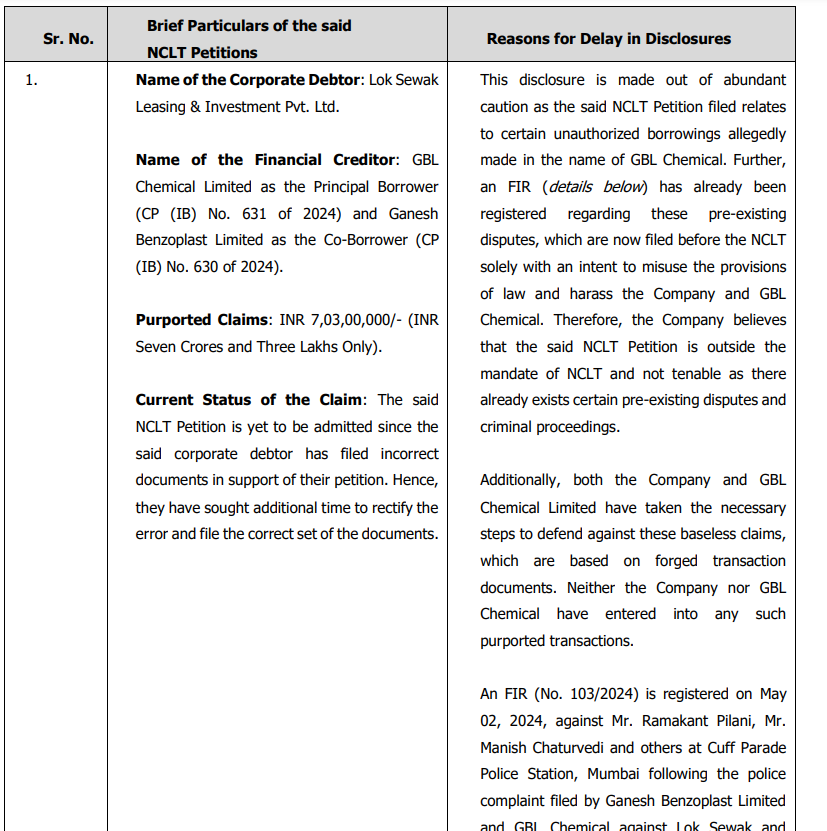

Major hit to the company- Creditors of the Chemical division have dragged the company into NCLT as a result of the recent fraud case~

Core operations should remain un-disrupted as a result of chemical segment being under a separate subsidiary.

Major hit to the company- Creditors of the Chemical division have dragged the company into NCLT as a result of the recent fraud case~

Core operations should remain un-disrupted as a result of chemical segment being under a separate subsidiary.

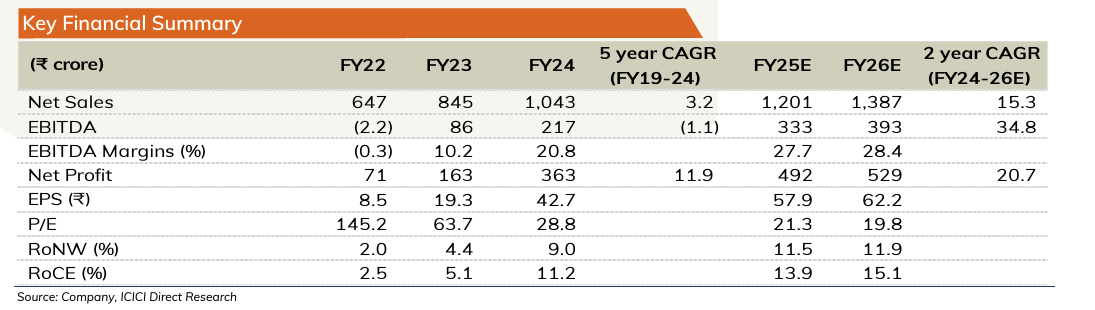

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.icicidirect.com/mailimages/IDirect_JustDial_CoUpdate_July2024.pdf

Trading at 20x FY25 and super cheap in the context of the current bull market

Do you guys know anything about recent selling?, is it because of this above disinvestment?

Thank you @Donald da for the writeup. This summarizes the major questions. The queries that I have are follows

I will update more questions as they come to my mind

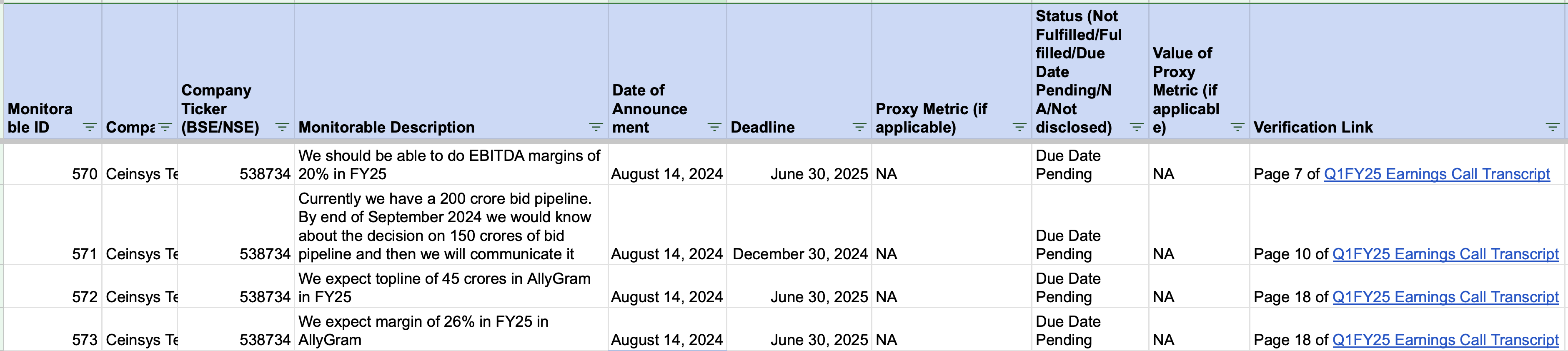

In the below tracker, I have started tracking important company goals for Ceinsys. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-4.xlsx (156.0 KB)

Similar high talking announcement like previous ones without specifics. Without value being called out or even an estimate provided, it is difficult to judge the runway for Sealmatic from this engagement. Hope to see some specifics released.

I think POPeyes has huge scope for growth

Answer is already in your question.

For rent a car , where we have to go? I will go to Ola or Uber because it is easy and convenient. Ola or Uber is a brand and we know it. Similarly, APL Apollo is a brand and SG Mart is going to do same thing like Ola or Uber in its field.

Steel service centre are like big retailer, they slit and supply as per customized requirement.

Highly unorganised industry with only local players i.e not even state level players. The bigger you are the better terms you get from manufacturer.

With a highly capitalized company with experience in steel there definitely is a case.

The growth in 1 yr is testament to their model.

can you please share the full report?