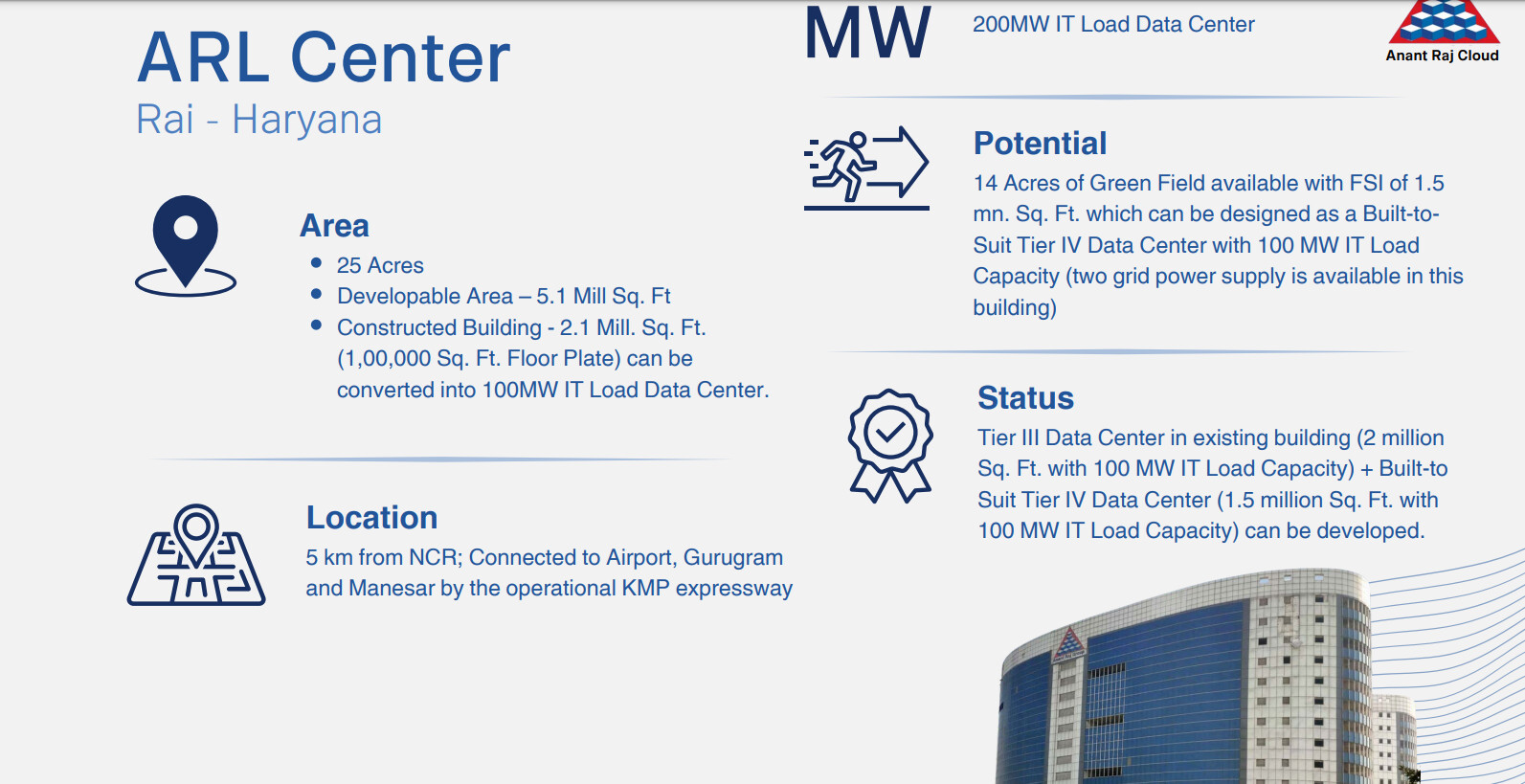

They have released the pictures of building in their latest presentation.

This gives me impression that they have physical infrastructure to execute the 300MW they are talking about.

Their business partner Orange business manage an extensive network of data centers which are integral to their global IT and cloud services infrastructure. These facilities support a wide range of services, including cloud computing, managed IT, and cybersecurity services, catering to a diverse client base from enterprises to government entities.

Given the physical infrastructure of Anant Raj and data center and cloud services of Orange I am quite confident that between the two they can implement the data centers they are talking about. They have already implemented 6MW.

I think Yotta is a older player and Anant Raj is a later entry into this business line.