By looking at the Q2 numbers released by Gensol (Revenue of 314 Cr.) this maths doesn’t seem to be working very well.

Posts in category Value Pickr

Companies with 20%+ growth guidance for next few years (03-10-2024)

totally agreed sir.in these scenario I feel better stick on

1-technicals entry and exit with proper stop loss .

2-you have to take position in any script if the risk reward ratio is favor (if a stock is in continues up trend keep 21 DMA as a exit it may differ for others )

3-don’t go for bulk entry took staged entry keep pyramiding while stock showing strength

4-if it is not following you please position sizing

5-don’t exceed more than 5 Stocks in your portfolio (initially one can entry 10 stocks keep pyramiding while showing strength exit if not and reduce the number .try to concentrate the portfolio as much as possible with proper exit plan

6-only portfolio make you rich not stocks

7-creating wealth you need to have proper stock allocation system

Anant Raj Limited (03-10-2024)

I believe everyone invested in Anant Raj or data center theme should definitely watch this video.

The sophisticated infrastructure shown in this video and high standard of execution and even strict security required to build a data center put a lot of questions in my head regarding execution by Anant Raj Manangement.

Zomato – Should you order? (03-10-2024)

Can goverment bring some policy changes in Quick commerce which can hamper the business of Zomato? Also lot of employment depends on quick commerce. So goverment may not want to kill this growing space . Requesting members to share your thoughts .

Mudit’s Portfolio (Stage Analysis + Price Momentum) (03-10-2024)

paper_811.pdf (331.4 KB)

The implications of applying stop loss to rank based momentum

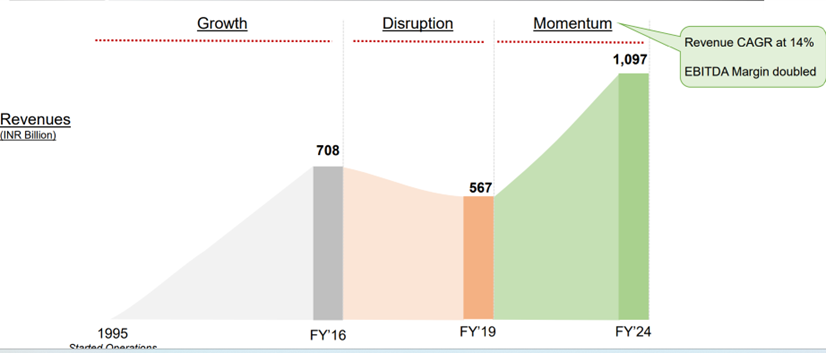

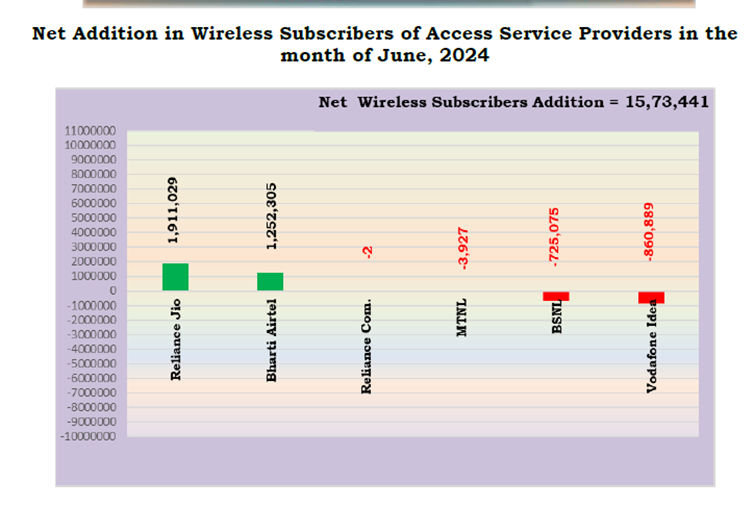

Bharti Airtel – What doesn’t kill you makes you stronger? (03-10-2024)

I have been following Airtel for a long time and it seems the company is at an inflection point. Two things that I heard from the few recent concalls that interested me are capex moderation and deleveraging. The company has been through a string of regulatory issues and a period of cutthroat competition.

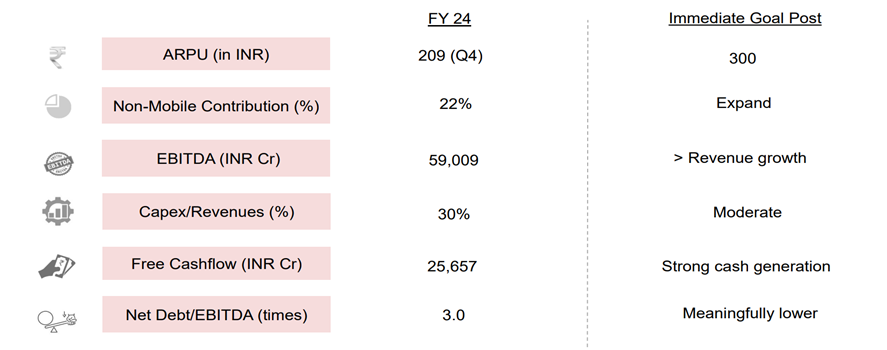

Finally, it seems like the overhang of the AGR crisis is over and tariffs have started to increase. From an ARPU of Rs 128 in 2020 the ARPU has increased to 209 in the last quarter. And management indicated that there is more scope for improvement in ARPU as management believes it will go to 300. India has one of the lowest ARPUs.

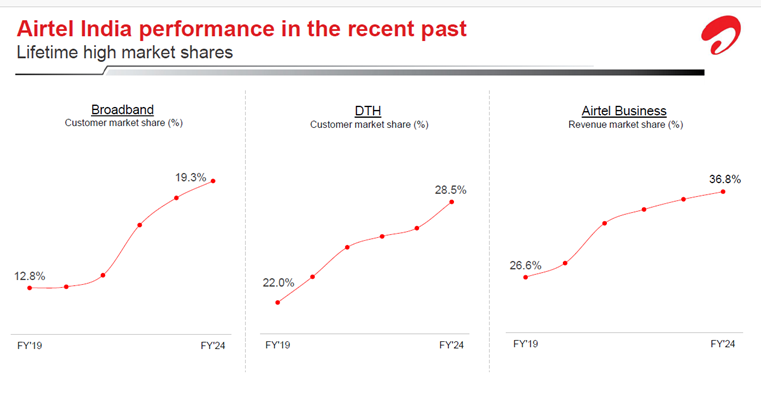

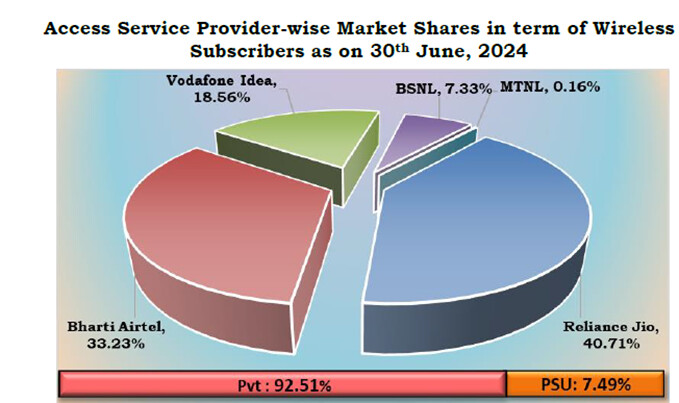

Airtel has been gaining market share in its core business.

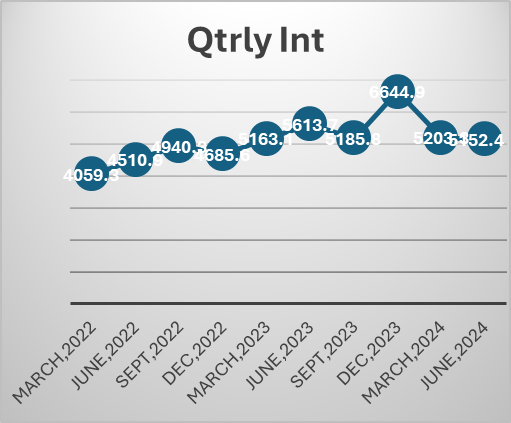

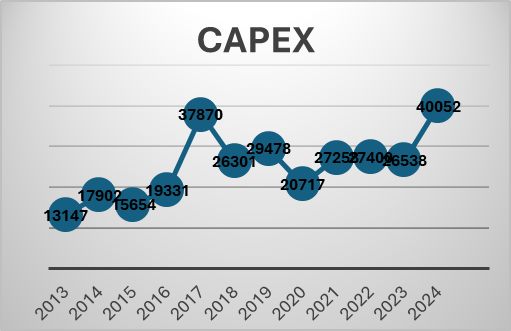

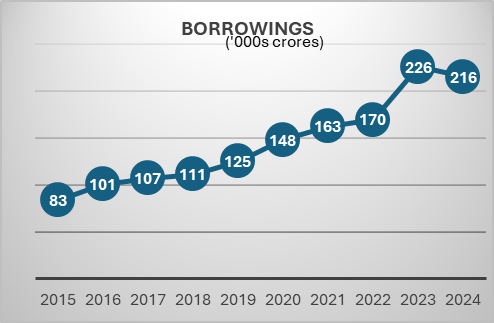

Telecom industry is characterized by very high regulatory capex. The company had to invest heavily in 5 G even before the benefits of 4 G roll out were realized. This has been the situation for long. The company had to raise a lot of debt for these purposes. But the situation has started to improve. Also, with a major part of 5g capex done we may see borrowings and interest costs coming down. The Company is also looking at paying down the high-cost debt. They prepaid spectrum liabilities of 24250 crores in the last year. Also, prepaid a spectrum liabilities debt of 8465 crores that carried an interest rate of 9.3 % in the current quarter. The interest expenses can be seen to be trending downwards in the last 2 quarters. Also, with interest rates coming down it will benefit further. Even though Airtel may look expensive on a P/E basis, it is trading at an EV/EBITDA of 14.8.

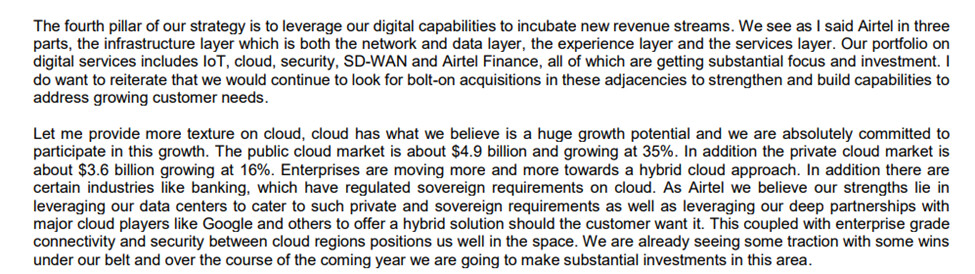

With the major part of this capex done. The company can now focus on their new age business, cloud, financial services etc. The company’s core business is going to produce a lot of cash which can be used to incubate new business opportunities. Last quarter the company made a cash profit of 16000 crores.

The company has a -ve working capital cycle.

Airtel Finance

On the payments bank, monthly transacting users stood at 71.4 million and the annualized revenue run rate is now over Rs.2,400

Crores growing 52% year-on-year. Deposits remain robust at over Rs.2,900 Crores again growing by over 50% year-on-year.

Airtel Finance is scaling up well with an annualized loan disbursement

of just under Rs.3,000 Crores and a loan book of Rs.3,300 Crores. They also launched FD marketplace. I think they understand the Indian markets quite well.

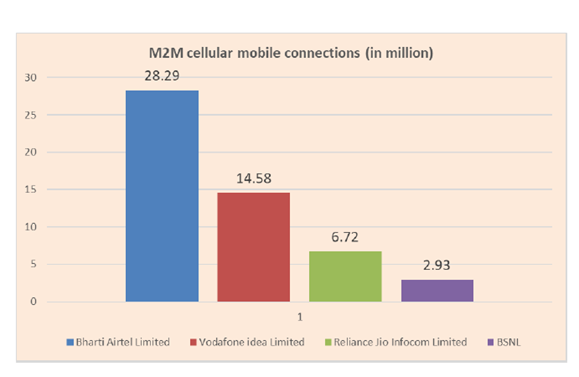

In M2M communication, airtel is currently having a dominant market share.

Kitex Garments Limited (03-10-2024)

did they confirm any valuation for the acquisition.

Manappuram Finance (03-10-2024)

You can set up a Google News alert to receive updates on Manappuram or any other company you follow every 24 hours. This way, you can check it once a day for the latest news.

Manappuram Finance (03-10-2024)

The next 12 months look promising for Manappuram and the gold market, with Goldman Sachs forecasting a rise in gold prices to $2,900 USD. Higher gold prices are expected to benefit gold finance companies. A recent RBI directive aimed at regularizing the gold loan sector will impact unregulated gold lenders. However, companies like Manappuram and Muthoot Finance have long been regulated and comply with most RBI guidelines. In cases where discrepancies arise, they have swiftly adapted, such as by implementing non-cash disbursements as required. Smaller players tend to take longer to adjust to these regulatory changes, making it harder for them to compete. Larger, well-established companies will thrive, while smaller ones may struggle due to the operational efficiency and high costs associated with running a gold loan business. Gradually, Manappuram and Muthoot are likely to gain more market share. In the past, companies engaging in questionable practices, like IIFL, grew rapidly. However, with tighter regulations, growth across the sector is expected to level out. Given the current conditions, Manappuram could see growth of 15-20% in medium term