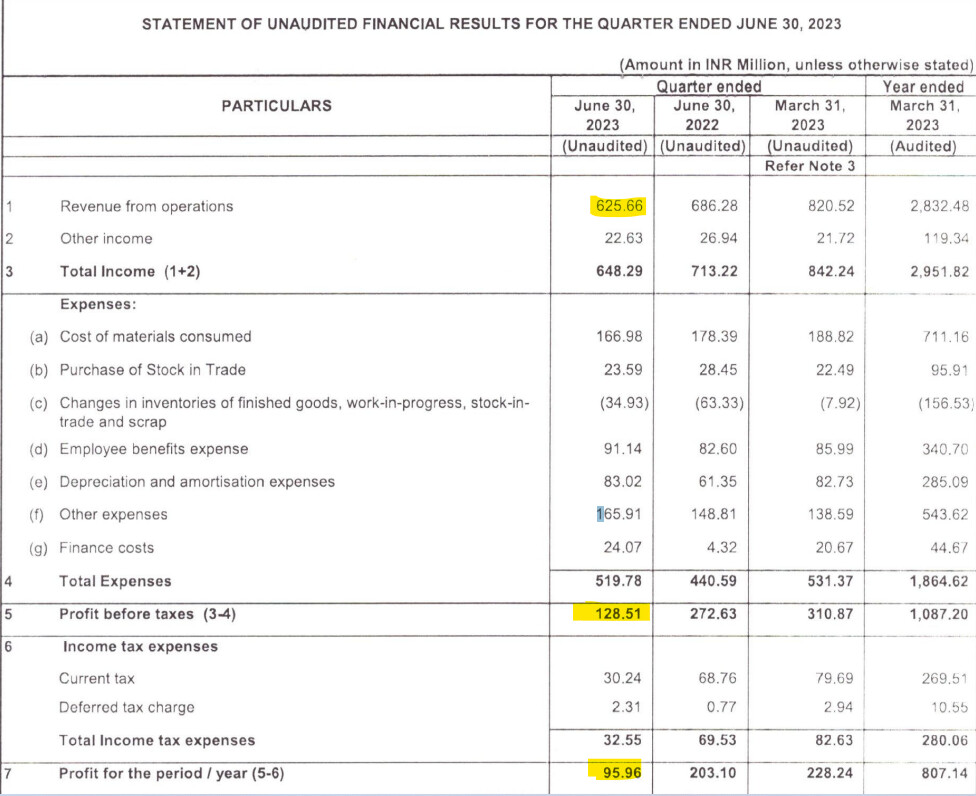

CO has been utterly disappointed with the results, as the industry, which is on an upward trajectory, had slight expectations that CO would give some better results. but this has not happened, and with an almost 1000 bps decline in margin, we would definitely see the pressure from the market. I doubt the industry is shaping up and not allowing companies to improve margins. I only hope that the launch of the Panchala facility is a trigger, and I’m not sure how this is materializing now.

Jagran prakashan (11-08-2023)

It has been around 3 years of holding Jagran Prakashan for me. Jagran has been one of the most interesting and controversial (among my investor friends) picks for me. I thought of sharing my experience and learnings of making a contra investment. I first bought the stock at ~37 and kept buying till ~66-67.

Jagran was a case of classic value investing. This was as contrarian as it gets. There was (and still is) extreme pessimism around the stock. Everyone told me this was a sunset industry, this kind of value buying doesn’t work anymore, no FII/DIIs would ever touch this stock, who reads newspapers anymore and in this era of technology why do you want to touch an old school stock?

I always list down 3 reasons before I buy a stock. These were my reasons for Jagran –

Strong balance sheet strength and cash flows

Jagran had 600 cr of cash & investments on a Market cap of 800 cr. The company had also generated ~300 crores of free cash flow every year. There was no long-term debt and Dainik Jagran was the #1 newspaper in India, with a strong foothold in the Hindi heartlands. In fact, within the 600 crores is freehold land whose fair value is much higher than stated in the balance sheet.

Consistent history of promoters sharing wealth with minority shareholders

Whenever you are buying a company based on balance sheet strength or cash & investments, it is important that the promoters have a history of sharing wealth with shareholders. The promoters of Jagran have been excellent in this regard. Instead of making any unrelated acquisition, they have been buying back stock and paying regular dividends. When I bought the stock, the dividends and the buyback amount for the last three years was greater than the market cap of the stock at that point.

The predications about the death of print were a tad bit exaggerated

What happened in the west does not necessarily replicate back here in India. The growth of print had stagnated, and I was under no assumptions that this would be a 10x or a multibagger stock, but it was also clear that newspapers weren’t dying, at least not anytime soon. The company was still generating healthy revenues and cash flows. My scuttlebutt also showed that Dainik Jagran had a strong brand recall in its target market and was still favoured by the reader. An acquaintance also owns a small local newspaper in UP and she confirmed that newspaper readership was not declining the way people thought. The cost of a newspaper in India is incredibly cheap and hence people continue to buy it just out of habit.

This is where owner’s mindset is particularly important. If I were offered to acquire Jagran at 800 cr, a company that has cash & investments worth 600 crore and makes around 300 cr of free cash flow every year, would I buy it? Absolutely. It does not matter whether FIIs buy it or what the charts say. The market is a weighing machine in the long run, and it will weigh it correctly, sooner or later.

It has almost been a 3x since my first buy and I continue to hold it. Even today, excluding the cash and investments, the stock is available at roughly 4-5x free cash flow, with digital being an added optionality. The outlook for print is quite bullish for the next couple of years. DB Corp has posted excellent numbers and I expect Jagran’s numbers to be somewhat similar.

This was an important lesson that whenever extreme pessimism is priced in, the probability of market being wrong doesn’t need to be very high to generate a favourable return.

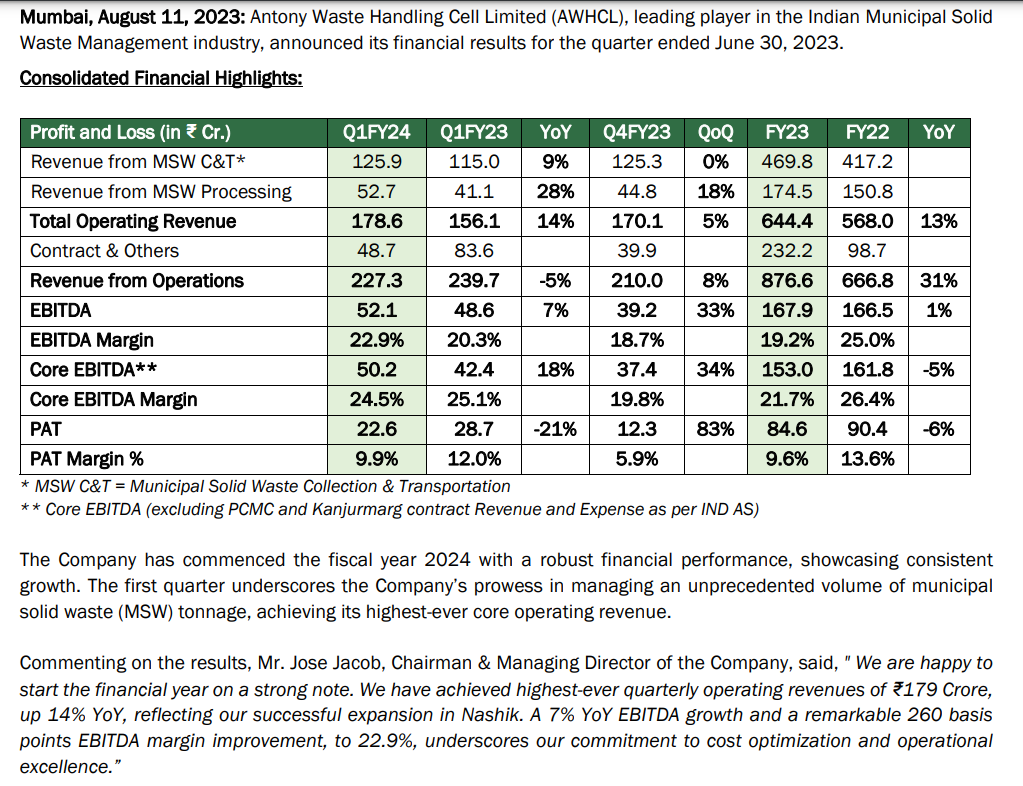

Antony Waste – Long Term (11-08-2023)

Results are good in comparison to the previous quarter, but Q1 is a slightly low volume quarter for the CO. Last year, it was good for the CO, as the escalations helped boost revenues. This time, without this escalation, the results are decent. For most of the other COs listed, Q2 is seasonally weak, but for Antony, Q2 is strong as increasing rainfall adds weight to solid waste overall, thus increasing tonnage costs.