Exclusive | PB Fintech plans to enter healthcare sector with own hospital chain: Sources

Posts in category Value Pickr

Manappuram Finance (25-09-2024)

Seeing the current situation of Fusion microfinanace , I got little worried about MFI division (Asirvad) of Manappuram. I again read the concall and got this…

VP Nandkumar : “Then coming to our leverage, SROs guided us to ensure that our leverage is not promoted. They have said, yes, the maximum income per family to be kept at this thing and maximum lenders to be kept at this. And do you see that if you take our growth compared to some of the peers where the reports were already published, our growth was a little lower during the last quarter.

Whether it is micro finance, or MSME, these are especially people who are exclusive for that from top to bottom. Their underwriting requirement, these are all Secured loan, if you take the MSME, the average ticket size is around INR5 lakhs, INR6 lakhs. So these are used by small businesses – is around 7% only. That means 92%, 93% is collected by nearly presenting the NASH or check. The balance 7% we are collecting. *So around 5%, we have unsecured lending to MSMEs. These are all small ticket lending up to INR3 lakhs, INR4 lakhs. Now we have reduced that further. And we gradually we will reach 97%, 98%. So we have a team for each of these. Our business model is slightly different.

I think Manappuram is currently hold for me. I have already build up my position starting from 89 levels. Eagerly waiting to hear next concall and how it performs.

Strides Pharma/OneSource – The Last Stand Will Create Wealth? (25-09-2024)

Key points from the AGM held today

• gVascepa – There is ongoing class action lawsuit against the innovator on API cornering which is likely to take 3-6 months to conclude and is currently sub-judice. Will contribute to sales next year.

• US manufacturing operations have become profitable and contribute positively to EBITDA. Currently running at 60-65% capacity utilization; can extend the utilization through shifts and have a long runway.

• Teriparatide – Licensed to top 3 European companies and over 20 companies worldwide (not sell in US)– Received approval in Europe and UK, EM approvals expected soon. Expect it to be $7-8m EBITDA business.

• One source has 40 logos, 19 are GLPs. Make all 3 GLPs (Lira commercialize Q4 FY 25, Sema CY 26 end, Mounjaro FY 37)

• GLP capex c. Rs 800 crs – will increase GLP capacity by 4x – expected asset turn is 1.7-2x. Expected EBITDA margins to be 40%+.

• Semaglutide (unmet un-serviced market) is expected to be a blockbuster given innovators are focussed on US market (given the pricing advantage)

• Impact of biosecurity act – Interest in Bio CDMO has dramatically increased. RFPs now are 2x of earlier. We have already announced one contract earlier with a top 3 global animal health company.

Disclosure: Invested

TV Today- Value Migration (25-09-2024)

TV Today Network

M Cap – 1400 cr

Cash on books – 830 cr

Debt to equity – 0.04

Sluggish growth in sales and profits, but paying out consistent dividends.

Considering the valuations and nature of business can be a defensive play, promoters also not aggressive.

It can be a major candidate for any majors or acquisitions considering the strong brand reputation.

Tejas Networks – Product based IT business in a favored sector? (25-09-2024)

This is a very promising project with great future potential I guess, but has a lot of challenges from regulatory, infrastructure and technical limitations.

Great articles to read on the web (25-09-2024)

Lots of upside still left. What a bullish commentary but with valid reasoning. Enjoy.

Indian Markets Poised For A Surge? JP Morgan’s Rajiv Batra Decodes On The Talking Point

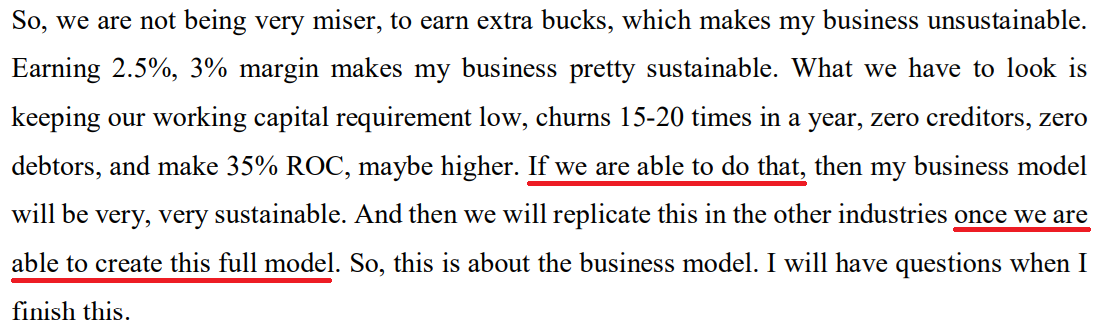

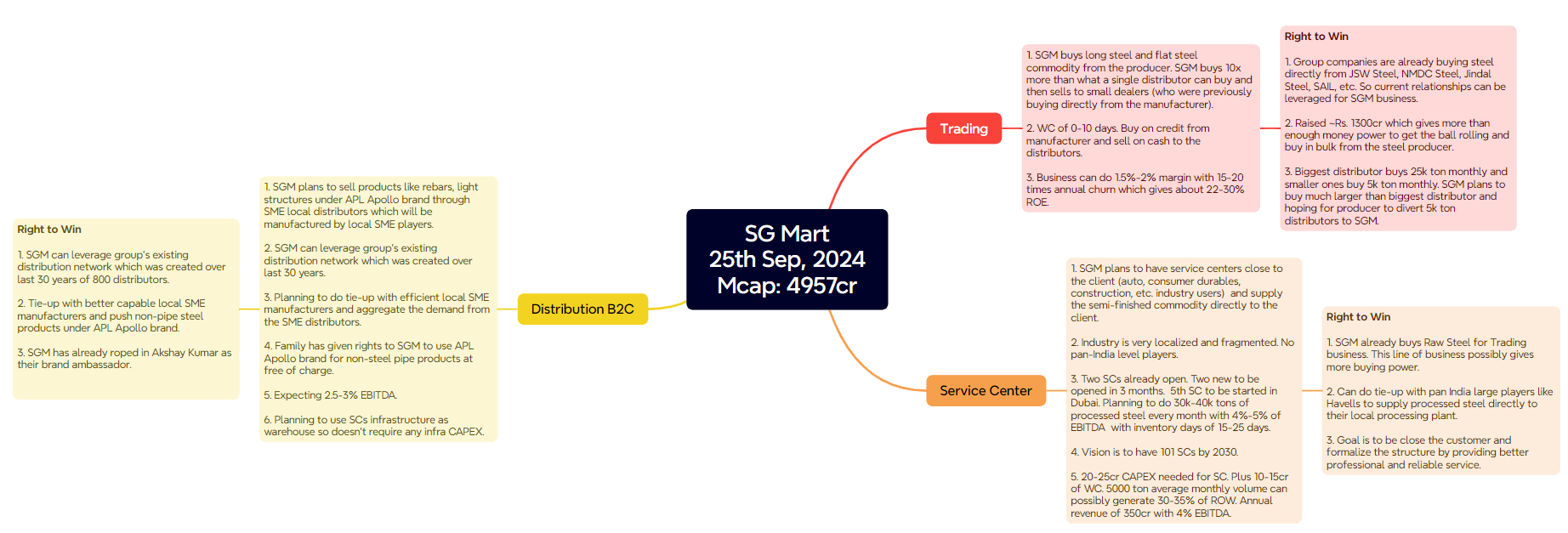

SG Mart- Can it successfully create a marketplace? (25-09-2024)

It’s a completely new business model which only time will tell, if the management is able to walk the talk. Although the management seems confident to fill the gap due to their decades of experience in the industry, but they are still being humble and confirming in the last con-call that this business model is yet to be proven (even after doing 85cr of EBITDA from just a 1-1.5 year old business). Below please see the humble lines underlined:

We all will have our opinions based on our past experience and mental models. I can see that the story of SG Mart can go either way as I can put up enough points supporting both bull and bear thesis. We are not helping this thread by simply sharing our one-line opinion without backing it with concrete facts and data. Story is currently half baked with lot to prove and huge execution risk ahead of it.

But I felt good after listening to the first concall and lean towards the bull camp to get my foot in the door. Current gaps that management shared on the concall seem to be big enough for a capable player to create a business and benefit out of it. Similar pitch has already gotten support from some of the respected investors and family offices (that doesn’t mean we don’t need to do our due diligence). While the company’s ambitious plans for a futuristic moat are intriguing, it remains to be seen whether decades of industry experience and Rs.1300cr kitty will yield a competitive advantage or simply become a costly folly.

I fully understand that we don’t need to have all the answers today (unless one is deploying 50% of their portfolio in SG Mart). Such stories with huge size of opportunity can have long run way of growth (many times very lumpy and bumpy along the way) and one can scale up along with the successful quarterly execution of the business and as confidence increases. In fact, I would feel much safer to average up at appropriate valuation in SG Mart 3 years down if they do Rs. 15000cr topline with 2.5-3% EBITDA.

Below I am sharing my understanding of each line of business and its “right to win” as shared by the management.

Disc: invested in last 7 days and managing execution risk with appropriate starting position size which will be kept on a very tight leash. Not a recommendation and do your own due diligence.

Shivalik Bimetal Controls Ltd (SBCL) (25-09-2024)

Was this a Hindrance in 22-23 for EV, Now back to Motivating levels for Govts ?

Or No One wants to Bet against China

Lt foods (daawat) (25-09-2024)

Dear Sidharth,

Interesting article on GI tag. Please go through!

India is facing increasing difficulties in securing Geographical Indication (GI) status for Basmati rice in the global market, which has an annual export value of about Rs 50,000 crores. Both India and Pakistan are staking claims over the GI of Basmati. Amid this dispute, New Zealand has rejected India’s trademark application for Basmati, following Australia’s earlier decision.

New Zealand’s stance is that other countries also cultivate fragrant rice, so no single country can exclusively claim it. The Intellectual Property Office of New Zealand (IPONZ) has refused to grant India a trademark certificate equivalent to a GI for Basmati. India’s Agricultural and Processed Food Products Export Development Authority (APEDA) had submitted the application on behalf of the country.

The dispute between India and Pakistan over Basmati has been ongoing for many years. In 2022, Pakistan applied for Basmati’s GI status in the European Union (EU). India, objecting to Pakistan’s application, demanded its cancellation. India’s own application for Basmati’s GI status has been pending with the EU since 2018. Pakistan claims it grows Basmati in 44 districts, including areas like Balochistan, where even normal rice is difficult to grow, and four districts in Pakistan-occupied Kashmir. Pakistan aims to increase its share in the global market for this premium rice by obtaining the GI status for Basmati.

To understand the global market issue of Basmati, we need to look back. In 2008, a group was formed in a joint meeting between India and Pakistan to address the GI status of Basmati. Joint secretary-level officials from both countries signed an agreement that recognized 14 districts in Pakistan and seven Indian states (Punjab, Haryana, Western Uttar Pradesh, Himachal Pradesh, Uttarakhand, Delhi, and Jammu & Kashmir) as Basmati production areas. It was decided that both countries would jointly apply for the GI tag for Basmati, but deteriorating relations shelved the matter.

In 2018, India applied to the EU for the GI tag for Basmati, but the EU put India’s application on hold. Pakistan applied in 2022, and the EU fast-tracked its application. According to the Geographical Indication (GI) application criteria, the product must be notified under a GI tag in its country of origin. India enacted a GI law in 1999, whereas Pakistan only did so in 2022, after which it granted the GI tag to Basmati and increased the number of Basmati-producing districts from 14 to 48, including four districts of Pakistan-occupied Kashmir. India was unaware of this until Pakistan’s EU application was made public for objections, revealing Pakistan’s strategy.

Upon learning this, the Indian government took swift action, and meetings were held between the Ministry of Commerce, Ministry of Agriculture, and scientists from the Indian Council of Agricultural Research (ICAR). Some officials suggested including new areas in India’s Basmati production area, but senior officials and agricultural scientists opposed this, stating that sticking to the already established areas based on specific geographical location, climate, and soil quality is in the best interest of India and its farmers.

At the Commerce Ministry, Ministry of External Affairs, and Prime Minister’s Office level, it was decided that India would oppose Pakistan’s Basmati application. The strategy is to initiate dialogue between the two countries after Pakistan’s application is rejected by the EU, adhering to the 2008 Joint Group agreement. Only 14 districts in Pakistan will be considered Basmati production areas, and India will produce Basmati in the fixed areas of the seven states.

Interestingly, three objections have been filed in the EU against Pakistan’s Basmati claim: by the Government of India, the Government of Nepal, and Madhya Pradesh. Many scientists and officials in India believe that Basmati production can be tripled within the already designated seven states, covering an additional 6 million hectares. For instance, Punjab currently grows Basmati in 600,000 hectares out of 3 million hectares of paddy, while Haryana’s 600,000 hectares can be doubled. Western Uttar Pradesh could also add 500,000 hectares.

A senior agricultural scientist emphasized that India should maximize its Basmati production within the designated states, as they meet the specific GI criteria. In contrast, Pakistan’s inclusion of new districts lacks legal and scientific basis. There is hope that India will successfully challenge Pakistan’s broad claim over Basmati.

Vijay Setia, former president of the All India Rice Exporters Association (AIREA), stated that the organization is opposing Pakistan’s claim and has presented its case through legal channels. While the EU’s decision is still pending, New Zealand’s recent rejection of India’s application has brought the issue back into the spotlight.

Moreover, Pakistan has captured much of the EU’s Basmati market due to its lower prices. India’s imposition of a minimum export price (MEP) on Basmati last year also negatively impacted exports. Most of India’s Basmati exports go to the UAE, Iran, and other Gulf countries. Therefore, securing the GI tag for Basmati is crucial for India, as it ensures better prices for millions of farmers in the seven Basmati-producing states due to the export market.

Amid dispute between India and Pakistan over Basmati GI tag, New Zealand rejects India’s application – Farmer News: Government Schemes for Farmers, Successful Farmer Stories)%20as%20Basmati%20production%20areas.