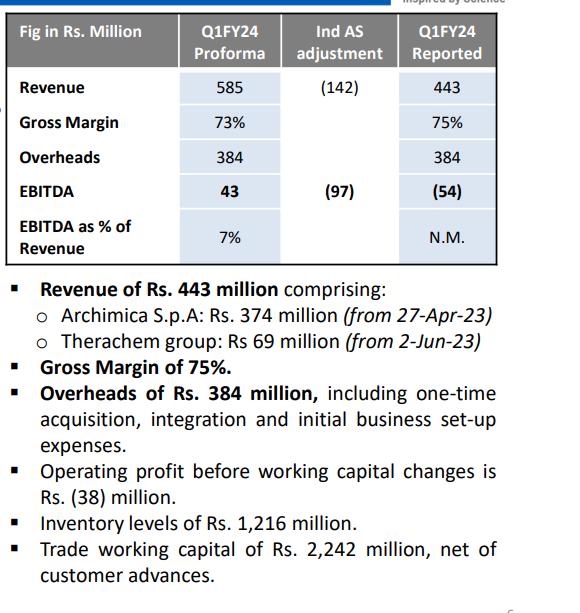

Ball has started rolling

73% GM and this business will add 200 crs at the top line…and EBIT accretive…

PI may attain 8000cr topline this FY…and also the presentation, data is full of disclosures… 60% improvement in cash flow !!

Ball has started rolling

73% GM and this business will add 200 crs at the top line…and EBIT accretive…

PI may attain 8000cr topline this FY…and also the presentation, data is full of disclosures… 60% improvement in cash flow !!

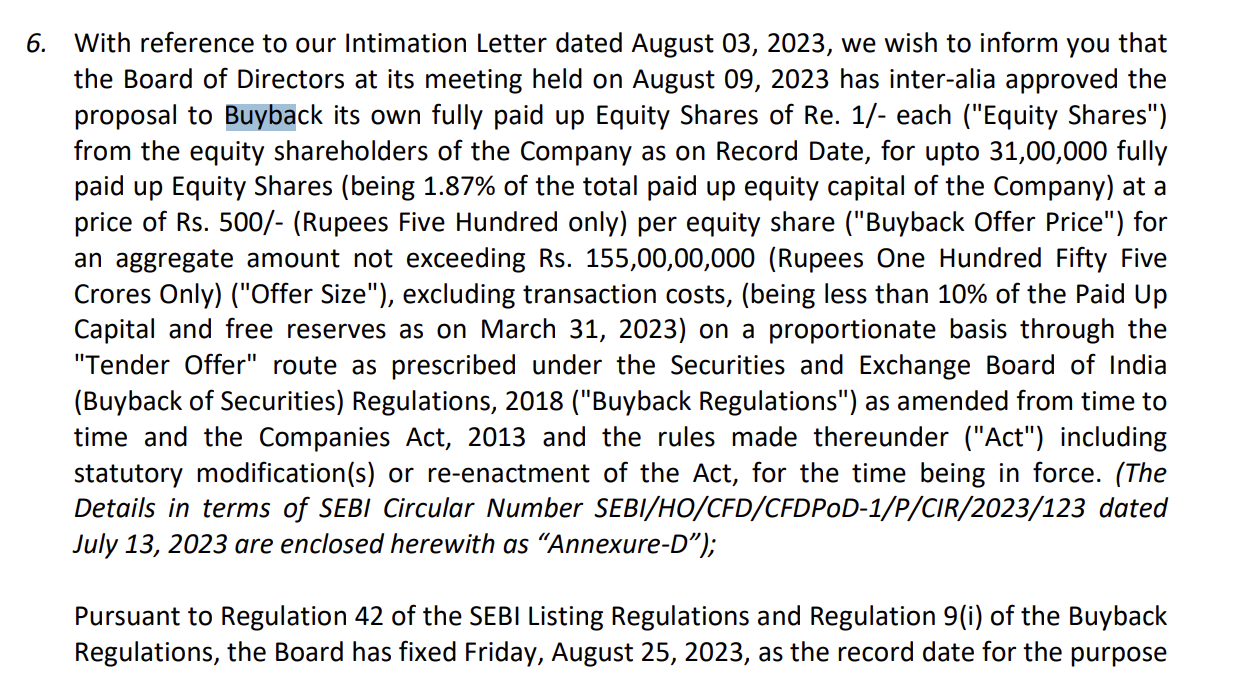

Buyback Announcement: @Rs 500 worth 150 Cr (CMP: ~390ish / MCap: ~6500)

Link: https://www.bseindia.com/xml-data/corpfiling/AttachLive/ae13aebc-63a1-45c9-a652-fa2403c70cf5.pdf

Disc: Invested (Portfolio sizing HERE)

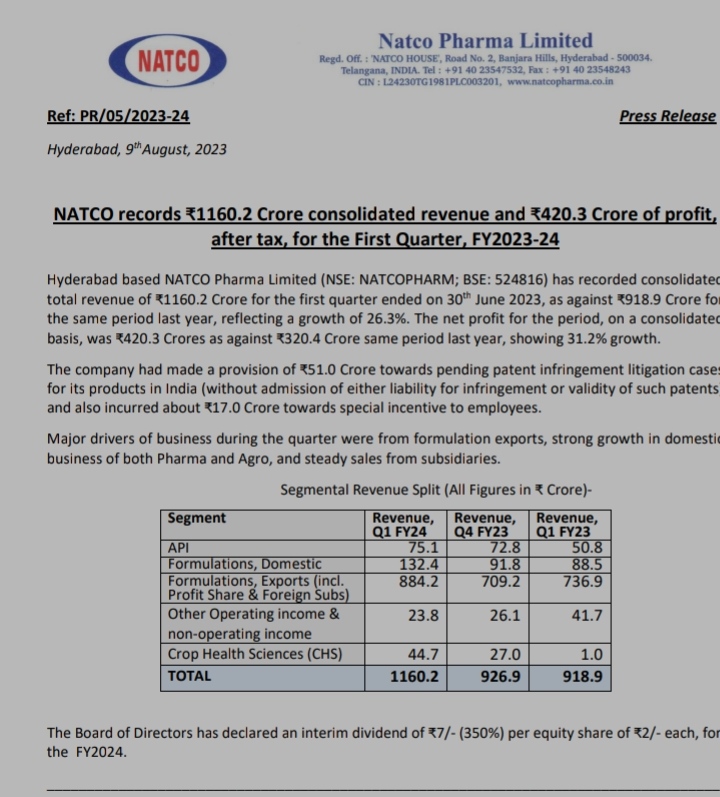

Natco pharma results

Disc: invested

Good set of quarterly numbers by Force Motors.

All time high EBIDTA margins.

Presentation and announcement

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2f482e3e-f6d3-4bf2-ad8d-6f33302eff0c.pdf

Great results.

From investor concall…loss of revenue estimate of Rs.150 Cr and failure to supply penalties of Rs.21 Cr …these are kind of one off …

R&D Exp of Rs.43 Cr in Q1FY24…expected to go upwards of Rs.50 Cr in subsequent quarters of FY24

Gradual improvement expected in Margin from Q2 onwards but management declined to confirm any guidance around revenue & margin for rest of FY24…

They also discontinued giving molecule wise sales break-up because of competition

From investor concall…loss of revenue estimate of Rs.150 Cr and failure to supply penalties of Rs.21 Cr …these are kind of one off …

R&D Exp of Rs.43 Cr in Q1FY24…expected to go upwards of Rs.50 Cr in subsequent quarters of FY24

Gradual improvement expected in Margin from Q2 onwards but management declined to confirm any guidance around revenue & margin for rest of FY24…

They also discontinued giving molecule wise sales break-up because of competition

From investor concall…loss of revenue estimate of Rs.150 Cr and failure to supply penalties of Rs.21 Cr …these are kind of one off …

R&D Exp of Rs.43 Cr in Q1FY24…expected to go upwards of Rs.50 Cr in subsequent quarters of FY24

Gradual improvement expected in Margin from Q2 onwards but management declined to confirm any guidance around revenue & margin for rest of FY24…

They also discontinued giving molecule wise sales break-up because of competition

Q1FY24 results are out and as expected degrowth in revenue but substantial erosion in margins (due to loss of revenue while expenses incurred). While this could be one off but investor presentation doesn’t talk about what is revenue and profit guidance for rest of period unless I am missing something.