Posts in category Value Pickr

InterGlobe Aviation – Indigo (04-10-2024)

Spicejet has had a ton of bad luck, first with the Marans and then with Covid and has still survived. I am fairly confident that under Ajay Singh whenever the airline catches even a small break, it will capitalize on it completely. Indigo is running mostly because its scale has given it an impressive moat but as soon as a viable options comes along, it will face a lot of pressure.

Disclaimer: Invested in both Indigo AND Spicejet. Aviation as a theme for growth is solid in India.

Shivalik Bimetal Controls Ltd (SBCL) (04-10-2024)

I think this is part of their Strategic Shareholding Changes – context above.

Shivalik Bimetal Controls Ltd (SBCL) (04-10-2024)

Promoters are changing from the Sandhu family to the Ghumman family. They have already reported to exchanges as well.

This is not a sign of worry. Is there something else I am missing?

Manappuram Finance (04-10-2024)

Thanks @Bhajan_Watwani for your input, and yes you are right. Muthoot has been increasing Gold Loan AUM consistently as a better growth rate vs Manappuram in FY2022, FY2023, FY2024 i.e. almost double is the growth rate.

| (in Rs. Cr) | Q1FY2025 | FY2024 | FY2023 | FY2022 | FY2021 |

|---|---|---|---|---|---|

| Manappuram Cons. AUM | 44932 | 42069 | 35428 | 30261 | 27224 |

| (% Growth – FY21 as base) | 6.81% | 18.75% | 17.07% | 11.16% | |

| Manappuram Gold AUM | 23647 | 21561 | 19746 | 20168 | 19082 |

| (% Growth – FY21 as base) | 9.67% | 9.19% | -2.09% | 5.69% | |

| Vs | |||||

| (in Rs. Cr) | Q1FY2025 | FY2024 | FY2023 | FY2022 | FY2021 |

| Muthoot Cons. AUM | 98048 | 89079 | 71497 | 64494 | 58280 |

| (% Growth – FY21 as base) | 10.07% | 24.59% | 10.86% | 10.66% | |

| Muthoot Gold AUM | 80922 | 72878 | 61875 | 57531 | 51926 |

| (% Growth – FY21 as base) | 11.04% | 17.78% | 7.55% | 10.79% |

Out of curiosity, checked the reason behind this growth in gold loan is that double the branches (i.e. more the branches, more the visibility & accessibility to borrowers – hence more loan growth). But it seems – here in last 3 financial years (in absolute numbers) Manappuram have added more Gold loan branches vs Muthoot (i.e. 497 vs 223).

| Absolute No. | Q1FY2025 | FY2024 | FY2023 | FY2022 | FY2021 |

|---|---|---|---|---|---|

| Manappuram – Gold Branches | 4044 | 4044 | 3985 | 3829 | 3547 |

| (% Growth – FY21 as base) | 0.00% | 1.48% | 4.07% | 7.95% | |

| Manappuram – Non Gold Branches | 1279 | 1242 | 1247 | 1228 | 1044 |

| Manappuram – Total Branches | 5323 | 5286 | 5232 | 5057 | 4591 |

| (% Growth – FY21 as base) | 0.70% | 1.03% | 3.46% | 10.15% | |

| Vs | |||||

| Muthoot – Gold Branches | 4855 | 4854 | 4739 | 4617 | 4632 |

| (% Growth – FY21 as base) | 0.02% | 2.43% | 2.64% | -0.32% | |

| Muthoot – Non Gold Branches | 1904 | 1687 | 1099 | 962 | 819 |

| Muthoot – Total Branches | 6759 | 6541 | 5838 | 5579 | 5451 |

| (% Growth – FY21 as base) | 3.33% | 12.04% | 4.64% | 2.35% |

Wondering what could be the reasons for such different pattern:

- Is it employees of Muthoot are more efficient vs Manappuram’s employee

- Muthoot Goodwill in customer is better vs Manappuram (may be because Manappuram auction more proactively vs Muthoot – my understanding basis management concall comments)

- Lending rate of Muthoot is more affordable vs Manappuram

- Muthoot branches are more strategically situated (to source better business) vs Manappuram

- or something else

Look forward to inputs from fellow forum members.

Vishnu Chemicals – Is Growth sustainable? (04-10-2024)

Key Takeaways from 31st AGM held on 27-Sep-2024

• Global customers are looking at India as reliable partner in the chemical space because of multiple reasons

• The company produces chromium and barium chemicals which are irreplaceable products in multiple industries due to unique characteristics

• Export and domestic sales mis has been historically around 50: 50 and currently around 45:55

• The company does not have domestic competitors having material scale. Competition in exports as well as domestically is from competitors based out of Turkey, Russia, USA, South Africa and Kazakhstan

• The company has flexible product mix and has been working on process innovations

• The company has been working on both forward and backward integration

• It has completed brownfield expansion for precipitated barium sulfate, which is used in multiple industries including power coating and battery. It’s an import substitute product and has achieved 60% utilization in first 12 months itself

• in FY24, the company acquired Ramadas Minerals for backward integration in barium segment. It has baryte beneficiation plant based on green technology and baryte produced from this plant is internally used as raw material for barium products. The plant is running at 90% production level now.

• In the current fiscal year, the company has acquired Jayansree Pharma to manufacture strontium carbonate. It’s a new (related) product and import substitute. It finds application in electronics and EV battery industry. Trial run and test marketing is completed and commercial production is expected from April 2025. This is expected to contribute about Rs.100 crore revenue in FY26, which is scalable to Rs.200 crore over a period.

• The company expects its revenue to grow by minimum at 20% CAGR over the next 3-4 years. Levers of growth are utilization of existing capacity (current utilization level of about 75%) and products such as strontium carbonate, sodium sulphide, chromium metals, special solvents organic chemicals which they are adding.

• Red sea issue has resulted in shipping challenges and higher transportation cost. Certain customers have also asked to delay dispatches. Inventory days have also increased due to this. The company is working on solutions and also exporting to other countries, which are not impacted by this.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

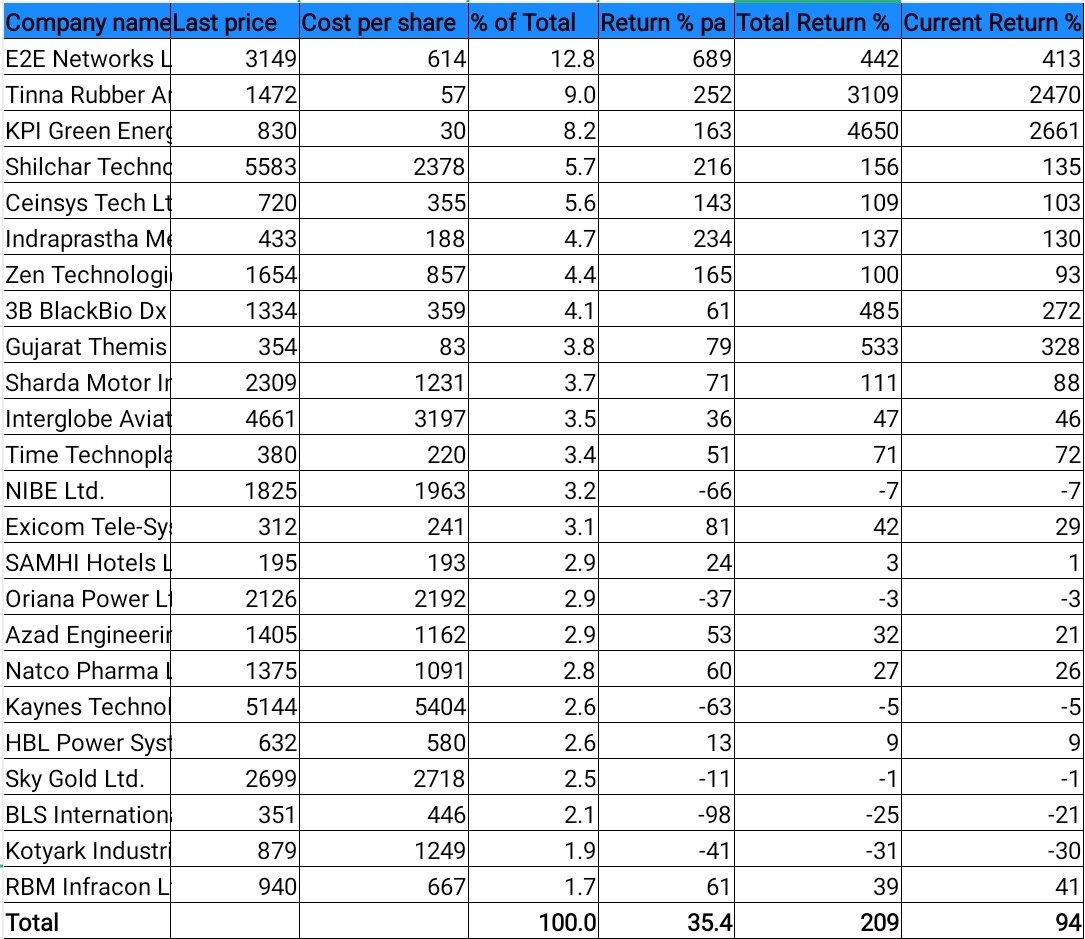

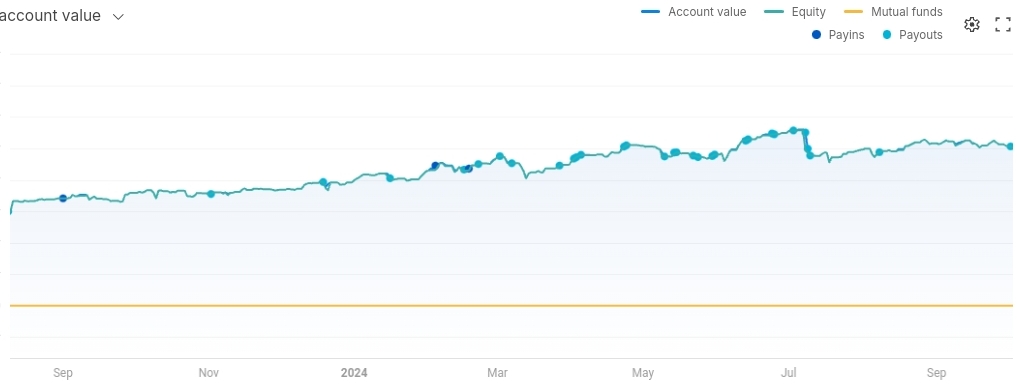

The Anti-Portfolio (04-10-2024)

Latest folio status:

CAGR approx 35% since inception, 7 years ago. Currently 2% down from previous peak (considering the withdrawn amount too in calculating). 90% up in past year.

Total 25 stocks.

Sold out Caplin and added Kaynes, it’s going to be a bit of patience games, can get stuck in losses for few months, very expensive. Kaynes is electronic manufacturing services provider, its setting up a chip testing and assembly plant soon, should grow due to the government subsidy. Caplin had reached a high point and was just a safety bet, pharma seems to be peaking now.

Seeking Guidance on Starting My Value Investing Journey (04-10-2024)

If you are saying value investing, it means that you wants to go that path, and that you have read something about value investing, and have some kind of a framework. You might have already bought some stocks based on your acquired knowledge. If yes, you can read about the threads on the stocks you bought, you can even find members who are inclined to value investing.

If you have not started your journey, you can try to find out what suits you, it need not be value investing, it could be HFT too, or it could be not just value investing, it could be a combination of value+growth. There are many options.

Either way, just like the market, this forum is big and rich with lots and lots of businesses discussed from different standpoints, financial and otherwise, by members with different perspectives. You can explore them. You can just start with IT threads, connect the dots between the intricacies of the business to price movement.

InterGlobe Aviation – Indigo (04-10-2024)

Disclosure in previous post.

InterGlobe Aviation – Indigo (04-10-2024)

Hi If that response was directed towards me, apologies to not make it clear. I am invested in Indigo and have add more of it too in recent fall. And yes, not invested in Spice jet.

To be clear, I’m putting up my views of both angles to Indigo – the positives ones and the threats one to remain aware of complete risk reward paradigm.