Please share your number on private message so we can create a whatsapp group and as we grow we can have a meet-up together

Thank you

Please share your number on private message so we can create a whatsapp group and as we grow we can have a meet-up together

Thank you

A good comprehensive post indeed covering all aspects of the business of Indian Oil.

It is a undervalued stock and as of now the market is giving a low valuation for this stock mainly due to the risk as mentioned under your point no 9 – last point namely “Unwanted privatization can be a hindrance so is sovereign interference”.

The other risks as perceived by market is (a) volatility in crude oil price in international market which would affect its profitability as it imports crude. (b) Carbon intensive – any business involving carbon emission – market tends to give a low valuation (c) ,petrol-diesel being a source non-renewable energy and crude reserve are getting depleted day by day and by 2050 Oil reserve world over would get depleted. Mr market feels that Indian oil would be out of business.

However , market is yet to discount the fact that Indian oil and most other oil PSU in oil & gas space are actively participating in mitigating the risks a, b & c as mentioned above under Energy transition and Green fuel , sustainability,.

SME Holdings as on 13/09/2024:

| Stock | Cost % | Latest % | Avg Holding Period |

|---|---|---|---|

| Qualitek Labs | 10.53% | 15.77% | 58 |

| Holmarc | 15.08% | 14.76% | 198 |

| Trust Fintech | 12.06% | 12.84% | 43 |

| K2Infra | 14.35% | 9.04% | 9 |

| Aurangabad Distill | 6.04% | 8.56% | 351 |

| Chaman Metalics | 6.42% | 7.51% | 193 |

| Vision Infra | 10.02% | 7.36% | 1 |

| Delaplex | 10.27% | 6.42% | 12 |

| Knowledge Marine | 1.08% | 5.78% | 767 |

| Bondada Engineering | 8.32% | 5.61% | 15 |

| Kotyark Industries | 2.60% | 4.07% | 599 |

| Tanvi Foods | 3.22% | 2.29% | 1 |

The average holding period for Qualitek, Holmarc, Trust Fintech and Chaman Metallics is lower than actual due to tax harvesting. In all 4, I have entered on the day of listing and later on bought and sold.

Thesis for new additions:

Their Fixed assets have increased from 14 cr in FY 23 to 30 cr in FY 24 (majorly capitalized after RHP date, i.e. after Jan 24 and before Mar 24) and is further expected to be at 42 cr in FY 25 (30 cr + 7 cr WIP + 5 cr from IPO funds).

Once they achieve operational efficiency in their newly established labs, it will act as a significant boost in bottomline PAT, although it may take 12-18 months to achieve that.

Moreover, from IPO funds they are developing CBS and LOS software for North America and Latin America. This may or may not work but their domestic revenue is enough for them to sustain and any revenue from these markets will boost their top line.

Recently, the company has also won small order from Indian Bank. This is a one-time order but they have started tapping the PSBs.

Investor Presentation:

TRUST_13082024111802_NewIntimationtoNSEInvestorMeet130824.pdf (nseindia.com)

H2 Results:

Company heavily capitalized their employee expenses, resulting into decent Profit and Loss. Had it been not capitalized; the company would be at nil profits. Moreover, they will continue to capitalize it in H1 FY 25 also.

Peers:

They have considered NPST and Veefin as their peers, but Trust’s customers are completely different from NPST and Veefin and also Trust do not have heavy tech implementation comparatively and thus do not command the same valuations as its peers and might never will.

The valuations are overvalued, and the execution of the order book will dictate the valuations and price of the company.

The negatives here are high debt and the profit arising from sale of fixed assets. It constitutes more than half of its PAT which is very high considering the nature of the income being one-time.

Delaplex:

Good business at good valuations. I had purchased it earlier in June but sold it due to some cash crunch and re-entered at the same price a month later.

Tanvi Foods:

The company faces significant liquidity crunch.

They finally started production of the new manufacturing unit. The construction started at least 4 years prior.

The price has fallen quite a lot and valuations are completely off the mark.

The company also has significant inventory levels.

The production and sales from the new unit will command its future, else it is going towards mediocrity with the burden of fixed overheads from new plant.

New unit details:

3753d325-ac10-43a2-8406-bc5b90702aa9.pdf (bseindia.com)

Update on Bondada engineering:

I had sold the company in January with the reasoning of high valuations and it proved to be a big mistake. I have re-entered the stock, albeit at even higher valuations but they have started execution, and they routinely receive big orders.

Regarding previous high allocated holdings:

Omfurn:

I exited from Omfurn just before their FPO listing because of their poor subscription figures and high liquidity post FPO listing. I completely exited post H2 results.

PNGS Gargi:

Once the holding turned into long term, I exited due to continuous trading at expensive valuations. The exit was just before their preferential issue.

My portfolio under SME stocks is at around 60%.

Average Holding Period post tax harvesting is 188 days.

From the previous post, I have exited in many of them post their sub-par H2 FY 24 results.

Is this not just a transfer between two family members – as per later filings?

Disc: Invested – but evaluating a potential exit

Summary of The Almanack of Naval Ravikant

It can be downloaded free form: https://www.navalmanack.com

Naval Ravikant is an American entrepreneur, investor and philosopher. Some of his mental model is useful in investing, like…

Earn with your mind, not your time.

As you make money, you just want even more· You make money to solve your money and material problems. I think the best way to stay away from this constant love of money is to not upgrade your lifestyle as you make money.

The more desire I have for something to work out a certain way, the less likely I am to see the truth.

Any belief you took in a package (ex. Democrat, Catholic, American) is suspect and should be re-evaluated from base principles.

Almost all biases are time-saving heuristics (mind takes shortcut). For important decisions, discard memory and identity, and focus on the problem.

IF YOU CAN’T DECIDE, THE ANSWER IS NO.

The three big ones in life are wealth, health, and happiness.

We pursue them in that order, but their importance is reverse.

Set up systems, not goals

Courage isn’t charging into a machine gun nest. Courage is not caring what other people think.

Value your time. It is all you have. It’s more important than your money. It’s more important than your friends. It is more important than anything. Your time is all you have. Do not waste your time. Don’t spend your time making other people happy. Other people being happy is their problem.

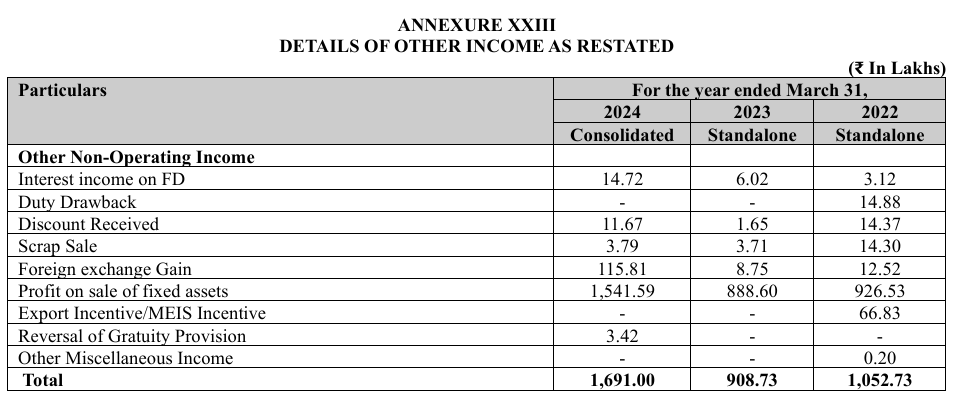

The total revenue of the company stands at 6660 Cr in FY 24 compared to 4960 Cr in FY 23 while the profit stands at 1304 Cr in 2024 compared to 544 Cr in 2023.

All these figures should be in Lakhs. 6660 Lakh revenue for the year ended 2024 and so on

How much are the returns for the stocks from October 18 until today? Were you able to track it somehow?

Can you share some of those methods? Thanks

When evaluating a company like Balu Forge, the numbers tell an interesting story — one that any investor with an eye on value should find intriguing. Over the last few years, this company has gone from strength to strength, growing its revenue from ₹142 crores in FY21 to ₹560 crores in FY24. That’s a CAGR you can be proud of, and one that doesn’t come by accident.

Now, there’s a simple truth in business: margins matter. Balu Forge’s Operating Profit Margin has climbed steadily, from 9% in FY21 to 23% in FY24. What this tells me is that the business isn’t just chasing growth for growth’s sake — it’s getting better at turning revenue into profit. The rising profitability signals that management has kept its eye on operational efficiency, even as the company scales up its operations. In the long run, profitability matters more than sheer revenue.

One of the golden rules I would like to emphasize is avoiding too much debt, and here, Balu Forge ticks the right boxes. With ₹49 crores in borrowings and a debt-to-equity ratio well within comfortable limits, the business is poised for growth without the heavy drag of debt payments pulling it back. This prudence gives Balu Forge flexibility to navigate any bumps in the road ahead.

And let’s not forget Return on Equity. At 26% to 31% over the past few years, this is the kind of number I look for when considering a long-term holding. It tells us that the business isn’t just growing, but it’s using shareholder capital wisely — generating excellent returns on every rupee retained.

But no company is without risks. For Balu Forge, the volatility in cash flows and working capital management raises a yellow flag, though I don’t believe it’s a deal breaker. The cash conversion cycle has improved, but like all investors, I prefer steady and predictable cash flows — it’s the cash that counts in the end. I’ll be keeping an eye on how this develops.

Now, as for their expansion into defense and aerospace, this is the kind of forward-looking move I admire. Balu Forge is positioning itself in industries where the future growth opportunities are vast. They aren’t just thinking about today, they’re building for tomorrow, and that’s a crucial part of the investment puzzle.

Lastly, the promoter shareholding has come down, which can cause some jitters in the market. But keep in mind, companies raise capital for a reason, and if that capital is used to fuel future growth, today’s dilution might well be tomorrow’s return on investment.

So, what’s the bottom line? For a long-term investor, Balu Forge represents a well-run business that’s growing its top line, improving its margins, and staying disciplined with its balance sheet. It’s not without its risks, but then again, no investment ever is. What I see here is a company that’s taking smart steps forward, and for those willing to buy and hold, I believe there are rewards ahead. Patience, as always, will be key.

Time is the friend of the wonderful company, and Balu Forge seems to be on its way to proving that it can be one.