Look like Ram is not sure of numbers.

Posts in category Value Pickr

Goodluck India Ltd (20-11-2024)

Look like Ram is not sure of numbers.

About the Equity Job Openings category (20-11-2024)

Hey Salman, I was looking to get into equity research fresh out of college . Would love to connect and have a discussion.

How to take leverage to go long in market (~2 years)? (20-11-2024)

If it pays off please comeback and tell us your process , incase you fail still come n tell what mistakes to avoid, cause even I will be leveraging in downward market.

Vinati Organics (20-11-2024)

18.11.2024 CNBC (link)

- Most products saw volume improvement

- ATBS: 40% of Q2 revenues

- Anti-oxidants and butyl phenols have seen 30-40% volume growth

- Anti-oxidant approvals have taken longer than expected + more Chinese competition. Trying ADD for this range of products

- Hope for 20% sales and EBITDA growth in FY25 and FY26

Disclosure: Invested (bought shares in last-30 days)

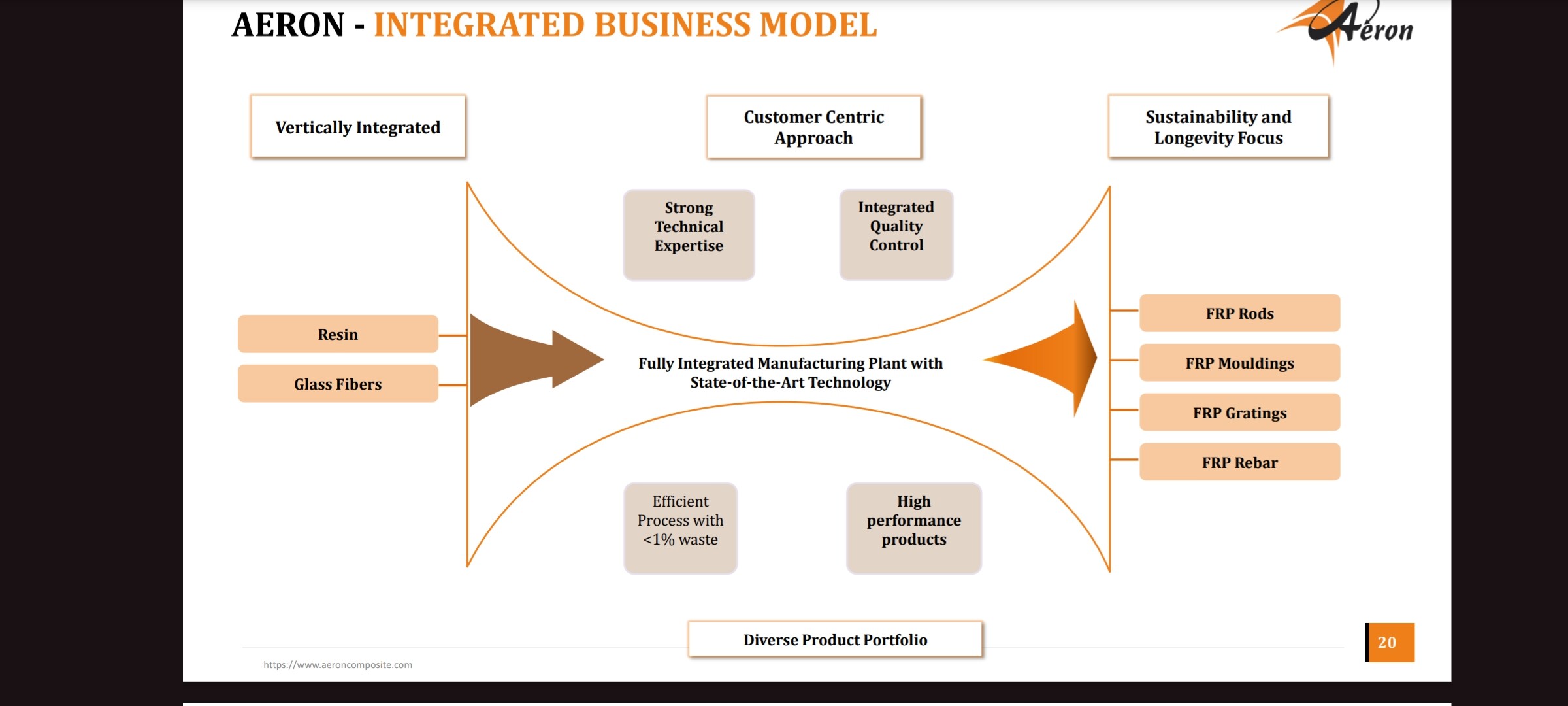

Aeron composites limited (20-11-2024)

Aeron composites limited

Market Cap: 214 Cr.

Stock P/E: ~19

ROCE: 36.5 %

ROE: 33.2 %

CMP: 126

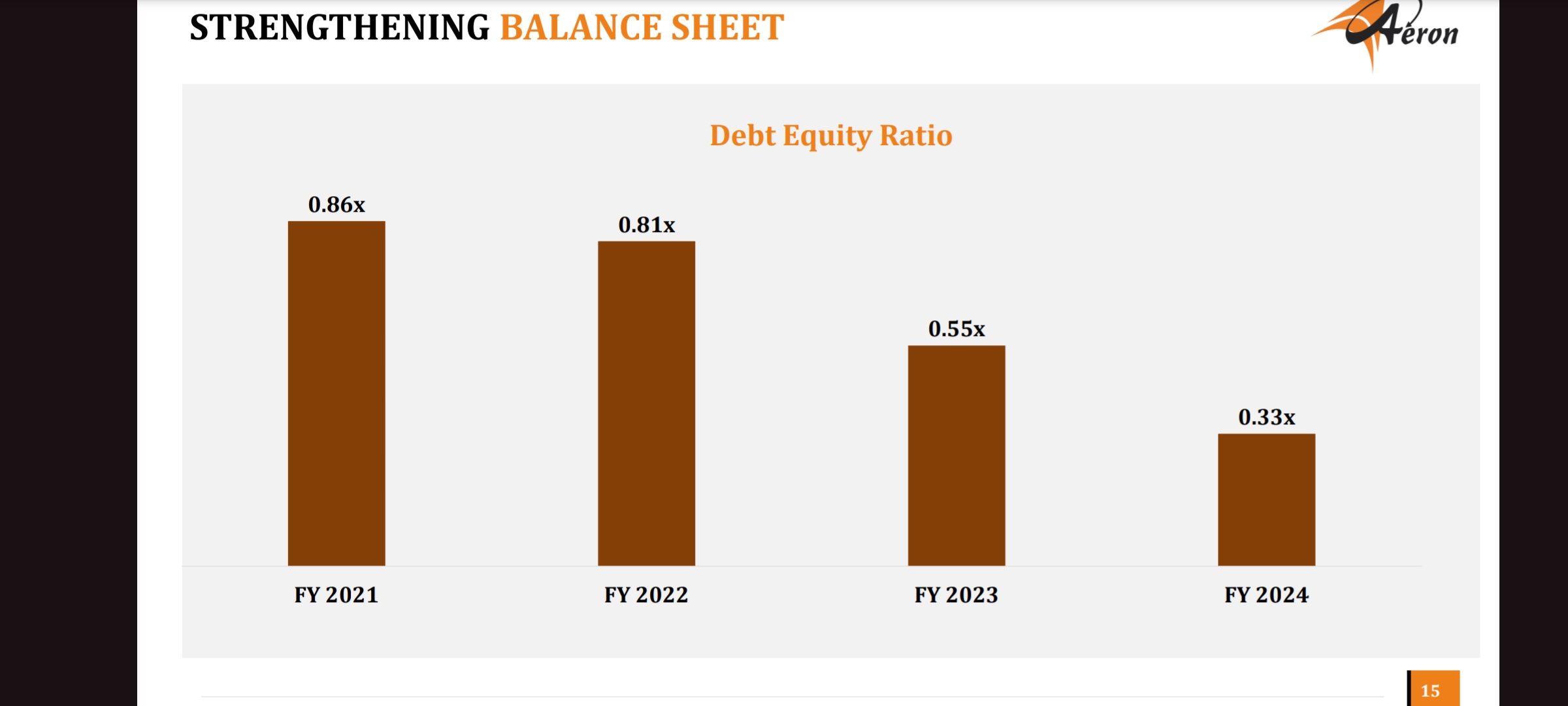

Debt to equity: ~0.35

CMP: 126

Promoter holding: 73.63%

Note: have taken most of the data from the company’s website, annual report, investor presentation and drhp.

• Introduction:

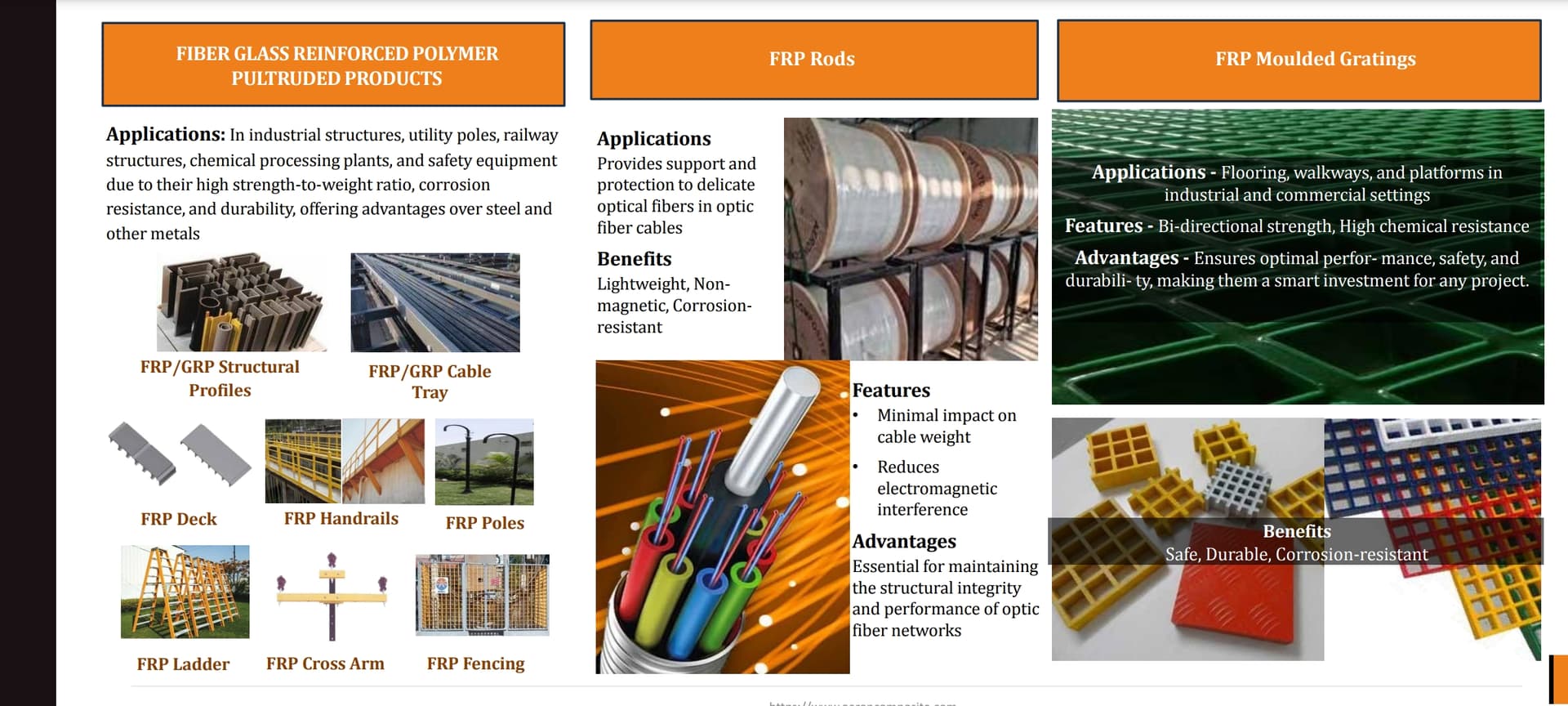

Aeron composites limited was Established in 2011, manufactures and supplies Fiber Glass Reinforced Polymer (FRP) products, including FRP pultruded products, FRP molded gratings, and FRP rods, tailored for various industrial applications. Basically the company makes products which are a potential replacement to traditional building/construction materials like steel, wood etc.

• Clients:

• Industry and product:

In recent years, fiber-reinforced polymer (FRP) has become a widely accepted alternative to traditional building materials like metal and wood. The composite consists of a polymer resin matrix reinforced with fibers, which results in a durable but lightweight material. These qualities make it suitable for use in a wide range of structural applications, from bridges and boardwalks to poles and piles.

FRP is available in many variations, each of which exhibits unique characteristics that make it suitable for particular applications. Additionally, the material can be worked in a variety of ways to suit different structural requirements and restrictions.

One can read this document from the dcmsme government website to understand in detail, the economics of frp business

DOC-20241121-WA0000…pdf (45.3 KB)

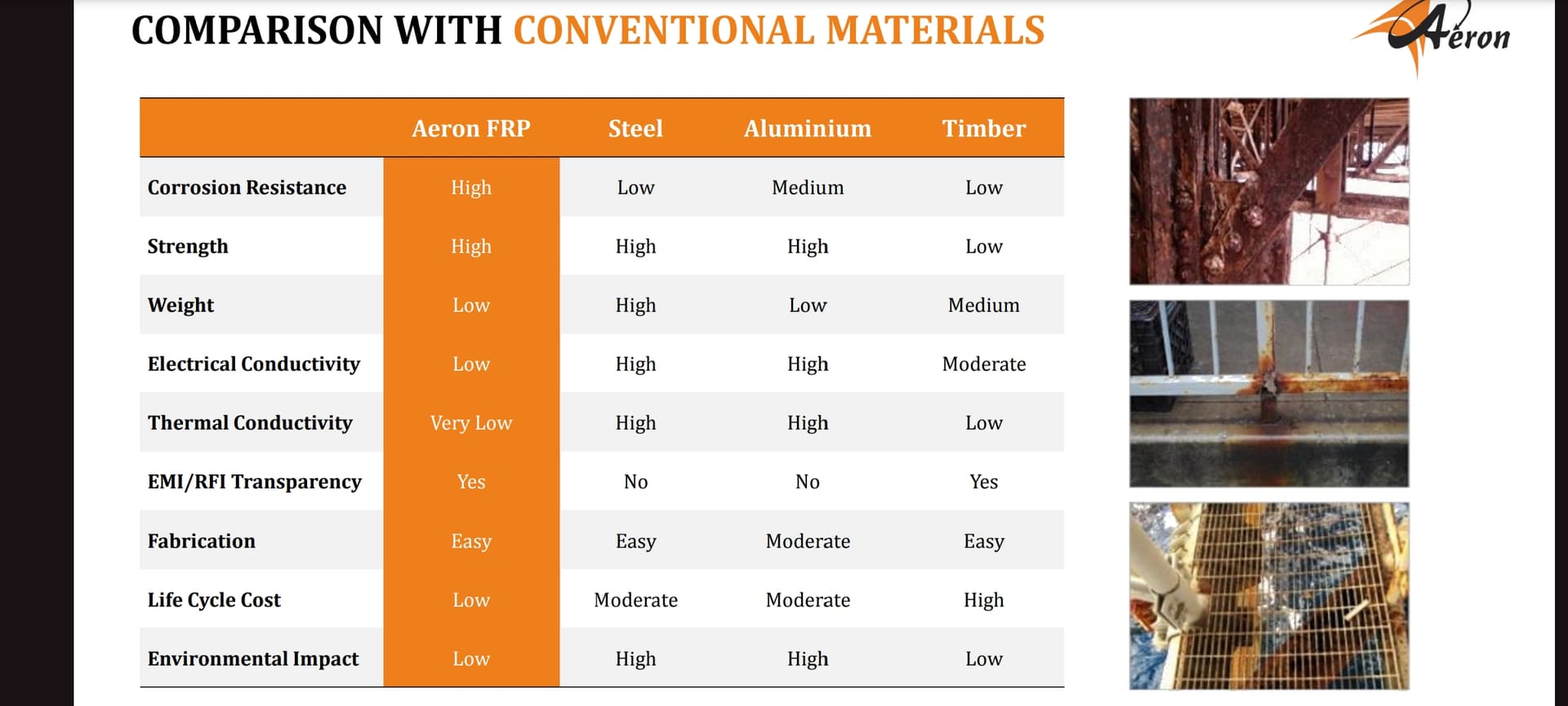

Key benefits of FRP Products include:

Corrosion Resistance, Impact Resistance, Light Weight, Better Ergonomics, Easy Installation, low maintenance, long lasting, High Strength, Electrical Non

Conductivity,Thermal Non

Conductivity, Termite

Proof, Less Environmental

Impact.

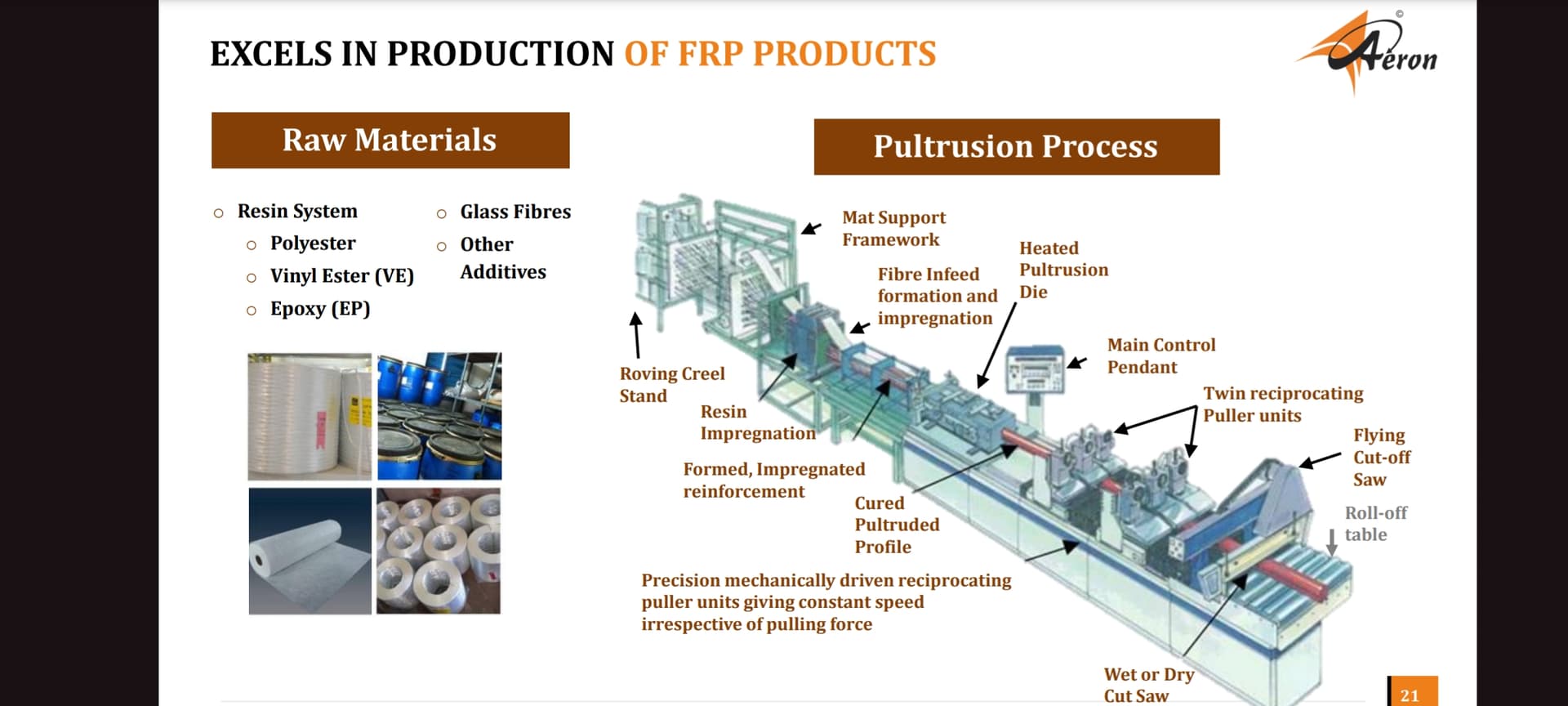

The production methods used by Aeron Composite Limited are Pultrusion and Moulded Gratings.

Pultrusion is the process of pulling fiberglass reinforcements such as mats and strands through a proprietary resin and heated die. The result is a specific complex profile that can be cut to any length. This process offers speed and consistency making it the best method for producing high-volume linear fiberglass products that require constant cross sections.

Poltrusion process:

Pultrusion. FRP Manufacturing. Plastic Process Technology. Fibreglass composites.

⚙️ Pultrusion, how it works – Epsilon Composite

GRP/FRP Gratings are produced by wet moulding and hot curing in a heated mould. The reinforcement consists of continuous fibreglass rovings in alternating layers, so the loads are distributed evenly in all directions. Regularly Moulded GRP Gratings have a polyester resin matrix. Glass content is approximately 35%.

Frp molded grating process:

Production Process of FRP Molded Grating

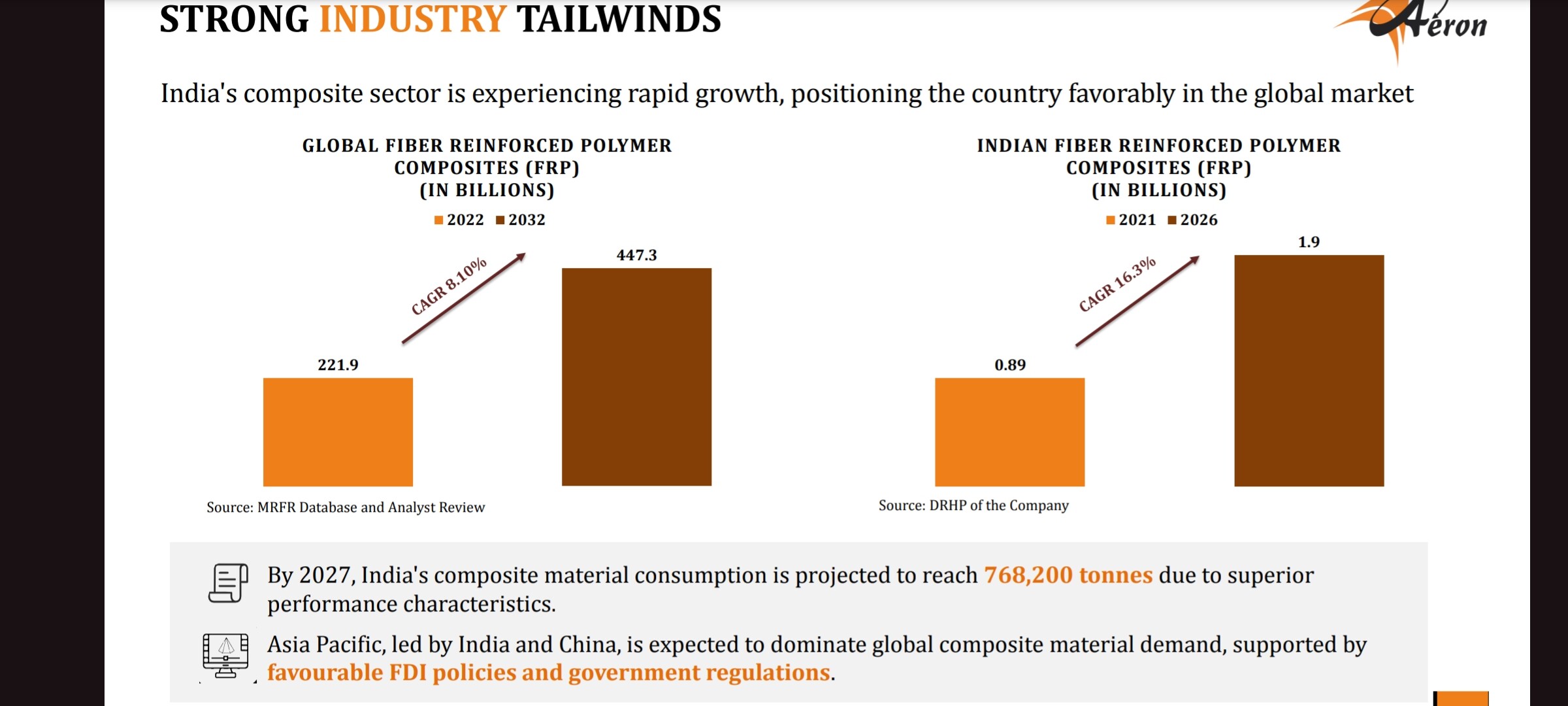

Global frp industry market size analysis:

According to aeron composites promoter the market size of frp products/ composites in india is ~16,000 crores

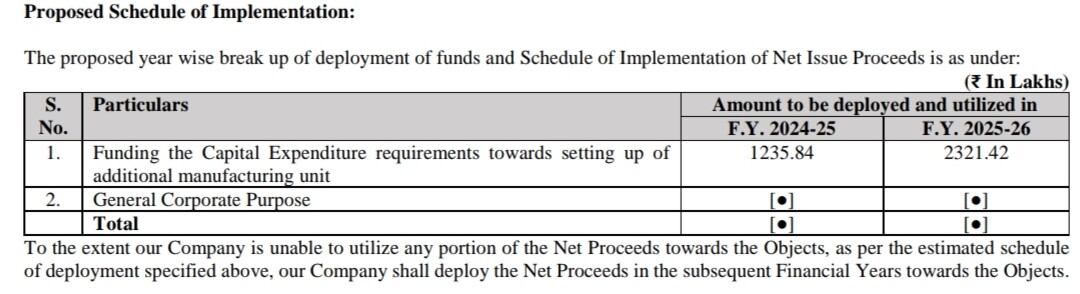

• Ipo details and Objects of the issue:

It was a fresh issue of Rs 56.10 crores at a price of rs 125 per share.

• Financial statements:

P&l

Balance sheet

Cash flow statement

• No listed peers to compare

•Valuation:

Pe ratio: ~19

Market cap to sales ratio: ~1

EV/EBITDA: ~ 10.7

Peg ratio: ~0.5

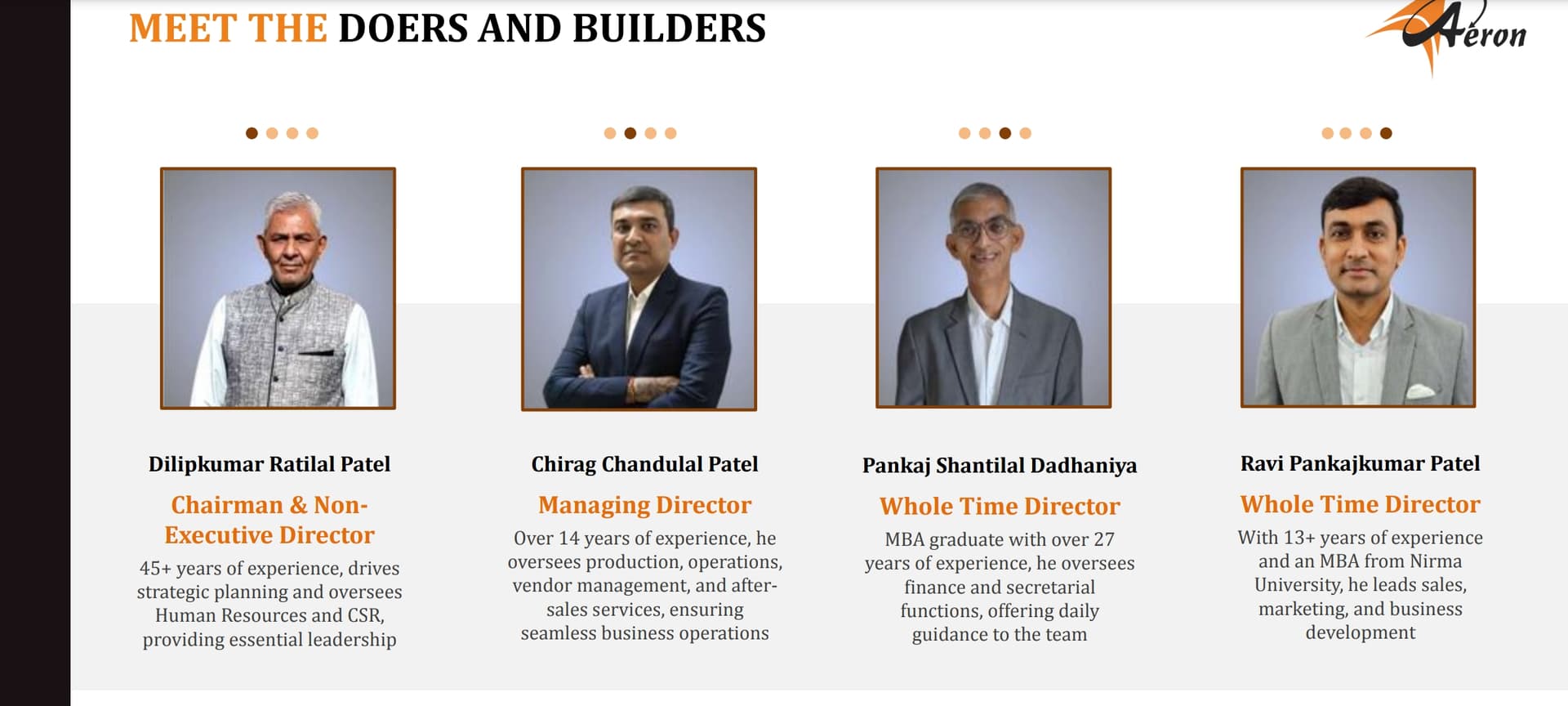

Management:

Aeron Composite Limited is a part of ‘A GROUP’

‘A GROUP’ is in business of Ceramic refractories, FRP/ GRP Composites, Ceramic Tiles, Waterjet & Laser Cutting machine, Paints and Lime.

Less info available on management.

Investment thesis/ key triggers/ positives

-

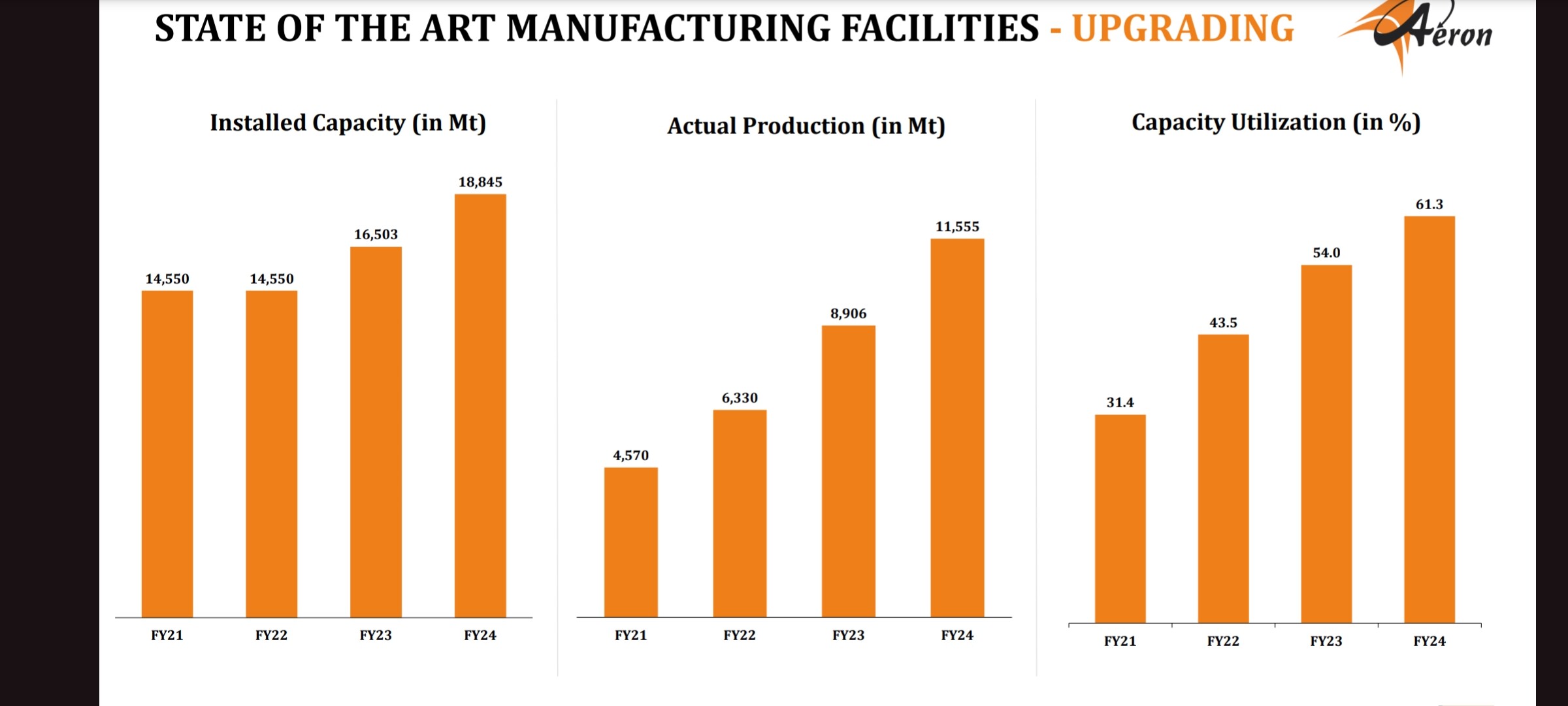

Strong financial growth

From FY2021-FY2024

Revenue cagr: ~36%

Net profit cagr: ~50%

Available at ~19pe

(Growth at reasonable valuations). -

Increase in capacity utilisation over the years and ~36% volume growth cagr from FY2021-2024 which means that increase in revenue was completely led by volume growth and not price/value growth.

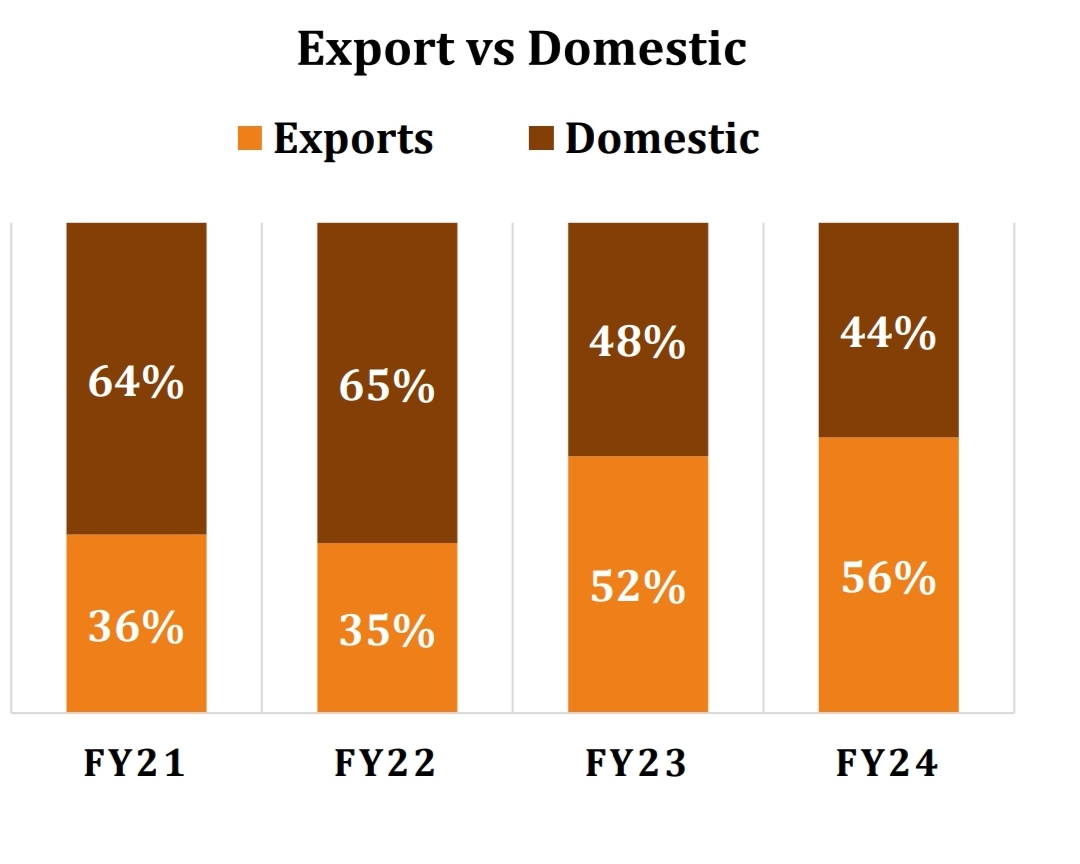

- Percentage of export revenue is increasing. In H1 FY25 domestic revenue grew by ~13%, export revenue grew by ~48%.

-

Strong sectoral tailwinds can arise due to increase in capital expenditure in various industries and increased investment in infrastructure, huge potential market as it can potentially replace traditional materials like steel,wood etc. in some of the infrastructure applications.

-

Deleveraging

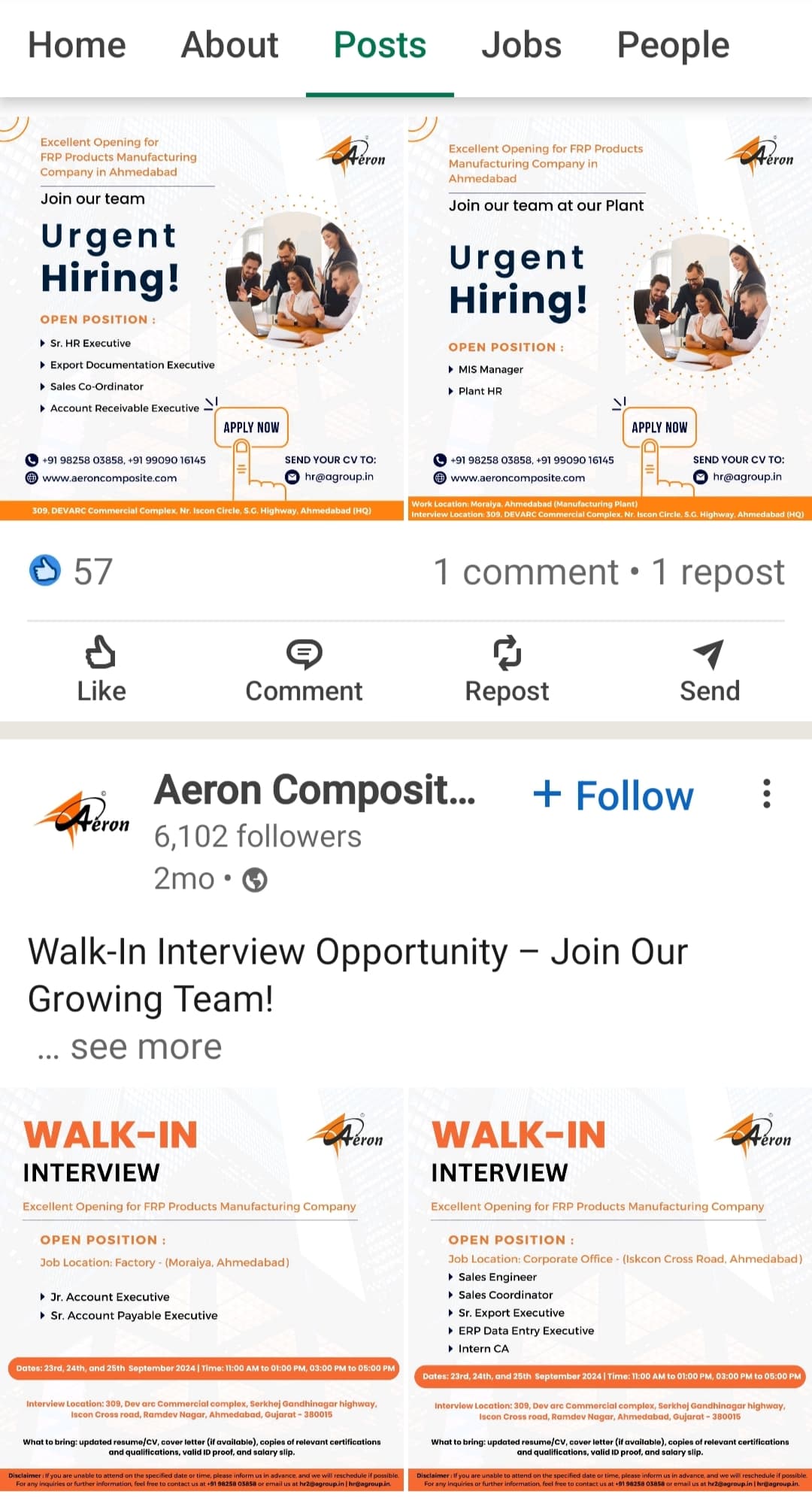

- Increase in Employee benefit expense and recent hiring posts on LinkedIn (positive considering the size of the company)

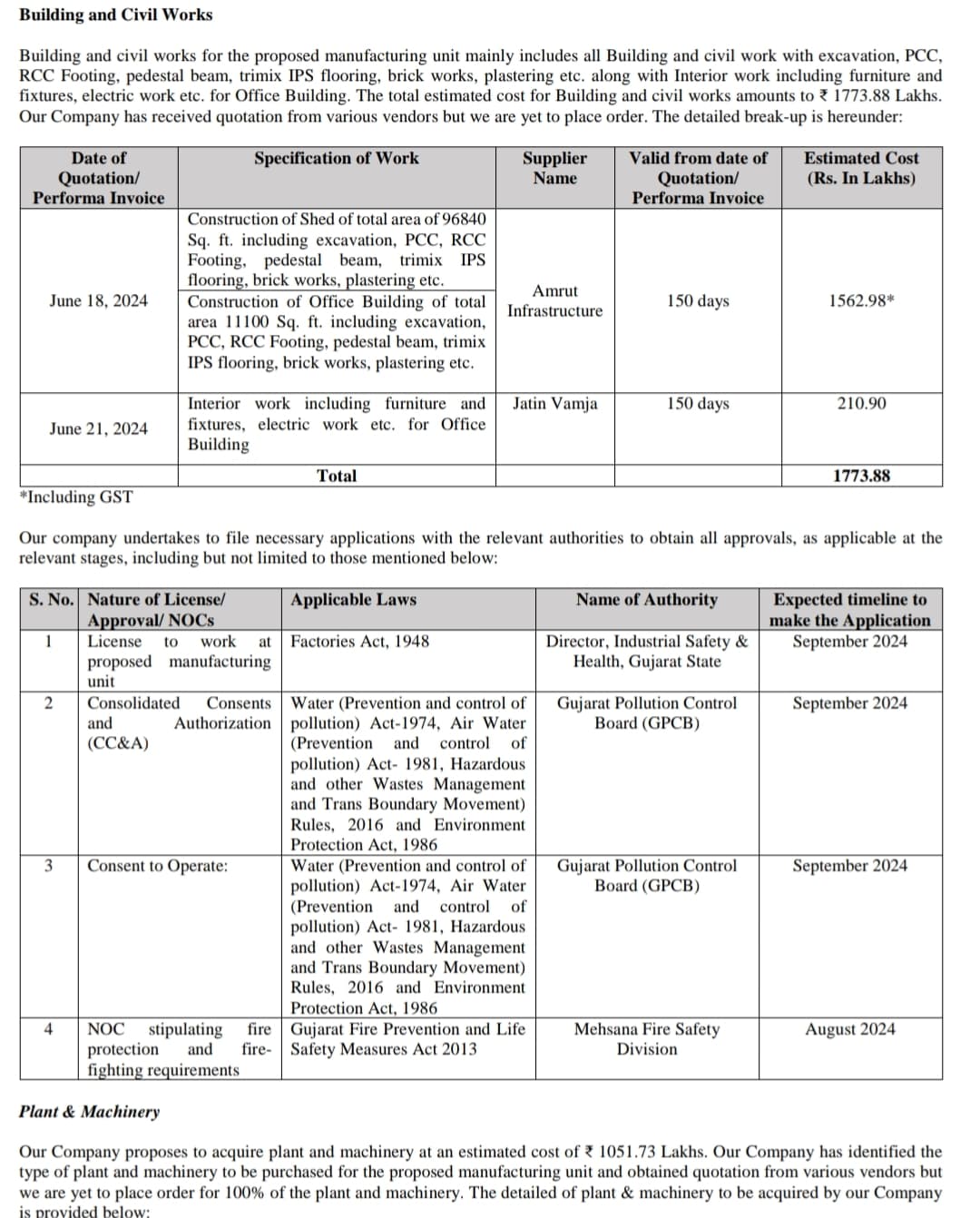

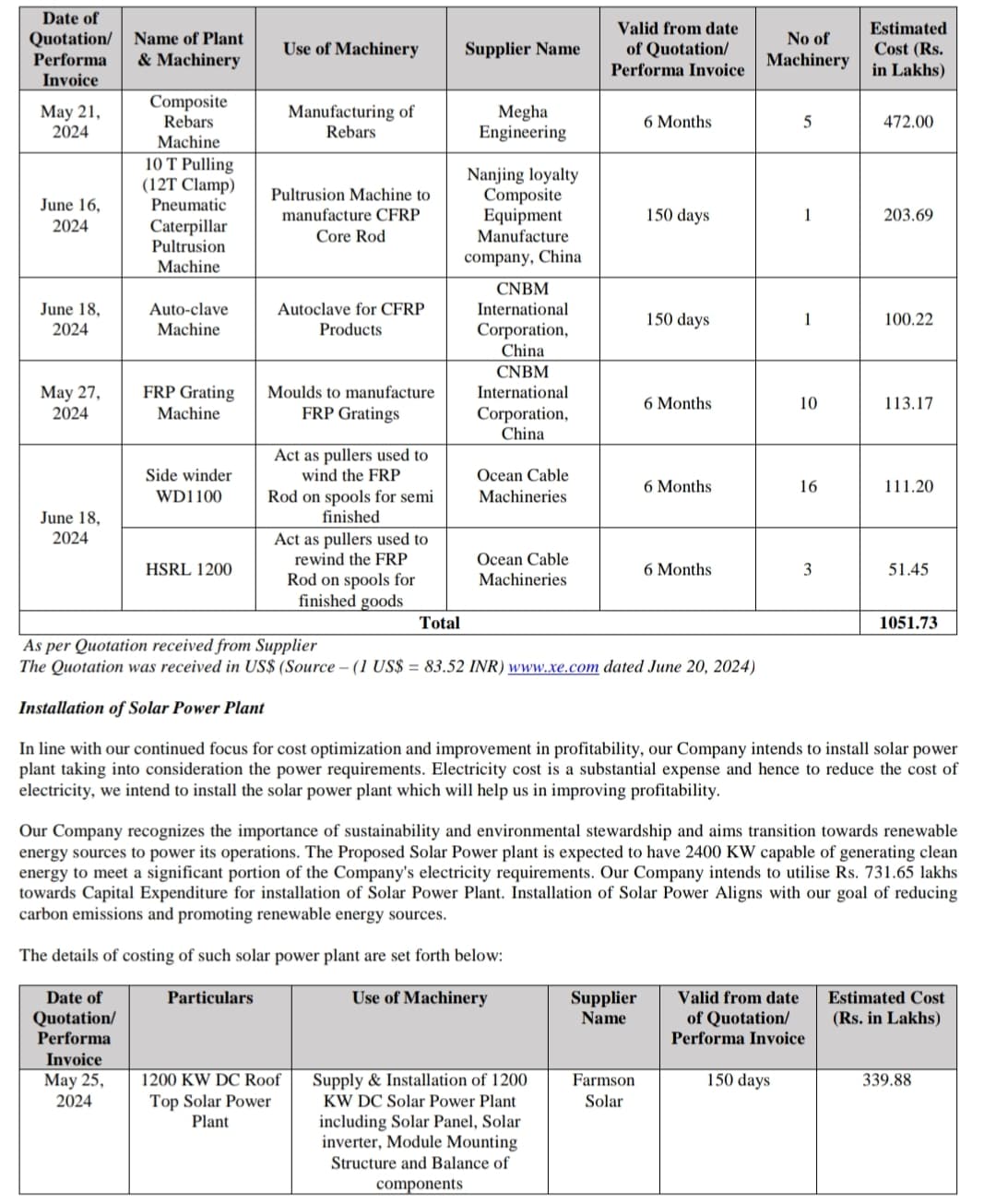

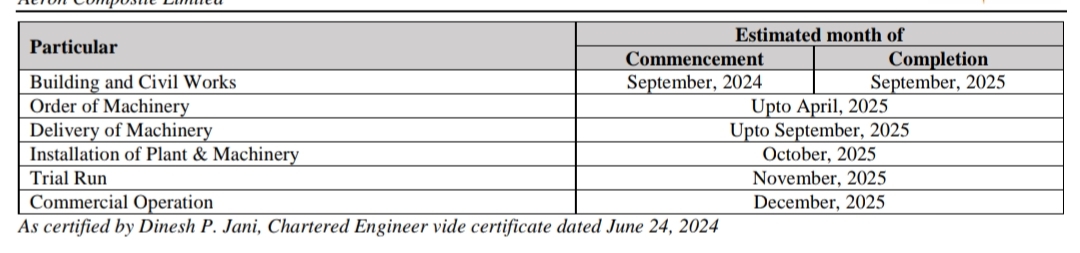

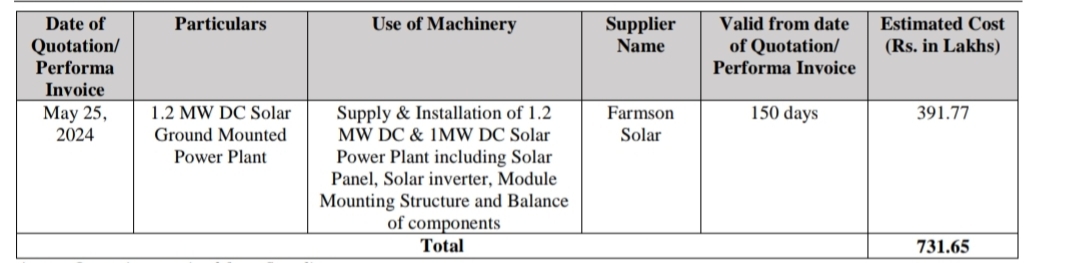

- Capital expenditure and potential revenue: if we remove installation of solar power plant cost , the company will still be doing 28cr worth of capex (building,plant and machinery), for comparison the company’s gross block as on FY24 was 29cr , according to the drhp they will complete the capex and start commencement by December 2025. This means if everything goes as planned the capacity will almost double within 1-1.5 years.

Risks:

-

Investment in microcaps/sme may lead to 100% loss of capital

-

Fluctuations in the price of raw materials like resins may impact the company’s gross margins.

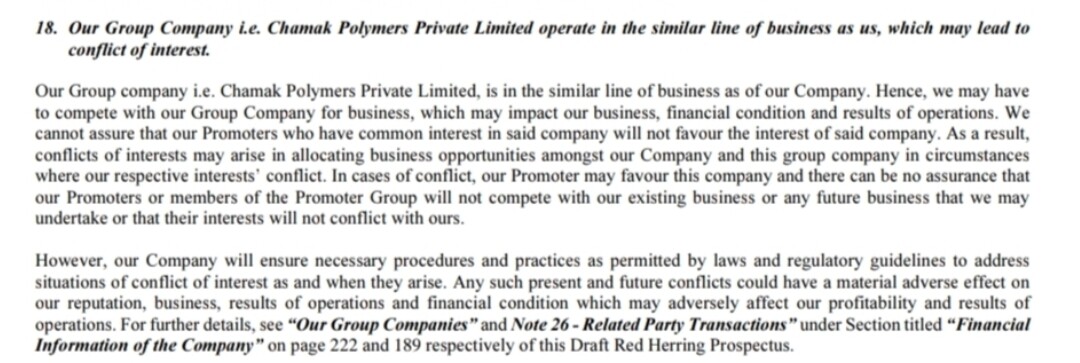

However chamak polymers has very less revenues compared to aeron composites and the total related party transactions with all the related parties for the year FY24 don’t exceed 15%( management salaries included in rpt)

Group-Company-Financial-Statistics_Chamak-Polymers-Private-Limited (1).pdf (142.4 KB)

-

Management salaries (total) were high in FY24 ~5.5cr. However it was a private company then and it has recently listed and became public, we must track their remuneration in FY25.

-

Execution risk, how they manage the capex and will they be able to complete the capex in time. They are Currently in the process of setting up a new

manufacturing unit in Mehsana district of Gujarat, measuring 51,671 sq. mtr,

which is owned by the company. Thier current operations are in ahemdabad, this shifting process may lead to some decline in production and revenues. However imo it won’t be a major impact since they will only shift their operations once everything is ready in place for execution

Disclosure:

Not registered, not a buy/sell recommendation.

Invested.

SYMPHONY – A Comfort to hold for Long term? (20-11-2024)

Symphony launches geysers, pretty nice ad as usual.

Symphony Spa – The Hairfall Control Geyser | Hindi TVC | 30s

SYMPHONY – A Comfort to hold for Long term? (20-11-2024)

Symphony launches geysers, pretty nice ad as usual.

Symphony Spa – The Hairfall Control Geyser | Hindi TVC | 30s

MOLD TEK PACKAGING—dividend plus growth (20-11-2024)

I have also taken a tracking position around 1 month earlier keeping the fact that Birla OPUS entering into paint segment. It is currently down around 10% from my buying price. I have an opinion that although sales are not growing and remains stagnant from last few years, but intrinsic value of company is increased due to capex in pharma packaging sector.

They are facing some challenges in supplying paint bucket to one of the Birla OPUS plant due to unavailability of IML printing machines, which is why they are supplying to Birla OPUS from their other plant.

Pharma packaging is a key sector to watch as it can command higher ebita/kg. Will continue to track results and concall to have pulse of the business.

MOLD TEK PACKAGING—dividend plus growth (20-11-2024)

I have also taken a tracking position around 1 month earlier keeping the fact that Birla OPUS entering into paint segment. It is currently down around 10% from my buying price. I have an opinion that although sales are not growing and remains stagnant from last few years, but intrinsic value of company is increased due to capex in pharma packaging sector.

They are facing some challenges in supplying paint bucket to one of the Birla OPUS plant due to unavailability of IML printing machines, which is why they are supplying to Birla OPUS from their other plant.

Pharma packaging is a key sector to watch as it can command higher ebita/kg. Will continue to track results and concall to have pulse of the business.