Highlights of the Concall by Capital Mkt

Total revenues fell 8% on a consolidated basis to Rs 372.4 crore for H1FY'16 compared to H1FY'15 while EBITDA before provision for exceptional item fell 14.4% to Rs 48 crore. The provision of Rs 6.29 crore has been made on account of bankruptcy of one of customers in UK. PBT was down 31.7% to Rs 31.2 crore while PAT was lower 34.7% to Rs 21.1 crore.

EBITDA margin for the quarter on a consolidated basis fell to 12.9% in H1FY'16 from 13.8% in H1FY'15. PAT.Standalone Income stood at Rs. 165.9 crore. EBITDA is Rs. 23.5 crore. EBITDA margin is 14.2%. Profit after Tax is Rs.12.66 crore for H1 FY16. Performance on standalone basis continues to be stable. The recent measures of Gol coupled with execution phase of India has begun which would lead to infrastructure creation and should improve performance of domestic steel producers

Monocon Group, UK subsidiary, reported Income of GBP 14.05mn for H1FY16. Profitability was impacted owing to one-time provision of GBP 0.64 mn in Q2FY16 on account of bankruptcy of UK based Sahaviriya Steel Industries, UK (SIS, UK), being British subsidiary of leading Thai Steel maker

Ei Ceramics, USA Business, reported Income of $ 7.67mn for H1FY16. EBIDTA came in at $0.61mnwith a margin of 8%. H1FY16 PAT was recorded at $ 0.25mn. . Lower domestic production of Steel in USA due to increased imports impacted the performance

Germany performance continues to have stable performance. Hoffman Ceramics, German Business, reported Income of Euro 5.35mn for H1FY16, EBIDTA came in at Euro 0.61mn with a margin of 11.47% an improvement of 91bps YoY.PAT was recorded at Euro 0.38mn with a margin of 7.18%

IFGL Exports, Indian subsidiary focusing on Exports market and operating in Kandla SEZ in Gujarat, reported Income of Rs. 23.30 crore for H1FY16. EBIDTA is Rs.6.1 crore with margin of 26%. PAT is Rs. 3.48 crore with margin of 14.95%. Favourable currencies led to better realisations. Phase 2 of expansion will now be completed in FY17.

Net Gearing stands reduced to 0.14x as on 30.09.2015 from 0.19x on 31st March 2015.

During quarter ended on September, 2015, Steelmakers continued to reel worldwide due to several macros likeslowdown in Chinese Economy, geopolitical conflicts, financial market turbulence, low investments, dumping of iron and steel by China. Global Steel production also fell by approx. 2.8% in H1FY16.Chinese Steel Exports increased by 28% in first 6 months of the year.

The World Steel Association has forecasted demand improvement in 2016. The company expects it to percolate down to its businesses, and expect better performance going forward, being directly related to iron and steel industry.

Domestic Steel makers in India are also under lot of stress. However few measures initiated by Central Government has given some respite to Indian steel makers- 1) To counter rising imports, 20% safeguard duty in September on steel imports from all countries to be valid for 200 days, 2) Import duty on base metals hiked, including iron and steel by 2.5% to counter cheap imports from China after Yuan devaluation and 3) Anti-dumping duty of up to USD 316 per tonne imposed on imports of certain steel products from three countries, including China.

Posts in category Value Pickr

Ifgl refractories ltd (17-11-2015)

Page industries (17-11-2015)

Royal Enfield  with a potential to sell all over the world, not just in India, Dubai & Sri lanka.

with a potential to sell all over the world, not just in India, Dubai & Sri lanka.

Re: Jammu & Kashmir Bank (17-11-2015)

Mushtaq Ahmad, CM & CEO addr the call.Highlights by Capital Mkt

For the quarter ended September 2015, the bank recorded a stagnant net interest income at Rs 694.47 crore as interest earned fell 4% to Rs 1721.33 crore and interest expenses fell 7% to Rs 1026.86 crore.Other income jumped 49% to Rs 126.51 crore after which net total income grew 6% to Rs 820.98 crore. As operating expenses grew 11% to Rs 383.27 crore, OP rose 1% to Rs 437.71 crore. Provision and contingencies fell 24% to Rs 126.58 crore. PBT grew 18% to Rs 311.13 crore. As taxation grew 25% to Rs 115.51 crore, PAT grew 14% to Rs 195.62 crore.

NIMs for the quarter ended Sep, 2015 at 4.02 % (annualized) vis-à-vis 4.01 % y-o-y.During the quarter, Post tax Return on Assets was 1.10 % (annualized) compared to 0.96 % y-o-y.During the quarter, post tax return on Average Net-Worth (annualized) stood at 12.29 % compared to 11.60%.During the quarter, cost of deposits (annualized) stood at 6.41% compared to 6.80%.

During the quarter, yield on advances (annualized) stood at 11.29 % as compared to 11.91 % for the quarter ended Sep, 2014For the six months ended September 2015, the bank recorded a 3% rise in net interest income at Rs 1389.31 crore as interest earned fell 3% to Rs 3474.05 crore and interest expenses fell 7% to Rs 2084.74 crore.

Other income jumped 22% to Rs 262.14 crore after which net total income grew 6% to Rs 1651.45 crore. Provision and contingencies fell 18% to Rs 339.45 crore. PBT grew 15% to Rs 556.57 crore. As taxation grew 24% to Rs 202.19 crore, PAT grew 10% to Rs 354.38 crore.

For the six months, NIMs stood at 3.97 % (annualized) vis-à-vis 3.83%.Post tax Return on Assets stood at 0.99 % (annualized) for the half year compared to 0.84%.Post Tax Return on Average Net-Worth (annualized) for the six months stood at 11.27% compared to 10.29%.For the six months, Cost of Deposits (annualized) stood at 6.40% compared to 6.84%.

Gross NPA stood Rs 3081.68 crore as on September 2015 against Rs 2186.94 crore as of September 2014 and Rs 2994.50 crore as of June 2015.In percentage terms, %GNPA stood at 6.48% as on September 2015 against 4.73% as of September 2014 and 6.63% as of June 2015.Net NPA stood at Rs 1269.69 crore as on September 2015 against Rs 1108.53 crore as of September 2014 and Rs 1276.76 crore as of June 2015.In percentage terms, %NNPA stood at 2.78% as on September 2015 against 2.46% as of September 2014 and 2.95% as of June 2015.

Other details:NPA Coverage Ratio as on Sep, 2015 at 61.92 % as compared to 54.85% a year ago.Cost to Income Ratio stood at 45.74 % for the half year ended Sep, 2015 as compared to 43.06%.Capital Adequacy Ratio (Basel III) stood at 12.76 % as on Sep, 2015 (RBI norm 9 %), which was recorded at 12.66 % as on Sep, 2014.In terms of RBI circular, the bank has, effective from quarter ended June 2015, included its deposits placed with NABARD, SIDBI and NHB on account of shortfall in lending to priority sector under "Other Assets" until now these were included under investments. Interest income on these deposits has been included under "Interest earned others". Until now such interest income was included under "Interest earned - income on investments".Interest on loans and advances fell 6% during the quarter to Rs 1259.48 crore.During the quarter, Other income jumped 49% to Rs 126.51 crore. Commission / Exchange, component of other income, grew 28%to Rs 49.00 crore. Insurance Commission grew 44% to Rs 9.17 crore, Treasury / Trading Income jumped 110% to Rs 38.83 crore and Miscellaneous Income grew 37% to Rs 29.51 crore.

Demand deposits fell 0.22% to Rs 5678.32 crore, savings deposits rose 10% to Rs 21306 crore and Term Deposits fell 7% to Rs 35457 crore.Restructured assets stood at Rs 2486.23 crore and there has not been any major change.Deposits in J&K State grew 9% to Rs 48053 crore, in Rest of India fell 24% to Rs 14389 crore and Whole Bank fell 1% to Rs 62442 crore.Gross advances in J&K State grew 14% to Rs 24545 crore, in Rest of India fell 6% to Rs 23428 crore and overall grew 3% to Rs 47973 crore.Gross advances to agriculture sector were 48%.Credit / Deposit (CD) Ratio (%) stood at 73.22% against 71.57% y-o-y.CASA Ratio (%) stood at 43.22% against 36.69% y-o-y.Branches – Excluding Extension Counters, Controlling Offices & RCC's stood at 829 against 802 y-o-y.Capital Adequacy Ratio (%) Basel II stood at 13.07% against 13.09%.Capital Adequacy Ratio (%) Basel III stood at 12.76% against 12.66%.The banks operating in J&K have extended credit of Rs 8080.21 crore to 214155 beneficiaries during the first six months of 2015-16 thereby registering an achievement of 34.23% of the Annual Credit Plan (ACP) target in financial terms.

J&K Bank alone has disbursed Rs 5337.53 crore to 116207 beneficiaries, which accounts for 66% of the total credit disbursed by all (46 banks and financial institutions operating in Jammu and Kashmir during the period.The bank has improved its performance somewhat when compared to the corresponding period of the last year and with growth forecasts brightening for the country's economy it expects a turnaround in the next 3 to 4 quarters.

In the floods aftermath and amid stagnation in the economy, the bank remained focused on balance-sheet cleansing and consolidation, improving the deposit mix besides provisioning enhancement. On all these counts it is moving ahead successfully.

The bank will continue to increase its market share in J&K through increased priority sector lending thereby giving boost to the agriculture and allied activities and craft economy.Increasing brick and mortar presence across the rural landscape of J&K shall remain at the heart of its focus.The bank also plans to increase its lending to tourism sector especially for infra-structural needs.Outside the state, the top rated businesses shall remain its preference within the niche lending markets.During the quarter there was slippage of Rs 202 crore.After the package given by PM Modi, next year is going to be very good.Non-J&K balance sheet grew by 15% the bank is focusing on GoI and top corporate houses.J&K balance sheet grew by 25%.

Page industries (17-11-2015)

A good latest report on Page by Motilal Oswal - "Getting into the big league" http://motilaloswal.com/Research-Research-actual.aspx?Search=14555

They label it is a long term compounder with 22% CAGR over next 8 years. I am pretty happy with that kind of returns for a core position in my portfolio. Of course if one thinks he can do better than that, then he should sell Page. Maybe at 16000 it was a partial sell, but not at current price. Any more dips will only make it more attractive.

Lot of FMCG names are at 40-50 PE with 15% kind of growth. So I dont see why Page should not get slightly more valuation for 20-25% kind of growth. Remember these business are valued highly because they offer long term secular predictability. How many brands have the "Aspirational but yet afforable" positioning?

Kaveri Seeds – Temporary thread for clarifications (17-11-2015)

without getting into detailed analysis, over a period of time the BT seed business will do well. genetically, BT seeds need to be replenished after every harvest & most importantly, they form a very small portion of the total cost of cultivation pushing cultivators towards better yield producing branded seeds. Dont let the recent gyrations in the price scare you. They are part and parcel of investing. It is a fantastic business.

Associated alcholols & breweries ltd (17-11-2015)

Hi Harshit,

Yes, the points you have highlighted are concerning and one needs to investigate more and have clarity.

@adrian007 - Like i mentioned in the first post itself that I was researching on the company and hence had some shares. In our personal style of investing - we often build positions while we are doing work and may increase or reduce exposure as per our further work. As a good practice, I just mentioned that I'm invested. However, somewhere it got mentioned that I'm endorsing the idea so I clarified that I'm not recommending the same.....its work in progress and just sharing the observations I have.

Regards,

Ayush

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (17-11-2015)

Thanks for your comments Nirav. I know that the lactulose facility is funded by debt. What I mean is that going forward, the cash flow from the lactose plant can be used to service this debt.

Lactulose in the formulation form is being made by almost every company under the sun. It is the bulk space where Lactose India competes and we need to determine if it really is niche and that is what we need to figure out. What makes it niche- is it access to process technology, raw material access or something else.

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (17-11-2015)

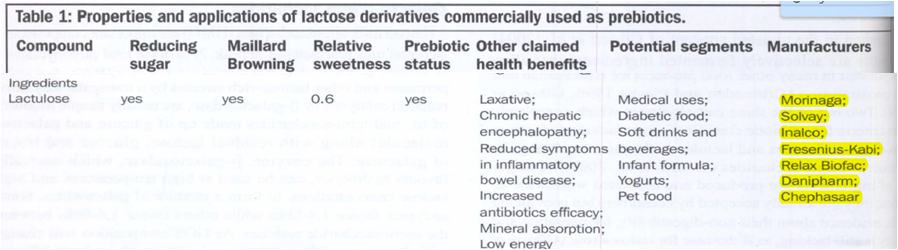

Lactulose market is indeed very interesting. Globally, as per some literature, there are 9 major producers and you are right Fresenius and Danipharm are 2 from that list and seems we are importing major qty from them.

If we search on alibaba there are many lactulose producers in china. But this is a milk derivative and as we know china is suspected of poor quality in diary products. So I think that could be part of the reason why China is not trusted for lactulose, while we probably import roughly 80% of other API's from them.

India is a mostly importing bulk lactulose (by tonnes), while exporting it form of small dosages like tablets and small bottles. Plus, lactulose has a wide non-pharma use, mostly as a food additive.

So, my guess is, mgmt. got this idea of getting into lactulose production based on their association with Kerry. Kerry after all is one of the world's largest food ingredient producer. I think the usage must be going up for lactulose as it's used for infant formula, pet food, yoghurt, beverages etc...which are mostly growing segments.

Searching for lactulose producers in India , leads to vague results, so am assuming there no producers currently and there is a strong case for import substitution.

It's been UC since the Q2 results were declared  , would have liked to add more below 60.

, would have liked to add more below 60.

Nirav already answered your questions on the usage of cash flow from lactose facility.

Disc: Invested before the Q1 results.

Lactose India – Unique Play on Lactulose & Contract Manufacturer for MNCs (17-11-2015)

Hi,

Couple of pointers...

1) Company isn't using cash flows from kerry (through lactose sale) for setting up Lactulose capacity. Numbers from Capex has just started flowing through and should keep improving sharply over couple of years.

2) Lactulose Capacity has been largely put up through debt (Long Term debt increased from Rs 4.7cr in FY13 to Rs 29cr in FY15.

I had attended the AGM (was among 3-4 shareholders who attended  )..What I could gather from Atul Maheshwari (MD)...Lactulose market is very exciting given application of the same and company has put up capacity after insistence from the clients. You are right sales from Lactulose will be around Rs 60cr. Demand it seems is largely tied up. I have no idea about whether Lactulose will be sold domestically or exported.

)..What I could gather from Atul Maheshwari (MD)...Lactulose market is very exciting given application of the same and company has put up capacity after insistence from the clients. You are right sales from Lactulose will be around Rs 60cr. Demand it seems is largely tied up. I have no idea about whether Lactulose will be sold domestically or exported.

Since company has expanded massively given its size, it would like to stabilize current capex initially. Management had indicated that Kerry has asked them to put up more lactose capacity. To get more idea about Lactulose beyond what capacity has already been put up, one should try meeting the management. What I could gather from secondary sources is Lactulose is niche market.

Hope this helps.

Thanks.

Disc - Invested.