Thanks Ashish and Venkatesh for the reply.

@Venkatesh, Could you please explain it bit more.

Also, does anyone has any comparative view of sales of products of insecticides vs other company products.

Thanks Ashish and Venkatesh for the reply.

@Venkatesh, Could you please explain it bit more.

Also, does anyone has any comparative view of sales of products of insecticides vs other company products.

Hi,

Apologies for the inconvenience caused because of website down.

There is issue going on with godaddy hosting . If they don't resolve in next 48 hours, I will start migrating to some other hosting provider.

Another decent quarter for company..

Though sales growth was missing, company did well to maintain the profitability momentum of previous quarter..

With half yearly EPS of 15 rupees & facilities back in compliance & 5 USFDA approvals in last three months which will eventually bring sales growth gives more power to its current rally.

At current price of Rs 400 & MCAP of 6400 Crores Jubilant looks undervalued.

A minimum PE of 20 ( though i believe even 25 is possible) with an expected yearly EPS of 30-32 gives a nice upside potential for 600-700 with limited downside..

Hi Sunil,

Your website seems to have gone viral, and rightly so. People on whatsapp and twitter complaining that your service is down and they are badly missing it.

Without this service, monitoring the results season has been tough going  You have solved a real need.

You have solved a real need.

I don't know if you have any product roadmap/plans of monetizing, but please bang the door/break the window to get the website working as soon as possible

Cheers

Kiran

Possibly. Their core product will still be RIVERA. What would you make of a company with one core offering and paying out all of its earnings(even more) as dividends? Doesnt this mean that the growth opportunities are limited?

Rakesh Jhunjhunwala is said to have placed a sizeable bid in the initial public offer of InterGlobe Aviation, the operator of no-frills airline Indigo, on Thursday.

Read more at:

Interglobe Aviation IPO scan by VS Fernando VS Fernando a veteran IPO analyst has come out with his view on Interglobe Aviation (Indigo) IPO. "Emptying the company’s coffers to fill the promoters’ kitty on the eve of IPO exposes the caliber of professional management", says the expert.

Read more at: http://www.moneycontrol.com/news/ipo-swot/interglobe-aviation-ipo-scan-by-vs-fernando_3789761.html?utm_source=ref_article

Consolidated Q2 2016 results:

Top line growth: 39%

Bottom line growth: 187%

India: Flat (Due to discontinuation of certain promotional schemes and hygiene initiatives)

US: 326%

Brazil: -18% (+19% on constant currency basis)

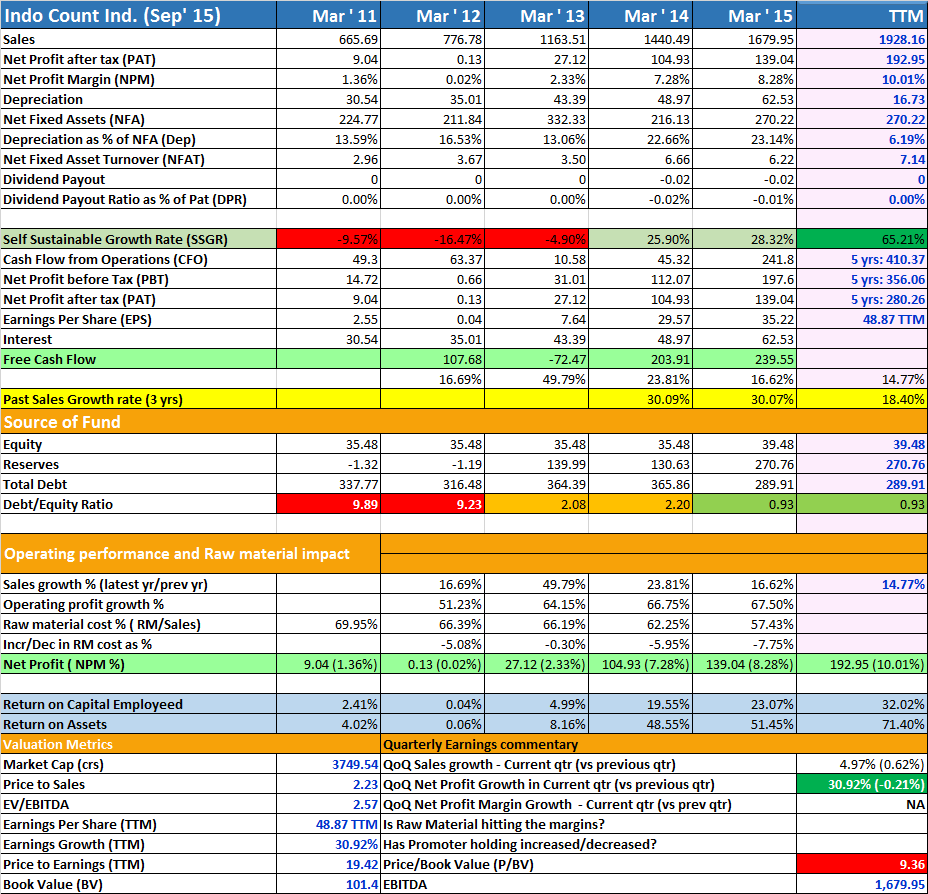

Good company with good growth rates. Good Self Sustainable Growth Rate. Debt reduced. Fantastic RoA and impressive RoCE.Valuation wise also at 2.23 levels is not horribly high. 9 times BV.

For Self Sustainable Growth Rate, pls read: http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

Note: FCF and EV values may be wrong as I have done it as per my understanding.

Promoters are above average on all three fronts of integrity,passion and competence,which one should look when evaluating a company or promoters. Retail side is going more towards mfs or pms in place of direct equity.Opportunity is big as this trend has just started.I am equally bullish.