Management’s reply regarding this question in last concall

Management’s reply regarding this question in last concall

SG MART –

Q1 FY 25 concall and results highlights –

It’s an APL Apollo group company – started operations in June 24. APL Apollo group already runs 2 big companies – APL Apollo steel tubes and Apollo Pipes

In India ( before SG Mart ), there were no trading / distribution giants who could pick up material ( in big / bulk quantities ) from manufacturers and Distribute them across the country ( mostly to MSMEs + smaller Retailers / Distributors ) in the Steel + Other Building materials space. Existence of such nation wide distributors is a norm in US/EU/China. This was one obvious gap in the Industry that the company intends to fill

SG MART is a premier B2B one stop shop ( basically a B2B marketplace ) providing a wide range of construction related solutions from top brands ( like – APL Apollo, Premium Structural Sections, Jindal Steel, JSW Steel, Hindustan Zinc, SAIL, NMDC Steel, Kajaria Tiles, Havells Electricals etc ) under one roof

At present – company has 90+ registered suppliers of building materials and 800+ registered customers

Company’s current product portfolio includes – TMT bars, Wire Mesh, Binding Wire, HR Sheet, Checkered Sheets, Welding Rods, Tapping screws, Bath fittings, Tiles, Cement, Laminates, Paints

Q1 FY 25 financial outcomes –

Revenues – 1137 vs 151 cr

EBITDA – 24 vs 2 cr

PAT – 27 vs 1 cr

Cash on books @ 1125 cr

India’s steel manufacturing ( in various forms ) capacities are slated to go up by 50 pc by Dec 25 vs Dec 23. That’s a huge jump and is also a natural Industry tailwind for the company

Before SG Mart, the biggest distributor in India was selling aprox 25k Tons/month – that’s peanuts if u look at the current size of the Industry – ie 120 million tons / yr and likely to go upto 300 million tons by 2030

Company has already started doing a monthly volume a 60k tons – inside 1 yr of operations. Inventory days in this business are low at 0-10 days. Company makes a margin of 1.5-2 pc when it trades in these products. If it can turnover its inventory 20-25 times / yr, return on capital can be 30 – 40 pc !!!

There is another Industry Gap – there are various Industries like – automobile, consumer durable makers ( making Fridges, Washing Machines etc ) who don’t buy raw steel. They get their raw steel processed by small local players and then buy it from them. Here – the company intends to set up nation wide service centers to process steel to meet the demands of these user Industries and this will also give them much better margins vs pure trading. Company has already operationalised 2 of its service centers – processing 10-12k tons / month each. Aim to start 2 more service centers in Q2 this FY. Company will set up its 5th service center in Dubai. In this business, the margins are better @ 4-5 pc, but Inventory days are also higher @ 25-30 days

Company intends to set up > 100 service centers across India by 2030. Company Intends to cater to towns ( that have small Industrial hubs ) like – Patna, Ludhiana, Jalandhar, Jammu, Kochi, Raipur etc and sell the processed steel to the MSME buys in these cities

Cost of setting up + Working capital + Inventory requirement per service center should be around 40-50 cr. Company has the cash ( > 1000 cr ) and the RM ( since its already buying steel from the big players ) – this is their right to win in this space

By 2030, company intends to clock a topline of 50,000 cr with an EBITDA in the range of 1500 cr

For FY 25, company is looking to clock a revenue of 7-8k cr, doing 1.3 million tons of steel business with a blended margin of 2.5 pc ( EBITDA ). That should mean an EBITDA of around 170-190 cr for FY 25

Company aims to ramp up revenues to 13-14k cr in FY 26 and 18-19k cr by FY 27 ( basically – there should be clean runway of high growth looking into next 2-3 yrs !!! )

As the company is already into 5th month ( as on date of concall ) – they don’t see any risk on the horizon which may hinder them to achieve this yr’s guidance

Aprox Break up of Q1’s revenues –

Metals trading – 600 cr

Service centers business – 400 cr

Distribution of building materials – 140 cr

At present, company’s focus is largely on the steel segment. Once they achieve 500 cr EBITDA ( say by FY 27 ), they ll start diverting some energies towards other products as well. Company intends and is focussed to be the biggest tech enabled B2B platform in the steel segment in India

Some of India’s largest – region wise distributors have already become company’s clients

Company is light on debt and heavy on Equity funding. Also, their capital intensity is light – hence won’t ever have high depreciation rates. Most of the EBITDA is likely to flow to PBT level

Also, since company’s Inventory days are limited to 10-30 days, the Inventory risk that the company carries is also minimal

Even if one looks at EBITDA margisn of Shankara buildcon ( which has higher inventory days ) for last 20 Qtrs, they have been stable despite a lot of fluctuations in the Steel prices

Since Shankara is a big organised retailer, it can eventually end up being company’s customer. Company has already started started doing some amount of business with Shankara Buildcon

There are companies across the globe which have a very successful business and a model similar to SG Mart. These include – Sumitomo Trading company, Mitsubishi trading company, ITOCHU, HANWHA, MARUBENI etc

Disc: initiated a tracking position, business looks promising, growth guidance ( if achieved ) can create a lot of value, not SEBI registered, not a buy sell recommendation, biased

Does it make sense to enter at CMP?

With urban consumption continuing to rise and Rural consumption picking up, It is the 2 wheeler industry seems to be leading the charge.

Before we decide to put our money in the 2 wheeler industry, let us try to identify the likely winners. To do that we need to get some flavours from the past which has led to the present status and then predict the future trends.

350 CC Bullet was the first 2 wheeler Motor cycle to be made by Enfield india some times in 1955. (now owned by Eicher).Royal Enfield- an Iconic brand is a global leader in the mid-weight motorcycle segment

Marriages used to get postponed if Chetak was not made available for Dowry- Dahej. ![]()

In Moped 50 cc, Kinetics Luna had monopoly business during this period.

TVS came with TVS 50 Moped to compete with Luna.

Sooner , TVS had a collaboration with Suzuki to produce TVS suzuki Motorcycles and to compete with TVS Suzuki , Escorts -Yamah was born.

During 1985-86, two more innovative products were born from two different companies. Hero group in collaboration with Honda came out with a 4-S engine motorcycle CD100- first in India .with ” fill it, shut it and forget it” . 80 kms per litre…It became a big hit in Indian market and was appealing to the middle class bridegrooms.![]()

Piaggio came in collaboration with LML to produce the 1st scooter with engine at rear Vespa XP which also became a hit ( Bajaj scooter had engine in front with imbalance issue)

Sales of Chetak Scooter once a monopoly started dwindling and Bajaj was forced to close down its Chetak Scooter ICE plant in early 2000.

All these.players are still there , but with new Avatars with Motorcycles in entry level , mid weight level and premium level. Eicher bought over Enfield India and they seem to be happy with the premium segment Eicher has no entry level vehicle where the mass market lies. However to eat a Pie out of Premium bike Segment, Bajaj Auto has partnered with Triumph Motorcycles to create a range of premium motorcycles:

Bajaj Auto also has partnerships with KTM and Husqvarna to manufacture higher CC bikes, while Hero MotoCorp to manufacture the Harley Davidson X-440 …

By the time TVS , Bajaj , Hero realised the potential of EV, Ola Took advantage of Fame1/2 subsidy and soon became the market leader.

But it was not too late for the Trimurthy (Bajaj,TVS & Hero ) to snatch away 50% of the EV market share by sept 2024 from Ola.

These traditional ICE players had brand loyalty , strong after sales service set-ups built over last 45 years.

So whether Ola days are over.? only time could say that. But it would remain a big challenge for Ola to face the onslaught from Trimurthy !

Motorcycle EV cost is 2X-3X than EV scooters. 2 wheeler industry is cost sensitive…so all the 2 wheelers are now focussing on EV scooters.

Who will be the winners ?

Still traditional ICE enjoys monopoly, EV is penetrating fast …but not very fast …EV charging infra not there in rural India and customers would still prefer ICE due to simplicity , even cost.

So while Trimurthy focussed on EV, HMSI ( Hinda) focussed on ICE . Like Maruti , Honda played safe (Japanese are conservative) . They are here to make money.

They knew , it would take time for EV infra.

So who moved my cheese ? While Trimurthy fought together to snatch away 50% EV market share from Ola , Honda HMSI seems to have snatched away the ICE market share if we see the latest data. 1st link.

But Trimurthy with 45 years experience in 2 wheeler business will not let it go so easily though HMSI is a Very strong company to fight with.

Bajaj also has an export base, which TVS and Hero are trying to catch up.

Honda is Formidable. just launching its EV 2 wheelers with a 3-E concept. Exclusive Factory , Exclusive one EV platform in which various models can be built , EXclusive After sales service workshop. It is aiming at 1/3 of its production in EV by 2030.

please dony miss link no 4 if you want to know more about HMSI.

All the 2 wheeler listed stocks have run up TVS has become expensive, unless you have invested from lower level .The next expensive stock is Bajaj Auto and the last one is Hero motors in listed space at an affordable valuation. HMSI is not listed so also Suzuki motorcycles.

By now, if you have read the above article fully and the articles in the link below, you may be knowing where to make your investment decisions in 2 wheeler industry.

Risk Factors:

(1) Auto Industry is cyclical in nature. In a down turn , the sales may come down which may affect stock performance.

(2) Auto industry reports sales figures every month. Market may react to monthly sales figures leading to stock volatility.

(3) Consumer preference changes very fast and companies may lose market share.

(4) EV carries a lot of govt subsidy.If subsidy is withdrawn, it may affect EV sales

(5) New players may come in which would increase competition among existing players

Discl : i have invested in Bajaj Auto from lower level. no transaction during last 6 months. Have a small position in Hero.

I may be biased . it is not a buy sell recommendation.please do your own assessment before buy sell.

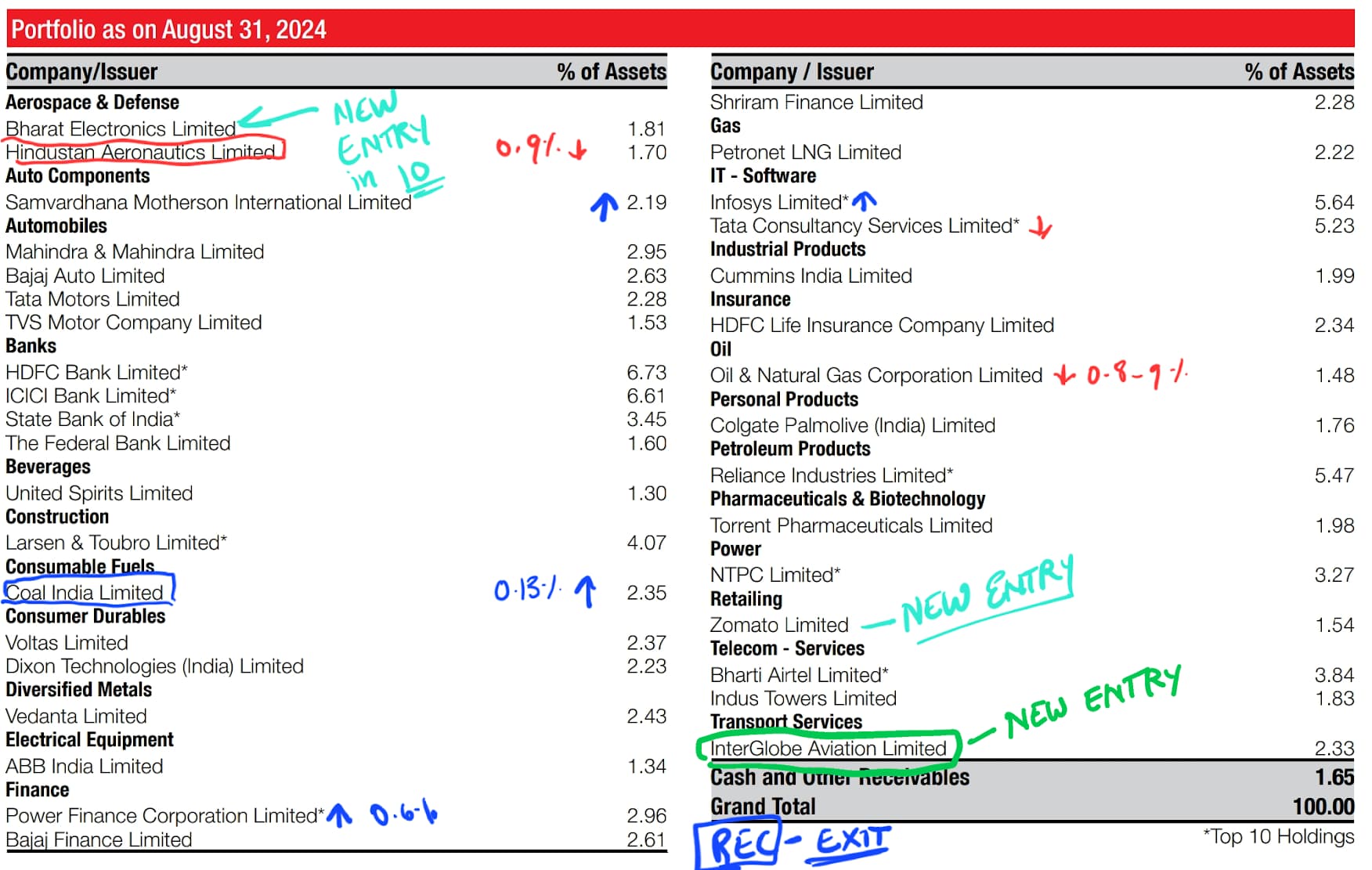

I have been tracking Nippon’s Quant Mutual fund since few months. I saw that in August Month, Indigo has come up as a new entry in Top Holdings of the Fund. It was missing in the July 31st disclosure. And this also very well corresponds to the jump in Indigo’s price from 4200 range to 4700-4800 range in past Month (due to big chunk of money coming at once). Ever since than, it is lying in this range more or less after climbing high for a day or two.

This shows that the fund is seeing opportunity in the stock for atleast 1 Quarter to 3 Quarters. Generally funds dont sell top Holdings after buying within a month or two.

Disclosure: This is my personal analysis. Remain well invested in the stock.

Assuming the drug is approved, What would be the incremental revenue for neuland labs?

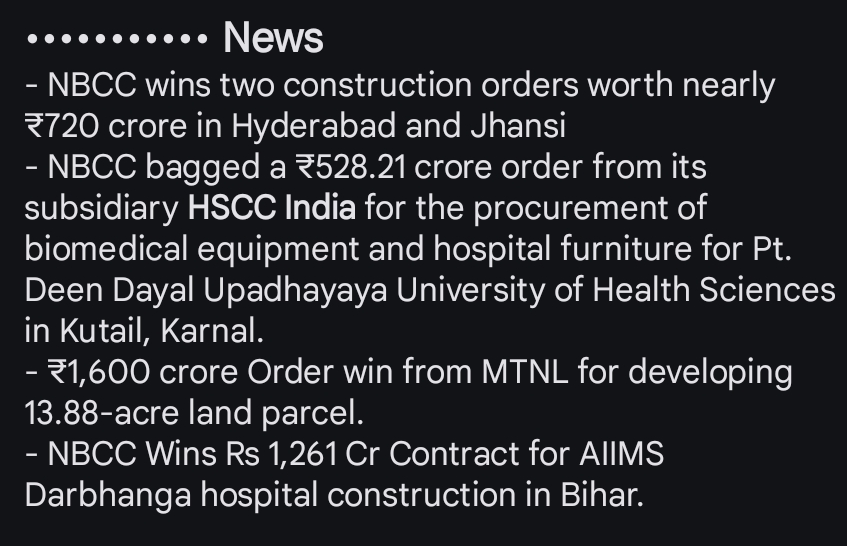

A collection of news of some recent wins since August this year

Any insights on capacity utilization in various sectors?

Bond values are indicated by 1. Issue price vs. Current price 2. Bond yield 3. Duration of the bond

Risks are more difficult to analyse, but things that help are:

I tend to use MF for bonds and direct for equity. This is particularly true if you investing for coupon payments…

Not sure, if it helps…