Capacity Enhancement: The new facility is expected to commence commercial production within the current financial quarter.

Capacity Enhancement: The new facility is expected to commence commercial production within the current financial quarter.

Capex: Company has an approval of an additional ₹50 crore capex for new manufacturing lines at the Ratadiya, Mundra project.

Company announced a capital expenditure (capex) of ₹30 crore to expand the processing capacity of their plant in Gujarat by 50%.

@hitesh2710 Do you run or are aware of some amateur investors’ club in Vadodara? I too am from Vadodara and was looking for a community to discuss ideas and learn.

Company just won ₹246.78 crore order for 48 dump trucks!!

A big Positive for Cell manufacturers like Websol & Premier. A big Negative for Module only players and EPC players.

Recent Interview of HDFC Life MD & CEO with Money Control highlighted following points:

(1) Persistency in 13th and 61st Month is going up for HDFC Life which is a positive.

(2) ULIP now contributes about 36% which is slightly less than Q1 FY25 but it at elevated level due to Stock Market uptrend as compared to 5-6 years back when it was 25%.

(3) HDFC Life may not launch Health Insurance products even if those are allowed by IRDA. They will continue to increase their current Pie of products, both Par and Non-Par.

(4) HDFC Life has about 16% to 18% returns on their Embedded Value which is reasonable.

(5) Sometimes when Banking stocks do well, Life Insurance stocks do not do that well, since Markets perceive them as Long term stocks.

(6) Even if more FDI is allowed in Insurance Sector, actual investments may not go up as Economics are always not favorable for FDI. They will also look at other opportunities before investing more funds in India.

(7) Customers are slowly buying more Life Insurance policies compared to 2019.

(8) Product Factory and Innovation will be the focus of HDFC Life going forward as they always have launched New products in the past decade, and they would like to continue with Innovation.

Just thought of sharing with wider audience.

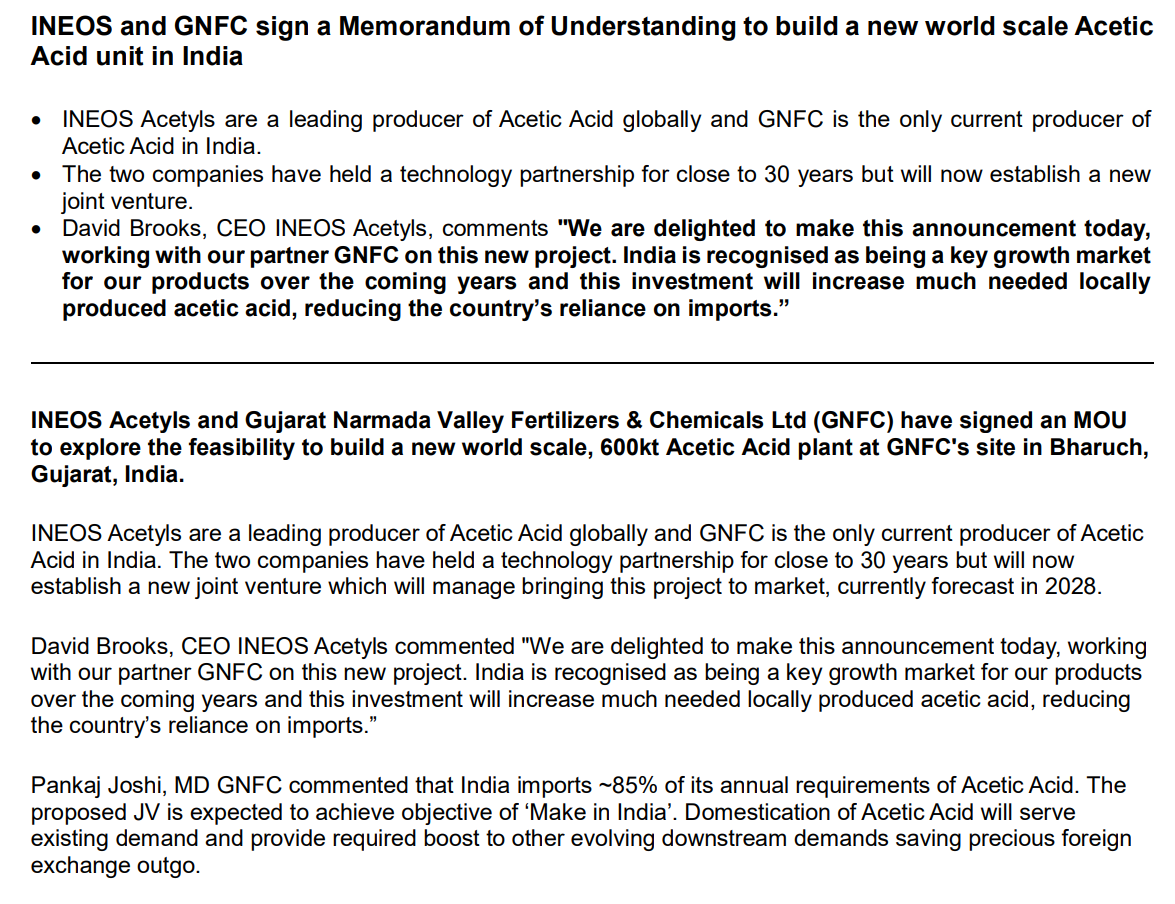

GNFC signs MoU with INEOS to form a JV and possibly build a 600kt acetic acid plant at Baruch by 2028.

KNR Constructions

Q2FY24

Elections issue with many EPC players in H1

Order book @ 4406 Crores

52% EPC, 23% irrigation, 25% pipeline

Within road projects other than HAM, 54% is contributed by state governments, 11% by the central government, and the remaining 2% by other entities.

Order book : 4406 Cr, doesn’t include 2 projects worth 1200Cr, H2 might be have better inflow : 6000-8000 Cr

Pipeline is good, 80-85 tenders from NHAI (800-1600 Cr)

Plans to bid MSRDC project in Maharashtra worth 2000Cr in partnership with other contractors.

The road sector is experiencing increasing momentum, with NHAI planning to award projects worth Rs 3 Lc Cr. Additionally, the Andhra Pradesh government aims to award irrigation projects worth Rs 1.5 Lc Cr, presenting significant opportunities for companies like KNR . The company’s strategy to diversify into other segments is a positive move for long-term growth.

Concall brief generated using NotebookLM:

Date: November 13, 2024

Attendees:

Main Themes:

Key Highlights and Facts:

Key Quotes:

Analyst Takeaways:

Disclaimer: This briefing document is based solely on the provided transcript of the Solex Energy Ltd. H1 FY25 Post Earnings Conference Call. Further research and due diligence are recommended before making any investment decisions.