This is pure spamming and it’s there in every single thread.

@admins please look into this.

Sharing my analysis on GPT Infra and why it stands a chance to 2x in next few quarters

Calculation for GPT to 2x

For FY25,

Revenue – Rs 1300 crore

Profit – Rs 80-82 crore

Shares outstanding – 12.6 crore

EPS – Rs 6.5

PE – 42-45 considering a growth company and previously achieved PE = 42

Price – 45*6.5 = 292 (2X from current levels)

Disc: Invested, biased

Anand Rathi Wealth Management (ARWL) stands out in the wealth management industry. It has a strong competitive moat compared to its listed peers like 360 One WAM and Nuvama Wealth Management.

While others have struggled to surpass the 20% ROCE (Return on Capital Employed) threshold, ARWL has consistently delivered impressive figures.

This consistent outperformance highlights ARWL’s superior operational efficiency and competitive edge in the wealth management space.

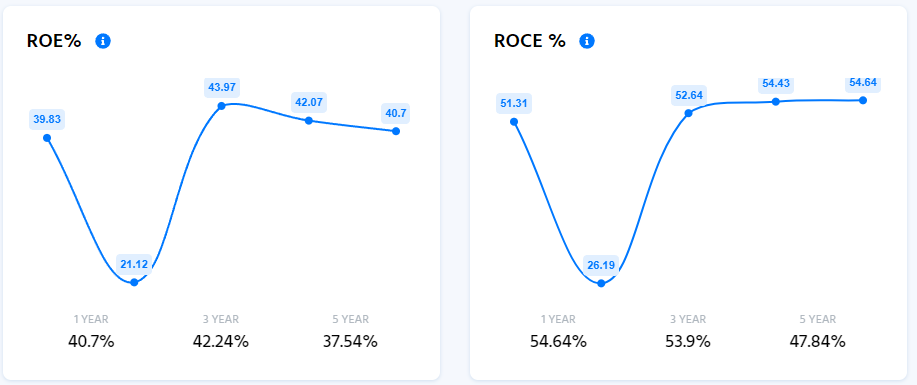

From Q1 FY24 to Q1 FY25, the company’s ROE was around 40% odd levels (the Annualised Return on Equity is 42.8% for Q1 FY25). The company is confident in maintaining current ROE levels, driven by sound capital management and growth strategies.

(Image Source: Finology Ticker)

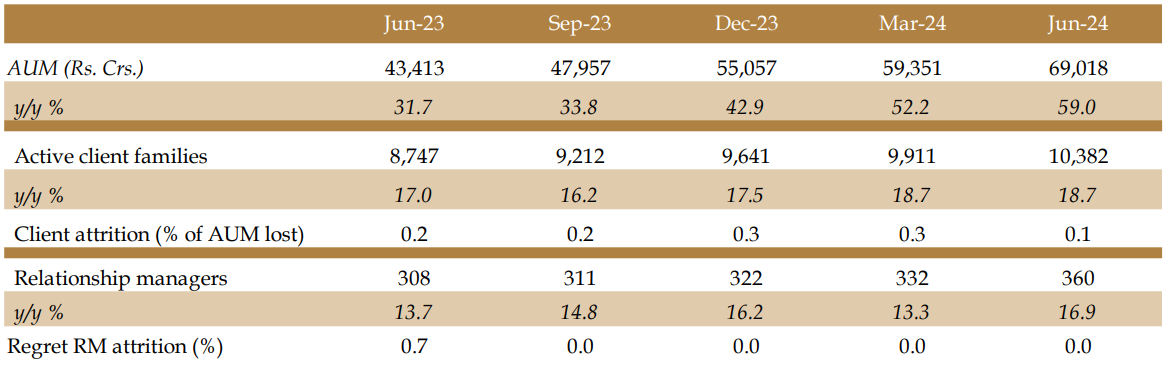

Here is ARWL’s recent highlight:

(Image Source: Company’s Presentation)

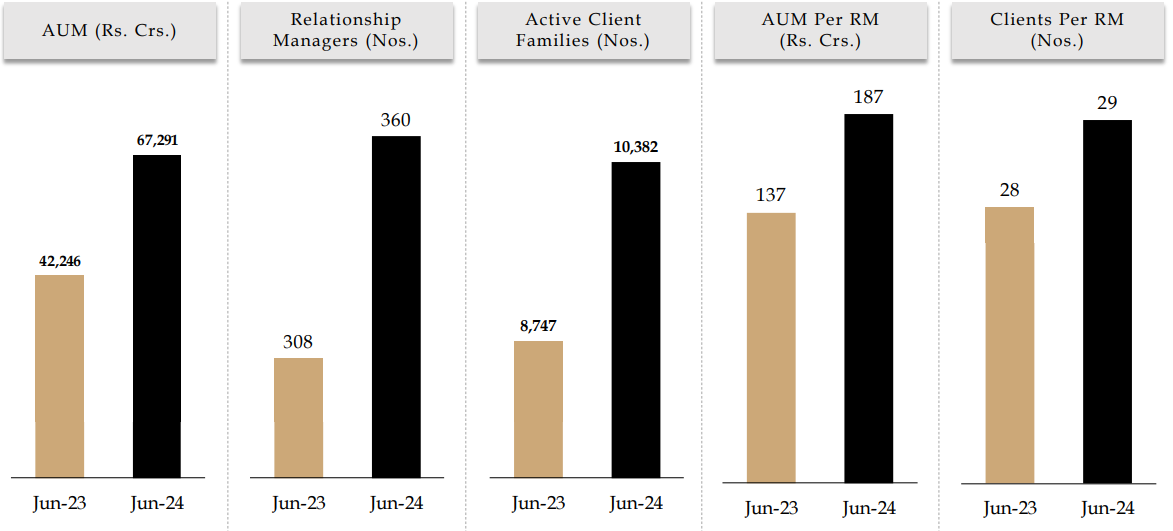

Improvement in key operational metrics and analysis of future growth:

(Image Source: Company’s Presentation)

What do you think about the company’s future?

I agree completely with your analysis. Most of people don’t understand Blinkit’s high growth is due to opening more dark stores and expansion to newer geographies. The most important metric is SSG (Same store growth), which Zomato, Blinkit don’t share. Also, given this sector has potential to affect millions of Kirana stores, Govt will certainly introduce some regulations. So, at this valuation, one should stay out of this.

Huge market sale of shares worth about Rs 160 Cr by promoters (Amar Engg, Angad Estates, BS Sandhu & Associates and Ultra Portfolio Management) which they reported to the exchanges today. This is different from inter-se transfers.

Hope this will remove any overhang on the stock price.

Assuming current dividend growth rate to be toned down to 5% and a cost of capital of 10%, when we do a DDM on the stock, the value stands at approx CMP.

But looking at the past, the dividends have grown from Rs 20 Cr in FY13 to Rs 565 Cr in FY24. Hence the 5% growth in dividends is a toned expectation.

Therefore the stock is significantly undervalued compared to its true value.

As for low operating margins, the business has never reported a PAT loss for the past 10Y, with ROCE above 15%. Hence we can assume the same to continue in the future.

Also it is run by professional management which reduce related party nature of transactions (as per crisil ratings report for the company).

Can accumulate if the dividend yield and earnings yield increases.

Well, there could be a further 12-year extension of duty free access for Bangladesh after it graduates from LDC status

Vikasji, What about valuation of Kaynas, its sitting at roof,

Hello

Route isnt an IT company … it uses technology and provides services more on a responsibility basis and have metrics which add value to customer …

So customers will tend to rely on them and will continue to do business . There is also technology disruption… which is very imprtant … So companies who do not keep up with technology disruption ( which is difficult) will fall by the wayside…

Malolan

Nope, it will not be. You end up paying STCG/LTCG only on the fractional shares that are converted and paid as cash into your dmat account.