(post deleted by author)

Posts in category Value Pickr

Websol energy system ltd (05-10-2024)

This stock fits a lot of good boxes. Had spotted this earlier on and decided not to invest sadly but have taken a tracking position. My only worry is that the margins for such companies depends on the tariffs imposed by the govt. Borosil renewables also suffered due to this issue. Now the margins look great and a 1 year forward PE makes this stock dirt cheap compared to other players but time will tell if the margins can last.

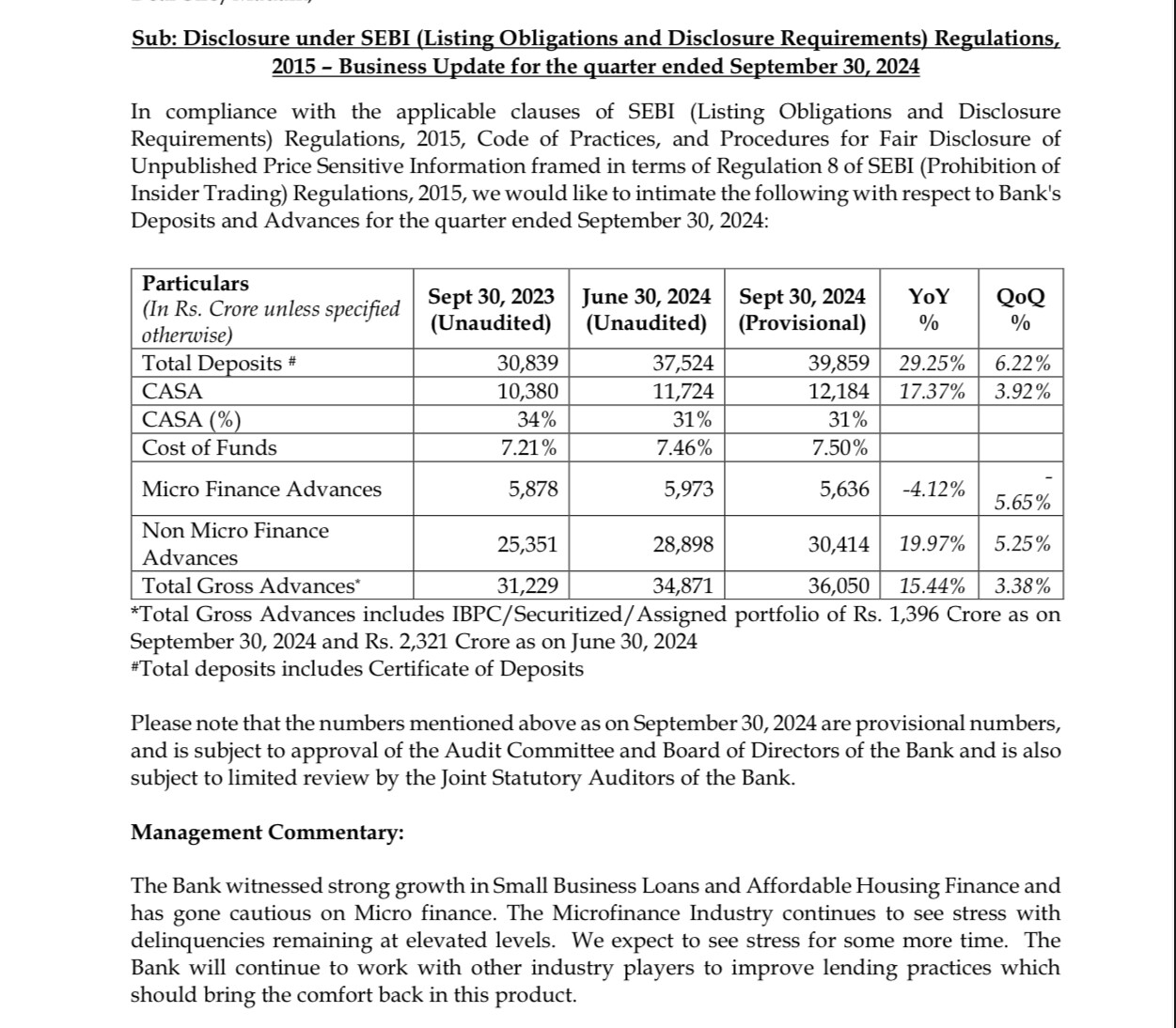

Equitas Small Finance Bank: A Profitable lender to small businesses (05-10-2024)

Key figures for q2 provisional

MANAGEMENT COMENTARY

Strong growth in Affordable Housing & SBL

MFI Industry witnessing stress at the moment & management expecting stress for some more time

MFI is 16 % of total advance & expected to go down further

Deposit growth steady, growth slowing down

Disc- invested

Pitti Engineering Limited: Is it on an inflection point? (05-10-2024)

- Revenue Growth: The combined revenue of Pitti Engineering Ltd is expected to grow significantly post-amalgamation, with projections showing an increase from INR 12,016 million in FY24 to INR 20,356 million in FY25 and further reaching INR 23,768 million by FY27.

- Efficiency Gains: The merger with entities such as Bagadia Chaitra Industries and Dakshin Foundry enables expanded capacity and cost efficiencies. Pitti’s expanded Aurangabad facility, along with new copper winding capabilities, is anticipated to improve margins and customer acquisition.

- Broader Market Reach: The acquisitions extend Pitti’s geographic footprint, unlocking new markets and enhancing its role in high-growth sectors like renewables and railways.

Source: KRChoksey research report

SmallCap Hunter : Trying to find the dark horses with triggers (05-10-2024)

All these stocks have made huge gains for investors who rode on the promise of new and renewable energy. And suppose we keep seeing poor historical performance without seeing the tailwinds and the reasons for the turnaround. In that case, we will end up not investing in future-oriented stocks and be happy with HUL, Tata and Nestle. Just my 2 cents.

Websol energy system ltd (05-10-2024)

The phase 2 execution is pivotal, but big players’ new capacity may not matter for the next 3-5 years as the demand is huge. Big players will not be able to fill the demand-supply gap until 2030 I feel.

Great articles to read on the web (05-10-2024)

Masterclass in Building Materials

Found interesting hence sharing.

My note of above video:

Key Sectors Discussed:

Tiles/Ceramics

Pipes

Wood

Branded vs. Unorganized Players:

Leading companies in these sectors include Kajaria, Somany, Century Ply, Green Ply, Supreme, Astral, and Prince. For example, Kajaria charges a 15% premium over unorganized players, highlighting the power of branding.

Spotlight on the Plastic Pipes Industry:

The plastic pipe industry stands out as the most interesting sector with organized players gaining market share. From 50% in FY10, organized players now control over 65% of the market. Here’s why the big players are getting bigger:

Raw Material Advantage: Large companies source raw materials like PVC directly from manufacturers such as Reliance, while smaller players have to rely on intermediaries.

Proximity to Customers: With transportation costs accounting for 10-12% of pipe prices, being close to customers is a significant advantage. For instance, Supreme has 30 plants across India, ensuring efficient logistics. Other big players like Astral and Prince follow the same strategy.

Builder Preferences: Pipes account for less than 1% of a building project’s total cost, but poor-quality pipes can severely damage a builder’s reputation. Hence, builders prefer branded products for their reliability.

Supreme currently holds a 16% market share and is growing at 25%. The management remains optimistic about future growth, in line with their guidance.

High-Margin Opportunities with uPVC:

Lubrizol and Astral initially partnered to produce uPVC, a high-margin specialty material compared to the low-margin PVC commodity. Although the tie-up ended, Astral now manufactures its own raw materials for uPVC.

Growth Drivers for Plastic Pipes:

Irrigation: A strong growth sector.

Plumbing: Driven by the booming real estate market.

Government Projects: Initiatives like “Nal se Jal” have accelerated growth. Previously, DI pipes dominated these projects, but now uPVC is replacing them.

New Applications: Plastics are finding use in fire safety systems, gas pipelines, door panels, etc., contributing 2-3% of current revenue with potential to grow to 15-20%.

The Wood Industry (Laminates, Plywood, MDF):

This industry is highly competitive, leading to lower margins as companies struggle to operate at full capacity.

In India, plywood dominates with an 80-90% market share, while globally, MDF is preferred. Although MDF was once considered a commodity, over the last decade, many players have shifted focus to it, leading to an overcapacity situation.

Challenges:

The cost of raw wood has doubled in a short time, putting pressure on margins.

Farmers prefer supplying wood for MDF due to its shorter aging process (3-4 years compared to plywood’s 8-10 years), causing a shift in supply dynamics.

Disclaimer: This summary is for educational purposes only. I have investments in Prakash Pipes, not in any of the companies discussed in the video. Some details may not be accurate, so please verify the data.

Microcap momentum portfolio (05-10-2024)

last week (30/09/2024 to 04/10/2024) we got -1.80% (loss) return if we invest equally in 25 shares.

Note : during (30/09/2024 to 04/10/2024) this period MicroCap Index -2.36% loss , Nifty-50 Index -4.45% loss

Shivalik Bimetal Controls Ltd (SBCL) (05-10-2024)

Thank you @Donald @dd1474 on the wonderful notes on Shivalik. I will try to simplify the technical aspects in the upcoming days. However the above quote has grabbed my attention. Forward integration to current sensing PCB modules can be done in 2 ways

-

You take the OEM requirements on the current sensing modules and then bid with your prototypes, once you get approval the product goes to mass production. You effectively become a Tier 1.

-

The other option is that you become a contract manufacturer for a Tier 1 , who based on your capability and pricing is not only buying your shunts , but asking you to fit it inside a PCB module and then send for further assembly. ( This could also be due to complicated and compact shunt design) .

For me point 1 is not too attractive as they would end up competing with their customers like Hella and Conti. Shivalik does not have the technical capability or experience to deal with an OEM directly.

Point 2 is very attractive as they are moving from a shunt design and manufacturer to a shunt system supplier . If they execute this well, one day they might as well have an in house current sensor module. Such position also allows Shivalik to go up the value chain and become more like Issabella Hutte in the current sensing space.

Disc: I have worked in this space in my previous job and hence I am extremely biased.