I am new to the valuepickr forum and i am still figuring it out. So will defientely keep it in mind to post on exisiting threads

Posts in category Value Pickr

IDFC First Bank Limited (28-09-2024)

In case of HDFC Bank: HDFC merger, all the F&O contracts of HDFC were terminated 2 days before the record date. The same is expected to happen in IDFC.

IRB INVIT TRUST- new game in the town! (28-09-2024)

I think we need to differentiate rating of InvIT trust from InvIT unit investment. The AAA rating is to debt taken by InvIT to finance assets and they have supeiror claim over InvIT unit holders. InvIT unit is broadly comparable to equity. Do we consider credit rating of debt company and yield of debt paper as quasi equity return? No, in my view. Similarly, investor in InvIT is taking business risk and hence can not consider as debt investors. The interest on loan of IRB InvIT is around 8% which is equivalent to AAA credit rating paper for debt investor. Yield of 13-14% is not certain and would undego change with toll change, traffic change, interest change, asset termination due to ageeement and foced event (likr Pathankot road closure in farmer protest). The additional 5% yield to invIt investor is to assume all other listed and many unknown unlisted risk. This is my view and may be wrong. However , would advise members not to consider credit rating of InvIt trust and current yield on InviT unit as same have differnt risk profiles.

Swiggy – unparalleled convenience (28-09-2024)

@Vivek_Kalavadiya

Any idea how much cash swiggy has before IPO? I remember somewhere I read about 5-6K but not sure. Thanks

Microcap momentum portfolio (28-09-2024)

I see small differences. Some differences in sequence and instead of TARC (is at 26), I have JCHAC in my pf.

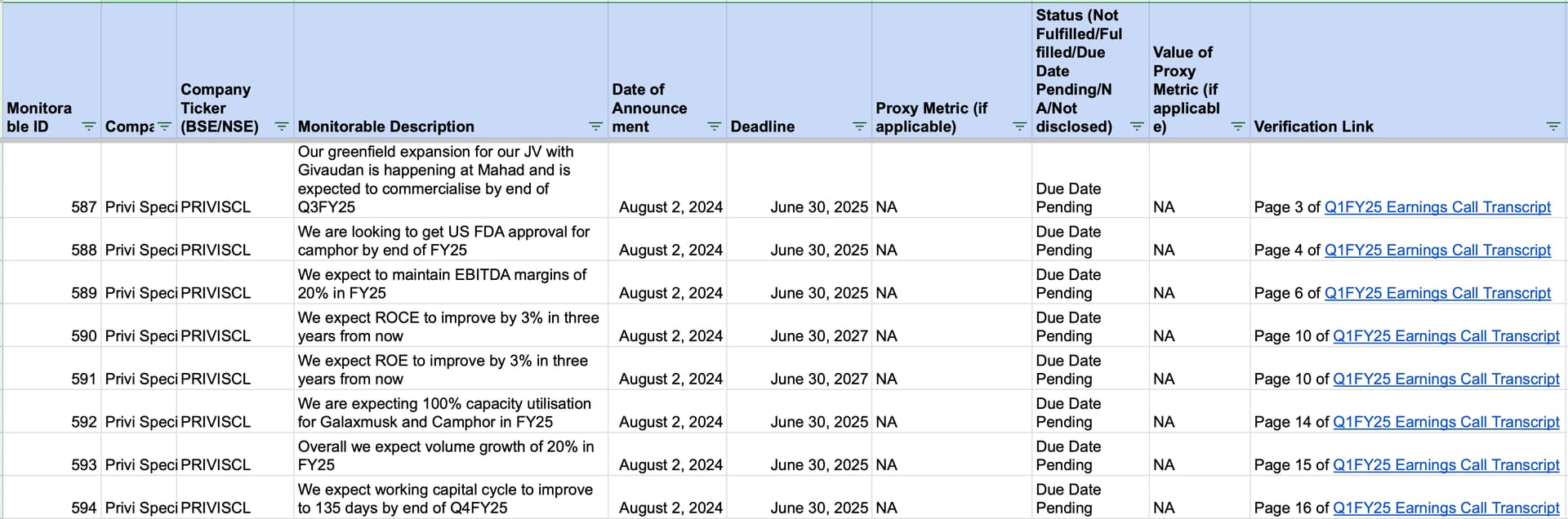

Privi specialty chemicals – Waste to wealth story (28-09-2024)

In the below tracker, I have started tracking important company goals for Privi. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-8.xlsx (157.6 KB)

Smallcap momentum portfolio (28-09-2024)

@Mudit.Kushalvardhan In our list from last week, only Godfrey Philips was present. Sobha, Bombay Burmah and First Source were not present. So, we are not missing much really.

Similarly, in our microcap pf, Sarda and Zentec are not present. So, we have not lost anything.

IDFC First Bank Limited (28-09-2024)

Hi,

Can someone please help me with this query?

I have bought October futures of IDFC Ltd. What will happen to those and how should I proceed?

Great articles to read on the web (28-09-2024)

If you’re looking to dig deeper, read the enclosed compilation of his selected blogs in one pdf.

Anand Sridharan blogs.pdf (4.3 MB)

P.S. i have read most of his blogs 10+ times and have personally benefited greatly (cognitively, financially, and psychologically) from Anand’s writings.