Please show the data to confirm this thesis. From what i have seen angel has been outgrowing all large competitors like zerodha, icici, hdfc, axis, upstox

Posts in category Value Pickr

Ksolves – a newage software development firm (10-09-2022)

Valuations have run up although mgmt is only expecting linear growth here on. Company seems to have taken some additional office premises on lease that may impact margins in the coming quarters.

Promoter shareholding seems to have changed to around 57.97% from 62.45% in last couple of months. Seems a steady decrease from 68.01% since June 2021 although does not appear to be a concern.

See the bright Sun: Aditya Vision (10-09-2022)

Answer is, every. Too many. Would urge you to study a random sample of all indian smallcaps. You’ll find 50% or more do the same. It’s a minor inconvenience as long as company can grow its revenue & margins. Some of largest wealth creators in last 6-12 month have been Mirza & meghmani which both had rpt concerns. In longer time frame: apl apollo, relaxo, poly medicure. Rpt is a minor nuisance unless the amount being talked about is copious (garware high tech films comes as an example here).

Opportunity in banking industary (10-09-2022)

Credit growth at 9 year high. Last year profit at all time high. This industry and the financial sector are at the begging of a multi year bull run. I feel the next 5 yrs are going to be the golden years for the Financial sector and especially banking industry.

I believe there are 3 banks which have the ability to outperform the banking industry in the next 4 to 5yrs. I would like to share the name of three of them and give a basic reasoning as to in which I have invested or not.

-

IDFC BANK - This bank has the brightest chances of outperforming but my reason to not invest here is it is a completely growth stock and epically in banking where the probability of a bad quarter is extremely high if investor see the next 2 quarters not as per expectation the volatility on these type of stocks can take the prices close to 50% down. Since I invest 40% to 70% in stock which I am confident I cannot invest in stocks which such high volatility.

-

FEDERAL BANK - This bank is a brilliant buy at 1PB and I have a view that the downside here is very low. The only problem they have is geographical risk. If you see they don’t have too many current accounts with them because kerela is an agriculture based economy and does not have big industries. For getting CA you need to have your branches PAN india. But technologically they are extremely good especially with their tie ups with neo bank. I have done a detailed analysis in this counter which I will post soon. You have to understand the middle east a little bit when analyzing this company because inward remittance is a big source of their money which comes form Keralite working in middle east. Just for add on info if you see the reason they go and work outside is because there is insufficient jobs in kerala for the skill set they bring.

-

YES BANK - Considering the growth which it can deliver in future the valuations of it currently make no sense to me. I share my view on this counter on its respective forum so wont be writing to much here. Currently this bank is close to 70% of my portfolio and I am pretty confident of it reaching a 1 lakh cr mcap by 2025.

There are 2 more stocks which I believe have the potential and I am analyzing them currently. INDUSIND BANK and BANDHAN BANK.

Overall I feel there are going to be heavy tail wind and I hope to make a lot of money out of them. I also hold 2% position on IDFC BANK of my entire portfolio and I am extremely interested to understand federal bank a bit deeper and take position here in future.

See the bright Sun: Aditya Vision (10-09-2022)

Can u ask them about this

Also their constant interest in buying and selling co shares?

Also do u own the stock now?

What is so great about cash and carry…infact its riskier if inventory remains in the stores due to low sales

See the bright Sun: Aditya Vision (10-09-2022)

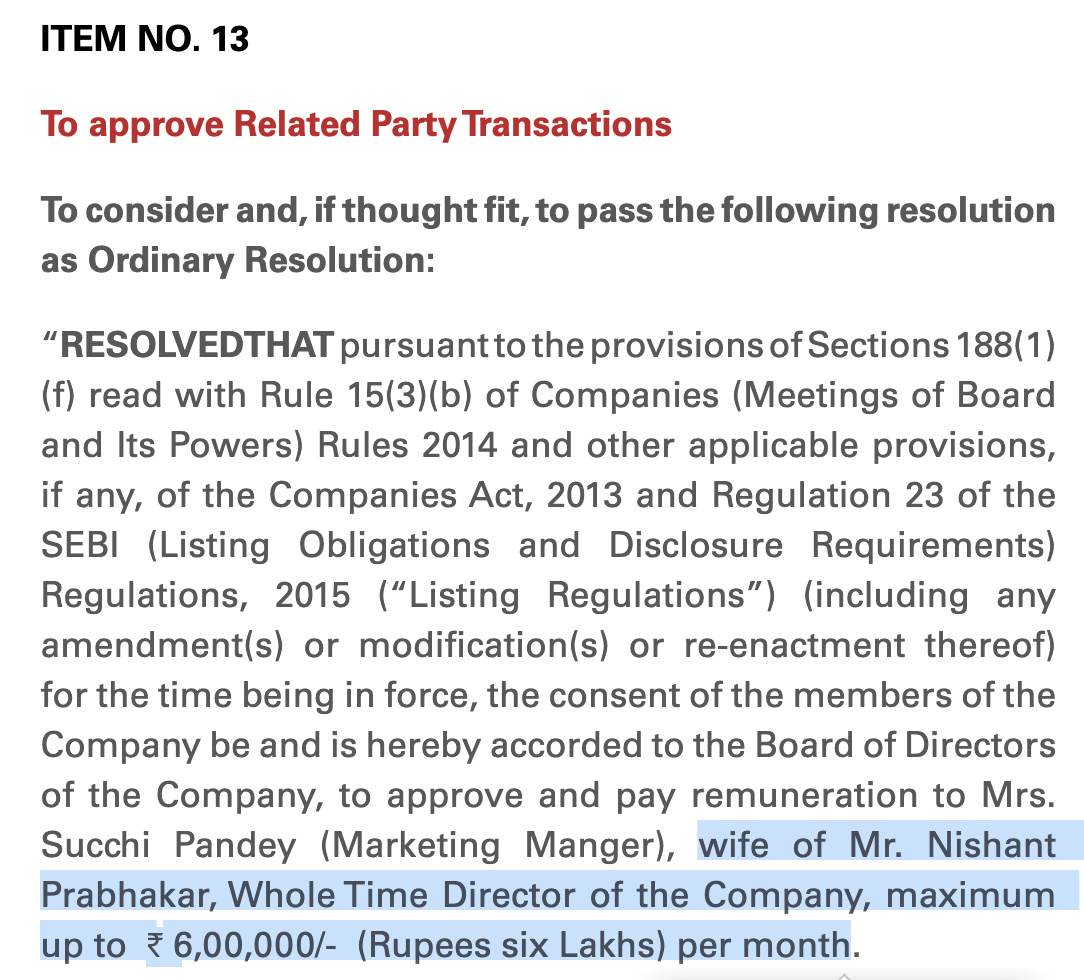

@sahil_vi Thanks for elaborating explanation and sharing notes of management discussion. This is really insightful. Credit to you, your post about the company made me to read about its business. While going through AR 22, found some RPT proposal to be approved in AGM. What is cause of concern here is many blood relatives are associated with the company and drawing hefty amount.

Well company at this stage, could it be justice to pay salary of 6 lakhs per month to a marketing manager. Would like to know you view on this(If you have any discussion with management on the same, pls do share)

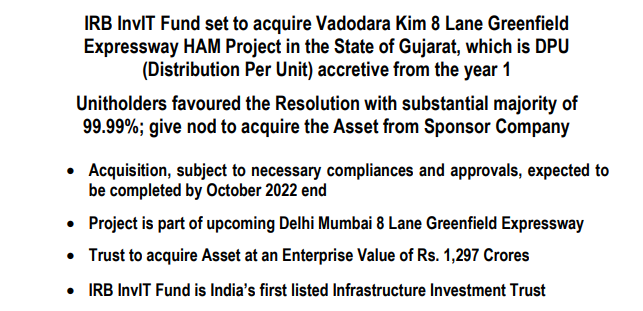

IRB INVIT TRUST- new game in the town! (10-09-2022)

My key takeway from yesterday EGM

- Management declaration of DPU accretive nature of new project indicates their intention for this asset and future asset additions

- Management if following more predictable/accurate timelines now as compared to last few years where they were giving vague answers in Concall

- Shareholder response to the resolution has been passed with great majority and same will push management to onboard more new assets in coming years

- Market Price differential from book value will merge soon and last few days price movement is quite indicative.

P.S: Invested and biased

See the bright Sun: Aditya Vision (10-09-2022)

As per the AR, they had 40 stores in FY 20, which increased to 78 in FY 22, so doubled, but revenue remained almost same ie around 800 crore levels. If one calculates, pre covid in FY 20 they were doing almost 20 cr per store sales, so with 90 stores already, they may hit 1800 cr sales run rate, even if they hit pre covid per store sales, AR says ssg is 15 %, that will be additional. This will be the first full year without any lockdowns for all new stores.

In H1 FY 23 they have already opened 10 stores, so assuming same rate may end FY 23 with 100 + stores, having a revenue rate of 2000 cr min, without considering ssg, which will be more than 2x of FY 22 sales of 890 cr.

If they continue to open 20/25 stores every year in MP, UP, Jharkhand in FY24 and 25, then having 150 stores in FY 25 is a reasonable expectation, so it is min 3000 cr sales rate, considering no ssg.

A lot depends on execution and consumer electronics demand also.

This is also a story of unorganized to organized retail and increasing penetration in under penetrated markets as per capita income increases.

ROCE is 78 %, ROE 51 %, ( asset light) so if the growth sustains market may give good valuation of 40-50 PE

Numbers estimate: Assuming no margin improvement, conservative estimate of 1500 cr sales in FY 23, they may do 70 to 80 cr PAT, FY 24 2300 cr sales, may do 135 cr PAT

So if they execute well on forward PE, this is less than 15 PE.

There is v little information available about this co apart from AR and screener, I hope management comes out with some investor ppt and do con calls to communicate better.

I think @ayushmit bhai also tracks this company closely and may wish to share his view

Disc : Invested and views are biased

See the bright Sun: Aditya Vision (10-09-2022)

For me the concern for investing in such stock:

-

Intense competition in the space, both from ecommerce as well as big retailers. Even if they are not present significantly today, it will see them in the near future. What makes Reliance, Croma or Vijay sales kind of people not to enter these cities when there is an opportunity for growth? I am sure they will be tracking AVL through their financial numbers. IMO, these big fellows would eventually eye Tier-2 & 3 cities when the growth is saturated in Tier 1. Then they can easily wipe out AVL.

-

As such business runs on low margin and further scope for reduction when the competition intensifies. So where is the room for improvement in margins?

-

Seasonality in the business.

-

Significant debt on the books. Debt for working capital, High inventories.

-

Promoter/promoter group/KMPs selling at higher levels from the open market. In Aug, 2022 itself, they sold 4.64 lakh shares.

PI Industries – Superior Business Model (10-09-2022)

You are right. Priyanka Chigurupati said this is completely untrue and baseless.