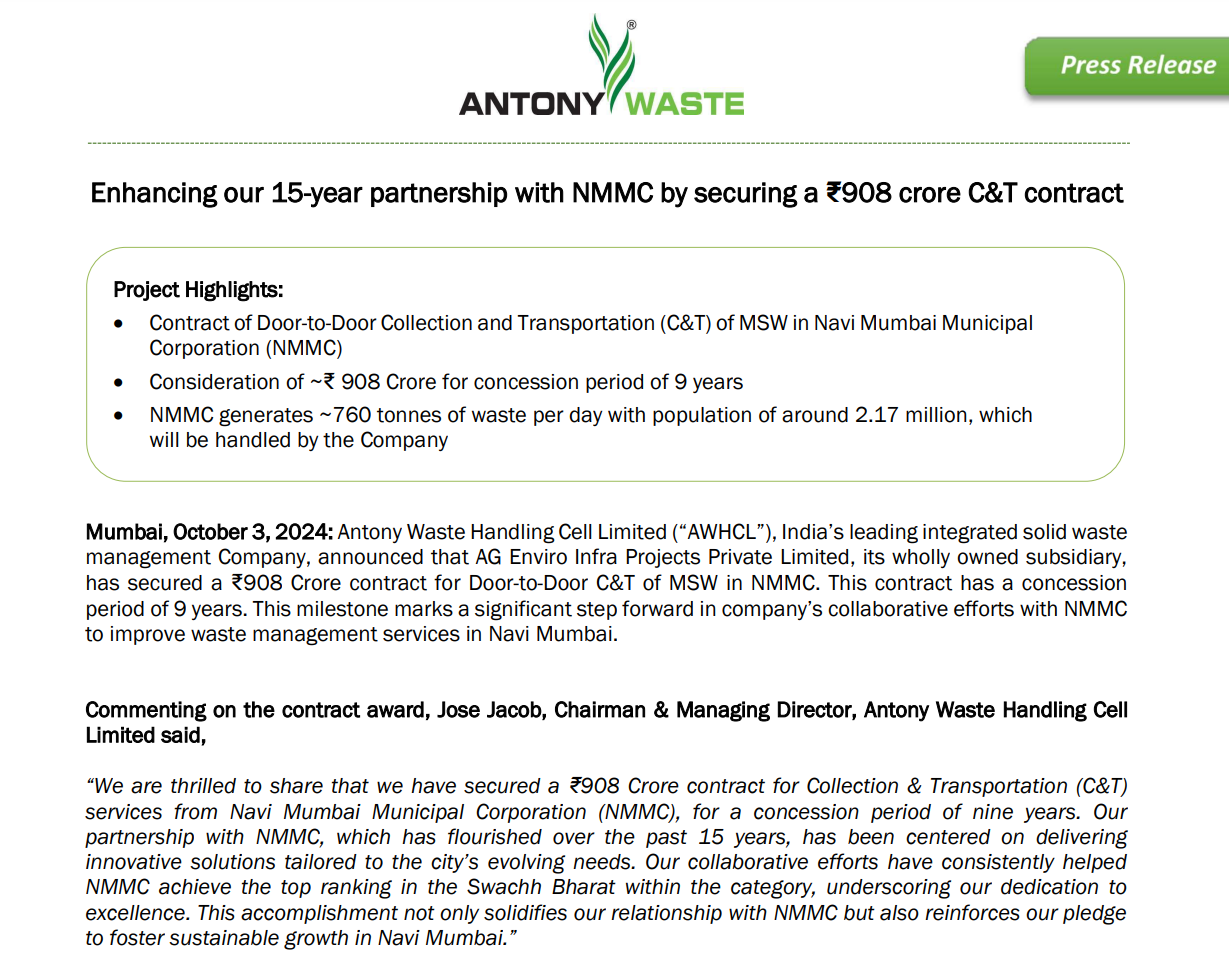

AG Enviro Infra Projects Private Limited, a wholly owned subsidiary of AWHCL wins Collection & Transportation project in Navi Mumbai for a period of 9 years. Total estimated contract value is 908 crores over period of 9 years.

AG Enviro Infra Projects Private Limited, a wholly owned subsidiary of AWHCL wins Collection & Transportation project in Navi Mumbai for a period of 9 years. Total estimated contract value is 908 crores over period of 9 years.

Right now i have many stocks in my portfolio. The problem is portfolio allocation/ construction. So, Yes mutual funds is an option but i prefer direct equity. Because honestly I dont believe any active fund managers. I’d rather go down direct Nifty 50 or Nifty next 50 funds.

I’ll try focusing more on how to get this into a good shape in terms of trimming down and narrowing the focus

ROCE is not the right metric to compare the different firms in this industry.

Anand Rathi is in pure-play mutual fund distribution & advisory while others (Nuvama, 360 One) also provide loan against securities & margin funding amongst other services (such as selling their own MF & AIF products). Hence, they will always have debt on their balance sheet i.e. they act like a bank & capture a net interest spread on the loans they provide.

A more useful metric would be to look at is ROE instead of ROCE.

In theory all 3 taxes – Dividend tax, STCG, LTCG are applicable for those who had DVR shares and opted for it to be converted.

However, the calculations involved are little complex, depending on your purchase date, qty, Deemed Dividend concept, TDS deduction by Tata Motors on the Deemed Dividend amount, potential offset of some LTCG against the same, deduction of STCG etc. I would suggest you download the sample tax calculator that they had issued before the conversion. Plug-in your numbers and change the value of Deemed Dividend as per the latest value they published after conversion…you will get all the answers.

If you are still confused, just contact your CA.

Sharing AGM notes

General

Electronics chemical: discussing with potential customers (NDA) in Europe. In few projects, they are in last phase of R&D and expect commercialization in 2-3 years

Since 2004, their focus was on API intermediates in the pharma sector. Since last 5-years, they have started catering to fine and specialty chemicals and focusing on respective chemistries. Multipurpose blocks help them manufacture molecules in any given chemistry. Expect product mix to change towards fine and specialty chemicals from pharma side. Make similar margins in specialty chemical and pharma

– In our current business, what is the mix of regulated vs unregulated markets that our end products are sold into?

Not into APIs, only present in unregulated markets and generic products. They cater to innovators and have large market shares in 2-3 products

– With the recent commercialization of our GMP plant, what kind of opportunities are we seeing? Are we going more into regulated market supply? What does our product pipeline look like?

Advanced intermediates for European customers – only few products using 1 GMP block. Running GMP block is expensive, and they only do it if the product can justify

– Can you briefly update us about the 3 CRAMS projects we had announced in FY23. How are these scaling up and what kind of revenues can we see in next 2-3 years from these products?

1st project – Q4 contribution (fine chemicals).

Cosmetic – project has been dropped

Agrochemicals – submitted small quantities from pilot plant (to be commercialized in 18-20 months)

– Have we won new CRAMS contracts? Can you provide us an update of latest business developments?

Getting more enquiries – haven’t seen any agreements yet

– What kind of product realizations do we expect in next few years? We were mentioning about new products of $500-1000/kg realizations, are we on track to launch more of these?

800 tons – earlier products were 500-1500/kg. New products are 3000-4000/kg

– What is our current reactor capacity and what utilization are we operating at? When do we go for next phase of expansion or is peak capex behind us?

After Plant 8 capacity has increased to 350 kl (from 230 kl) – prior utilization: 80-85% (full realization). Plant 8 utilization will require 18-24 months

Plant 7 is being designed – 20-24 months

Can do 2 more plants (Plants 9 and 10)

– Given that we have significant land in Dahej, any plans on a greenfield capex?

Bulk projects – customer dedicated. In discussion with 2 customers, agreements still to be signed

– How much sales comes from our top 3 and top 5 products? What are those products and what is their end usage?

5 products – 60-62% of sales (reduced from 80% earlier)

Disclosure: Invested (no transactions in last-30 days)

Acquired Goyal distelleries, promoters selling stake, now SEBI notice, not sure what to make of the recent developments

This has prompted me to stick to smallcap and microcap universe.