While compare with its peers De Neers Tools found that iT

Taparia Tools valuation is very low and company fundamentals are good.

Posts in category Value Pickr

Taparia Tools – A Micro Cap. Company with Mighty Financials at Mightier Valuation (29-09-2024)

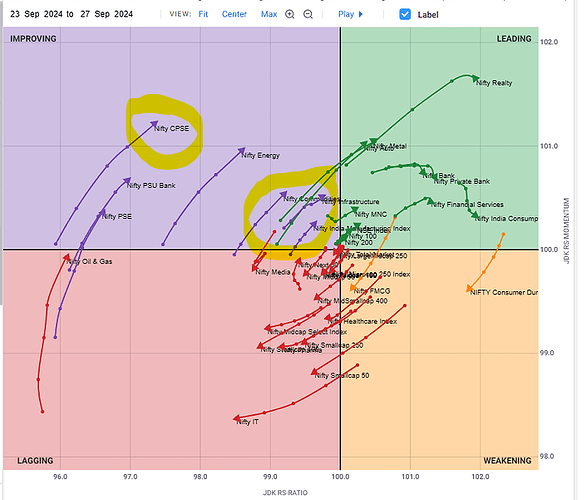

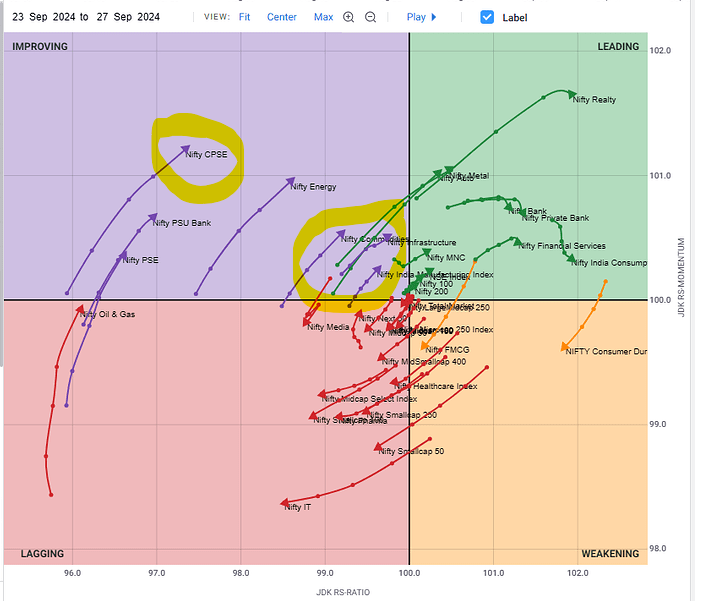

Relative Rotation Graph (29-09-2024)

Thank you @insiderTrader for this valuable information. SInce I am beginner and in learning phase I have couple of questions.

- Where can I see these Graphs ) Any free/Paid portal that provide the insights and trends?.

- As shown in picture few indices are far right and big and few are very close and short. I have highlighted in picture below. How this is detrmined. Is this based on Capitla it holds or no of stocks or what. Why I am asking this is if you look at graph indices close to center point are short and very quick to swift the trend where as indices far end usually take time to move from one quadrant to other quadrant right.

- Will the direction of rotation always clockwise or anti clock wise can also happen?

- This Graph helps mostly for Momentum/ Swing traders right. yes for long term investors in weakening/Lagging quadrants are the accumulation period. This also help in taking entry/exit positions.

- What are the major factors impacting these rotations like micro economics macro economics, Govt policies…etc.

Neuland Laboratories Limited – Transformation towards niche APIs? (29-09-2024)

Oh i missheard it. Thanks for pointing out

IDFC First Bank Limited (29-09-2024)

@Vineet_Bhatia : Management has guided for CI ratio of 65% for FY 27 , Secondly Cost of deposit is lowered assuming paying off all legacy liabilities in next 2 years and lowering of saving deposit rates by bank due to fall in interest rates and lesser deposit needed by bank

Ranvir’s Portfolio (29-09-2024)

Jash Engineering –

Company overview and Q1 results highlights –

An engineering company making critical products for Fresh water and Sea water intake systems, fresh water and waste water pumping stations, de-salination plants, storm water pumping stations, hydro-power generation and also for manufacturing industries like – Steel, cement, Paper & Pulp, Petrochemicals, Fertilizers and other process plants

Product portfolio includes –

Water Intake systems – Like – Penstock gates, Open channel gates, Downward opening Weir gates, Flap gates, Stop Logs

Heavy fabricated gates – Bulkhead slide gates, Roller gates, butterfly gates, Crest gates, Radial / Tainter gates, Bonneted gates

Coarse screening equipment – Trash rack, MMR screen, MultiRake screen, suspended trash racks

Fine Screening equipment – Screenmat step screen, Rotoclean rotary drum screen, Rotobrush Rotary screen, Mahr Perscalator screen, Travelling band screen

**Gate Valves **

Solid Bulk handling Valves

Special purpose Valves

Process equipments like –

Water clarifiers

Detritors

Slow speed floating aerators

Slow speed fixed aerators

Hydropower Screw generators

Screw Pumps

Filtering equipment

Secondary treatment Equipment like –

Diffuser aeration

Mixing and Aeration equipment

Decanting equipment

Turbo Blower

Products wise revenue contribution in Q1 FY 25 –

Water control gates – 49 pc

Screening equipment – 31 pc

Valves – 13 pc

Hydropower, Pumping, process equipment and others – 7 pc

FY 24 financial outcomes –

Revenues – 521 vs 415 cr

Gross profits – 311 vs 243 cr ( gross margins @ 59 vs 58 pc )

EBITDA – 105 vs 77 cr ( margins @ 20 vs 19 pc )

PAT – 67 vs 52 cr

RoE – 19.7 vs 21.7 pc

Q1 and Q2 are generally soft for the company. Company drives bulk of its business from Q3 and Q4

Q1 FY 25 financial outcomes –

Revenues – 116 vs 65 cr ( up 78 pc )

Gross profits – 60 vs 39 cr, up 52 pc ( margins @ 51 vs 60 pc )

EBITDA – 5.2 vs 1 cr ( margins @ 4.5 vs 1.4 pc )

PAT – 0.1 vs (-) 3.4 cr

Company’s order book as on 01 Aug 24 –

Jash Engineering – 553 cr

Rodney Hunt – 365 cr ( their US subsidiary )

Waterfront fluid controls – 21 cr ( their UK subsidiary )

Total @ 939 cr

Order pipeline (under negotiation and in final stages) @ 103 cr

Revenue guidance for FY 25 @ 675 cr

A new construction facility measuring 60k Sq Ft is under construction at Shivpad, Chennai. Likely to be commissioned by Feb 25. At peak capacity utilisation will contribute to aprox 100 cr of revenues

Capex lined up for FY 25 @ 29 cr

Areas like – Storm water and flood prevention, Desalination, Rising sea levels, Wastewater treatment and re-use are likely to open up exiting new possibilities for the company

Company – at present operates via its 6 manufacturing locations – 04 in India, 01 each in UK and US. Current employee strength @ slightly above 1000. Company is approved by most municipal authorities in India and Abroad. These approvals are extremely critical in the company’s line of business

Overtime – company has made 04 major acquisitions – Rodney Hunt ( US ) , Waterfront ( UK ), Shivpad ( in India and Mahr Maschinenbau ( in Europe )

Shivpad was acquired to help in treatment process equipment

Mahr Meashinenbeu was acquired to get bet screens technology in the world

Rodney Hunt was acquired for their brand value in US

Waterfront was acquired for their penetration in the UK mkts

Company’s current facilities have a revenue potential of 800 cr. Aim to take it up to 1000 cr by next FY

Company does perform a lot of their manufacturing functions – in house – which gives them critical advantage over competition

Company has a technical collaboration with Invent ( Germany ) to make Disc Filters and have already started manufacturing the same

Equipment like – diffusers, Mixing and Aeration equipment, Decanting equipment, Turbo Blowers are recent additions to company’s products portfolio

Company executed some legacy orders from its Rodney Hunt subsidiary in Q1. These had thin margins. Future pipeline of Rodney Hunt has much better profitability

As the company’s turnover keeps rising, even Q1,Q2 will start to report descent profits from FY 26 onwards

Company is likely to overshoot its revenue guidance of 675 cr given in the beginning of the year. Revenues may go upto 700-720 cr range ( contingent on customers taking delivery of materials in Mar 25 )

Over and above the expansion at Shivpad( Chennai ), company is undertaking expansion of its Unit -4 by another 64k sq ft @ cost of 23 cr. This again, has the potential to add 100 cr to the company’s bottomline

At present, company is not doing its screens business in US. US business is currently restricted to various types of gates. Now that the company has been able to turn around Rodney Hunt, it plans to introduce screens in US as well. One advantage that company has is that Mahr – brand is well known in US, hence products approvals should not be a problem for them

Singapore has earmarked resources worth 6000 cr for electrotechnical equipment to be deployed over next 10-15 yrs to combat rising water levels. This business should start flowing wef next FY. Jash engineering should be a beneficiary

In a typical waste water treatment plant, money is spent on civil works and electrotechnical equipment. On an avg, company’s share of value in any such project is around 5-10 pc of the total project cost

Company believes, as of now the GoI’s focus on water related infra is not at levels that it should be. However, as govt’s focus in this area improves – it can be great times for the company

Company has started to increase its focus towards waste water treatment business – hence their latest technical collaboration with Invent ( Germany ) to make disk filters, canisters, diffusers, Turbo blowers etc. At present there are certain differences of opinions between Jash and Invent about the JV’s strategy. Invent wants to do low volume / high margin business whereas Jash is trying to convince them to go for higher volumes. According to Jash’s management, it may take another 6-12 months for the opinions to converge

At present 3-4 additional jobs are under negotiation that the company is actively involved in. Each order is of the magnitude of aprox $ 5-15 million

Company has guided for a 1000 cr topline by FY 28. However, if the business buoyancy is good – they may achieve it sooner

Disc : not holding, tempted to add on dips, looks like a promising company, not SEBI registered, not a buy / sell recommendation

Samhi Hotels – Turnaround with Tailwinds (29-09-2024)

Do corporates borrow at floating rate or fixed rate? I used to think it was always fixed.

Companies with 20%+ growth guidance for next few years (29-09-2024)

Can you give some examples of guaranteed 25% returns with no risk of loss of capital?

Sakar Healthcare – Tiny Pharma Company for promising Growth ahead (29-09-2024)

Nothing much happened in the AGM, but I am giving some information below.

Du Pont analysis is the past but market discounts the future. Sakar has setup a Rs.250-crore plant which includes an API, formulations and R&D facility dedicated to Oncology. The unit has received WHO GMP and EU GMP certifications. Revenues from Oncology have just begun and are not captured in current financials.

Last year, a contract with PharOS of Greece was signed in May for product development (mentioned as among the Top 10 products in Oncology). The product has been developed successfully by the company’s R&D and bioequivalence studies by the customer will get initiated soon. I believe some milestone payments have already been received for the same. Similarly, contracts with Ferring Pharma and Bazell Pharma of Switzerland for development and supply of two Oncology products have also been signed last year, and the Annual Report mentions validation work is going on. Currently, company has 6 products are under development in oral solid and 7 in oral liquid category in Oncology alone. Most of these products are either in validation or in accelerated stability study phase. Meanwhile, for the export markets, regulatory filing has been done for 17 product registrations till now in the EU and 10 in Latin America, Southeast Asia, Africa. Work is in progress on another 28 product dossiers. Nine agreements have been signed internationally on Oncology products of which 6 are in Europe / UK. In the domestic markets, 10 agreements have been signed in India. Commercials have started with 9 customers, and this will go up to around 12 by FY25 end. Approvals from EU are expected to start coming in from Q4 of this year. In addition, company is also in discussion with several potential customers for strategic tie-ups.

Meanwhile, rest of the business (non-oncology) is expected to grow at 7 to 8 % in line with the market growth. Here, Sakar in mainly doing CDMO / outsourced manufacturing for customers such as Zydus Lifesciences, Intas, Emcure, Glenmark, Torrent etc. I believe Zydus is the main customer. The Annual Report mentions technology transfer from Zydus Life Sciences for 23 SKUs of Oral Solids and 19 SKUs of injections, besides some others such as API supply to Jodas and Meta Life Sciences. Sakar does not market its own brands in the domestic market.

Overall, till date in FY25, filing has been done for 33 product registrations in all (including 17 mentioned above) & 4 registrations have been received. By the end of this financial year, dossier submission is expected reach 50. Company now has 290 product registrations in its own name and 321 registrations in all. Pharma is a long gestation business, it takes years to set a facility, file for product registrations, get approvals, sign customer contracts and revenues to start flowing in.

In FY24, Oncology revenues were just Rs.30 crore of the total of Rs.150-odd crore revenues. Going ahead, Oncology revenues are expected to double in FY25 and touch around Rs.100 crores by FY26. Once the product approvals start coming in, company expects to generate Rs.500 crores from Oncology alone over three years. Moreover, these will be at a higher margin of around 28 to 30 % compared to the existing business.

So, a lot of work has been happening which is not reflected in the current financials. The management has raised equity funding along the way which has kept debt levels under control. I have been invested in the stock for nearly four years now, and so far, I find the management has executed well. Last year, Tata Capital took a stake in the company, providing a stamp of approval for the business. All these expectations are factored in the current valuations.

Companies with 20%+ growth guidance for next few years (29-09-2024)

Sorry to be a party pooper but I just want to add a different perspective to this discussion.

Best way to invest in micro-caps of unknown provenance is to answer the following question.

Between two investment options where First gives you 100% return with 75% probability of losing your money and Second gives 25% guaranteed return with no loss of capital, which do you think is better option?

Rational folks will say that both options are equal.

However in investment world many retail investors believe option 1 is better as they only look at potential return (100%) and ignore risk premium (75%). This is what drives rush for micro-caps stocks because they can rise really fast in a bull market when there is a relentless gush of liquidity in the market. But when liquidity dries down, and often without advance warning, drawdown can be severe.

On the other hand high quality companies with a track record of building moated businesses, credible management and strong cash flow generations are ignored because they over long time compound money ONLY at 15-18% (not exciting for someone looking for a multi-bagger in 1 year). One of the reasons they are avoided by retail investor is that they are “well discovered” names.

In my long association with equity market (since before dotcom time), I have seen quite a few bull markets. One consistent principle across all of them, I have seen playing out, is the belief that one wouldn’t lose their capital in micro-cap stocks because of quality of their research or will be able to get out of them in time with good returns. Part of that confidence comes from analyses done on reports, commentary and exciting growth guidance given by the management which during a bull market can be very credible.

I am not an Oracle but by simply extrapolating history I will confidently be able to bet that 20% of the companies giving 20% growth guidance will not survive next 10 years and another 50% will be average investment giving returns not justifying the risk premium. Only a handful will probably make their investors make money.

Not all micro or small cap investments are bad. But evaluating management’s ability to execute well and good intentions to act in shareholders’ best interest is much much harder than many people think it is. There is no free lunch in equity market. More money in short time comes with a lot of risks and some catastrophes.

Neuland Laboratories Limited – Transformation towards niche APIs? (29-09-2024)

I think you misheard, but the news reporter is saying “nineteen” thousand and not “ninety”, since she’s talking about a 47% upside from the current ~13K price