It was a hit piece that came out (market hours) on the same day of RBI announcement (during after market hours). Clearly someone’s toying with the media to crash the share price so they can buy it before RBI announcement and reap the benefits of the price bump. SEBI should probe.

Posts in category Value Pickr

Great articles to read on the web (21-09-2024)

Data Centres – Investment Theme by Vivek Bajaj.pdf (7.5 MB)

- Introduction to Data Centres

Data centres are specialized facilities housing IT and communication equipment such as servers, storage devices, and network routers. Their primary function is to offer secure environments for hosting data racks, with adequate power supply and cooling systems to prevent overheating.

- Types of Data Centres

- Captive: Owned and operated by companies for their private use.

- Colocation: Large facilities renting out space to third parties.

- Hyperscalers: Large-scale cloud service providers.

- Edge: Small-sized centres focusing on low-latency, last-mile data processing.

- Global and Indian Data Centre Market

The global data centre market is projected to grow at a CAGR of 10.5%, reaching a market size of $600 billion. India, although contributing 20% of global data, has only a 3% share in data centres, indicating massive growth potential. By 2030, India’s data consumption is expected to exceed that of developed markets, driven by increasing internet usage, 5G adoption, and IoT expansion. - Demand Drivers

- Rising digital technologies and data usage.

- Increasing demand for data storage and management.

- Growth of cloud computing, AI, and IoT.

- Low-cost data in India and the rise of mobile internet users.

- SWOT Analysis for Data Centres in India

- Strengths: Large consumer base, growing mobile internet penetration, increasing 5G rollout.

- Weaknesses: High energy consumption, lack of infrastructure in smaller cities.

- Opportunities: Urbanization, tech adoption, digital initiatives.

- Threats: Competition from global markets, regulatory challenges.

- Key Metrics

- Power Usage Effectiveness (PUE) is a key metric for data centre efficiency, with an ideal PUE of 1.0 indicating no energy waste. India’s average PUE has improved from 2.5 in 2007 to 1.55 in 2022, showing growing energy efficiency.

- Indian Data Centre Landscape

India has an operational capacity of 1,074 MW across 163 data centres as of March 2024, making it the 13th largest data centre market globally. Mumbai and Chennai lead the market due to their strong undersea cable ecosystems, accounting for nearly 60% of the country’s data centre activity. - Companies Involved in Data Centre Infrastructure and Development

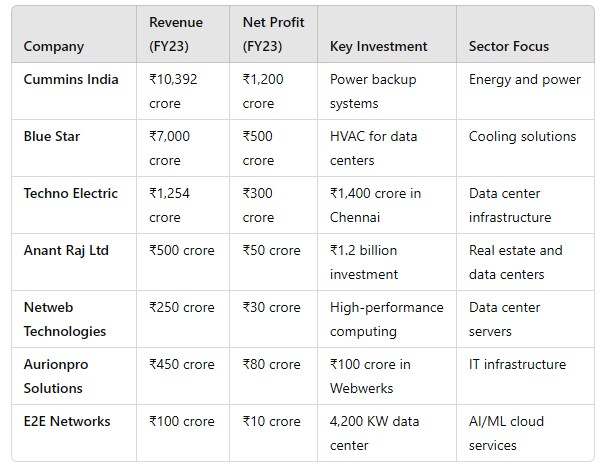

- Cummins India

Cummins is a global provider of backup power solutions, particularly for data centres. Its reliable diesel generators are essential for data centres to maintain uninterrupted power supply. Cummins India Ltd. is part of the Cummins Inc. Group USA. - Blue Star

Known for its heating, ventilation, and air conditioning (HVAC) solutions, Blue Star has already worked on projects like the Yotta Data Centre in Noida. The company provides turnkey solutions for mechanical, electrical, and plumbing systems and is the largest after-sales service provider for air conditioning and refrigeration products in India. - Anant Raj Ltd

Engaged in the development of IT parks and SEZs, Anant Raj is converting a commercial property with a potential leasable area of 5.66 million square feet into a 300 MW data centre. The company’s initial 3 MW of this project became operational in Manesar in FY23, with 50 MW more expected soon. - Techno Electric & Engineering Company Ltd (TEECL)

TEECL is developing hyper-density data centres, starting with a 24 MW IT load data centre in Chennai, scheduled to launch in Q3 FY25. The company plans additional centres in Kolkata, Mumbai, and Noida over the next five years. It is also working with RailTel Corporation to deploy edge data centres across 102 cities in India. - Netweb Technologies India (NTI)

NTI is a leading provider of high-end computing solutions. Known for its supercomputers, the company offers data centre servers, AI systems, and private cloud solutions. It caters to clients like IIT Jammu, IIT Kanpur, and Graviton Research Capital LLP. - Aurionpro Solutions Limited

Aurionpro partners with Webwerks to operate Tier 3 data centres in cities like Navi Mumbai, Hyderabad, and Bangalore. The company provides turnkey solutions for data centre design, consultancy, and master planning. It is also planning to develop 100 MW data centres in the coming years. - Black Box

An ICT solutions provider, Black Box offers system integration services in areas like data centres, cybersecurity, and digital solutions. In FY24, the company secured deals worth $105 million for data centre solutions and other significant contracts. - E2E Networks

E2E Networks focuses on AI-centric cloud infrastructure and is expanding its data centre capacity from 1000 KW to 4200 KW over the next seven years. This move will support AI/ML application development and deployment.

- Growth Drivers for Indian Data Centres

- Increasing internet penetration: India’s internet penetration is expected to grow from 50% to 90% by 2030.

- Mobile data consumption: Per capita data usage is projected to reach 62 GB per month by 2028, far surpassing current consumption rates in developed markets.

- Energy and Infrastructure Requirements

Data centres require robust energy supplies and infrastructure for cooling, IT equipment, and electrical management. As the demand for data increases, companies like Cummins, Blue Star, and Anant Raj are essential players in building the necessary infrastructure.

Conclusion

The data centre industry is a critical part of India’s growing digital economy. With increasing internet penetration, mobile data consumption, and the adoption of technologies like 5G, AI, and IoT, the demand for data storage and processing infrastructure will surge. Companies like Cummins, Blue Star, TEECL, and others are well-positioned to benefit from this boom by providing the necessary power, cooling, and computing infrastructure.

DDev Plastiks Industries – A Smallcap Gem (21-09-2024)

My two cents on consumer electrical industry as ddev in proxy player in this sector

India is the third largest producer and the second largest consumer of electricity in the world. contributing approximately 8% to the country’s manufacturing production, approximately 1.5% to India’s GDP and approximately 1.5% to India’s exports.

consumer electrical industry entails heavy electrical products such as W&C (A wire is a single conductor, whereas a cable is a group of conductors) and light electrical products such as FMEG.

The W&C and FMEGs were estimated at approximately 1.80 lakh crores in 2023 and it are expected to grow at a CAGR of approximately 10% till 2027 (Market value: 2,66,500)

In 2023, the total domestic market for W&C industry was estimated at approximately 75 thousand crores (41% of consumer electrical industry), It has grown at a CAGR of approximately 11% from 33,500 crore in 2015 to 75 thousand crore in FY2023 and is further expected to grow at a CAGR of approximately 13% till 2027 to reach a market value of 1,20,000 crore.

W&C market can be divided into 5 key sub-categories, namely housing wires, power cables, control and instrumentation cables, communication cables and flexible and specialty cables. Housing wires constitute approximately 32.8% (24,535 crore) of the wires and cables market in India.

There are six key factors supported by a positive macro environment that are expected to provide growth in the W&C and FMEG industry between 2022 and 2032:

- Public and private investment outlay in infrastructure

- Continued growth of residential real estate sector

- Resilient commercial real estate sector

- Transition of automobiles and transport towards electric vehicles (“EVs”)

- Rural electrification 6. Push towards renewable energy

The domestic W&C and FMEG industry is pivoting towards branded play. The share of branded play in domestic W&C and FMEG industry has grown from 60% in Fiscal 2015 to approximately 76% in Fiscal 2023 and is projected to reach approximately 82% by Fiscal 2027

Nearly 72% of the wires and cables market in India is controlled by branded play. Within this 72%, five leading players namely Polycab, KEI, Havells, RR Kabel and Finolex, garner approximately 60%–62% market share and the balance, 38%–40%, is controlled by challenger brands like Syska and V-Guard. Polycab is the market leader, having approximately 16% market share by value, followed by KEI (approximately 8% market share), Havells (approximately 8% market share), Finolex (approximately 6% market share) and RR Kabel (approximately 5% market share). RR Kabel is the fifth largest player in wires and cables market in India.

Simple Investing (21-09-2024)

Again to add, my post was not to say which strategy is better or superior. It was simply to appreciate our own style cutting all noise and thankful I could do that so far.

It’s like my chosen stocks follow different strategies instead of me and I give them that free hand to do that in cycles.

Mudit’s Portfolio (Stage Analysis + Price Momentum) (21-09-2024)

Hi Mudit, would really appreciate if you could share your tactics for position sizing in your momentum portfolio.

Simple Investing (21-09-2024)

This line summarizes it quite well.

Most of the new strategies fizzle out in deep market corrections, and then investors need to sometimes revert back to simple value investing which is the age old strategy and keeps working after every few years and also work across market cycles if the investor has patience!!

Simple Investing (21-09-2024)

To an extent maybe yes, but there are also set of excellent investors who are wired that ways irrespective of market conditions. These set of investors may be the ones who have practiced that strategy across market cycles and stuck to it as it’s the way who they are…

Rudra’s PF and Information attic (21-09-2024)

Hi,

The call-out was on the newly listed Northern Arc and not on Fusion Micro. Thanks for calling out the updates

RIL: Is the ‘Reliance” on ‘Jio’ Justified? (21-09-2024)

I am also holding Reliance for the same demerger play but What if Reliance instead of demerger like Jio Finance decides to do a separate listing for RR and Jio?

How will the existing share holders benefit via vi if it had been demerger.

- Has any time in past MA said that there will be demerger only for those two subsidiaries?

Mayank portfolio (21-09-2024)

Same reason here. I bought Anand Rathi at 1300 and sold at 2800. Put all that money in Nuvama at 3k levels. Rathi is v good but valuations are really stretched. One advantage of Rathi is their 0 debt. Really helps the valuation