South West Pinnacle Exploration

BSE CODE – 543986, NSE – SOUTHWEST

CMP – 115

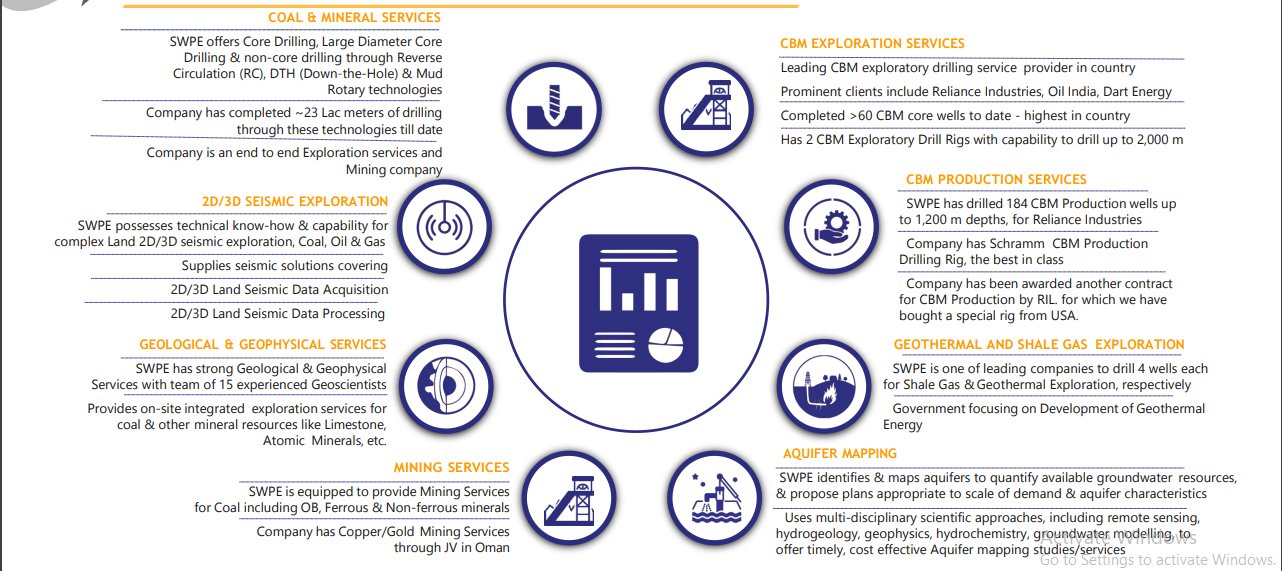

Company is present across various domains of drilling & exploration like Coal and Mineral drilling services, 2D/3D Seismic exploration, Aquifer Mapping etc. This segment is expected to grow at 15% with EBITDA margins in the range of 20-22%.

Some details about all the segments company is present into.

Company entered into a JV with renowned Australian exploration & mining company, Alara resources in 2018. Company was awarded $125 Mn. Copper mining Contract for 11 years in February 2022.

The company looking for their next phase of growth had bid for 3 coal block and amongst them won a coal block for commercial coal mining in the state of Jharkhand. The estimated Geo reserves of this block is 84MT. Company plans the start coal production by FY26-27 with a capex of 240 crs. According to the management the coal block alone could generate 700-800 crs. of revenue from Fy 27-29.

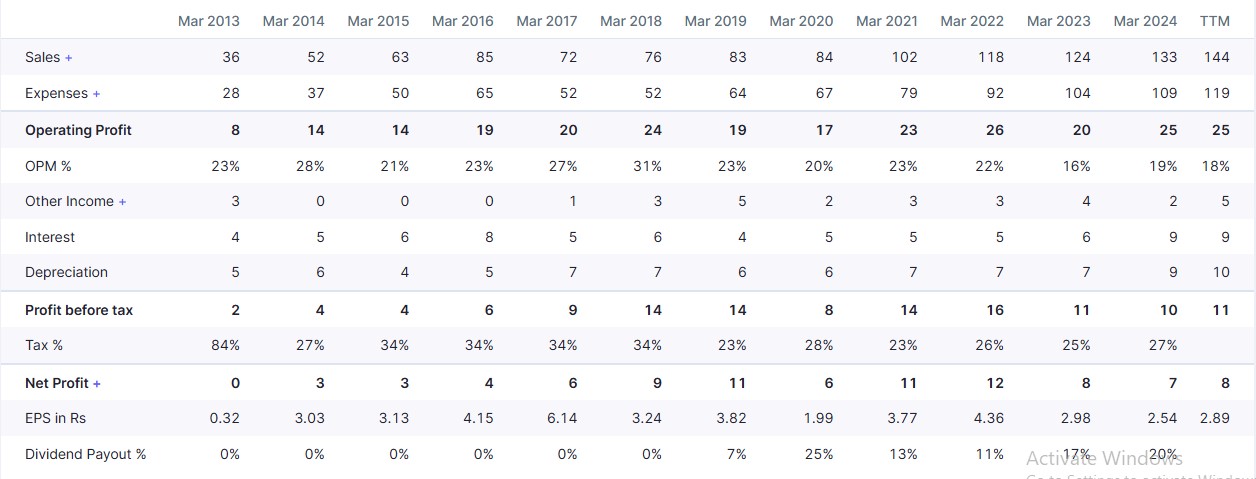

Company’s financials have been decent. They have some debt on the Balance Sheet but have been profitable mostly though profit margins are not stable.

Company has been generating healthy cash flows as well.

Risks –

The coal block alloted to the company is supposed to be at the place where they live. The management said that will help them as they know the area in and out. But coal is a risky business in India.

There is Govt. approvals required in every stage so this can be a hurdle as well. Many a times there have been huge delays because of approvals.

Disclosure – Holding the company so my views could be biased. I am not a SEBI registered analyst. Please consult your financial advisor before investing.