Posts in category Value Pickr

Byke hospitality – Truly asset light? (04-09-2015)

Any insights on the rating suspension issue?

When a company hires a rating agency to issue a debt rating, they agree upon the facilities that the company wants to get rated and the time period for which the rating agency should monitor these ratings. Payment happens at the start of the rating activity and also in installments over the lifetime of the contract. When a company does not see value in getting the rating reviewed on a periodic basis, it gets the rating suspended to avoid paying the rating maintenance fees.

Its alright if the rating was suspended because of commercial reasons. Don't understand if it was the same in Byke's case. If not there could be some financial irregularities which the company did not want to disclose.

Disclosure: Haven't invested, awaiting more clarity on the rating suspension.

SRG Housing Finance – A fast growing NBFC (04-09-2015)

@madhug Allow me couple of more days to get back. Have been caught up with somethings at work.

Byke hospitality – Truly asset light? (04-09-2015)

where is target for 50000 rooms given and by when.

also having agent network of 220 plus across geographies will take time.

dont think make my trips of the world getting into this

Byke hospitality – Truly asset light? (04-09-2015)

Regarding the question of moat/entry barriers , Mr Anil patodia in his own words said room chartering business is scalable but has NO entry barriers .

Bykes business model has no comparable peers. But that doesn't translate to a moat/entry barrier. For that it must provide some form of differentiated service

• But bykes way of finding prospective properties for lease & run hotels through room chartering definitely gives it a edge over other budget hospitality chains.

• If byke achieves its target of 50,000 rooms for room chartering in 3 years,more importantly develop a working relation with hotel owners throughout the country plus cross selling of its own extended portfolio , byke may develop a 'network' effect .

Cupid Ltd – Helping the world play safe! (04-09-2015)

The Annual Report for 14-15 is out. The undertone is distinctly bullish. The CMD Mr. Garg worked all these years without any remuneration. Now that the Co. has started rewarding it's share holders, the mgt. has finally started on a remuneration of Rs. 3 lakh a month. A good example set for other promoters, but are they listening?!

http://www.bseindia.com/bseplus/AnnualReport/530843/5308430315.pdf

Hitesh portfolio (04-09-2015)

But Lincoln pharma ratios as ROE are very low. This should be problems with company or its management.

Towards a Capital Allocation Framework! (04-09-2015)

This is a good topic and the gist of the matter has been covered very well. However what I want to bring out is the question on how much of your networth to invest in equities? People talk about conentrated portfolio of well researched 2/3/4 stocks with strong conviction and understandig of the business. But what is the point if your equity portfolio is less than 10% of your networth? Personally based on my interaction with fellow investors equities are still a small pie of one's networth usually dominated by real estate and in some cases gold. I would like to hear and learn from investors who have more than 60% of their networth in equities and how they look at portfolio construction? Do they concentrate on a few names or diversify? What has been their experience over the past bull and bear markets?

Personally I hold a little over 30% of my networth in equities with a concentrated portfolio of 3 stocks making up 80% of it.

P.S: I have excluded the house I live, jewellery, car, etc.,while considering networth.

Hitesh portfolio (04-09-2015)

Dear @hitesh2710 : Do you track Lincoln Pharma?

Here are some quick notes:

Lincoln Pharma established in 1979 has its plant located in Ahmedabad.They are present in 51 countries (predominantly Africa, Central Americas & Central Asia) but not in regulated markets. 55% of their revenues come from International markets. Here is the break-up of their revenues from various segments:

General anti-infectives - 25%

Respiratory Systems - 20%

Alimentary Tract & Metabolism -20%

Genito Urinary + Sex hormones - 12%

Others- 33%(the break-up is available in Investor presentation)

This is a micro-cap with a mcap of about 200 crores. On a TTM basis the company is available at a P/E of ~11.88.(low P/E is due to lack-lustre sales growth i think for the past many years) The company's sales growth over the last many years has not been very impressive, but there are some recent positive developments.

Recent Developments:

1. Company has tripled its Unit 1's capacity.(has 2 units)

2. Acquires 36.58% stake from Lincoln parental - This is a key development as it offers Lincoln capability to develop complete range of product under therapeutic group like Tablet, Capsule, Ointment, Injectable, Syrup, Dry Powder under Lincoln Pharmaceuticals Ltd

3. Debt reduction

I have also attached their Q1 investor presentation for your reference. LPL-2015-16-Qtr.-1-Business-Presentation.pdf (1.2 MB)

Will the above developments mean a meaningful turnaround for Lincoln?

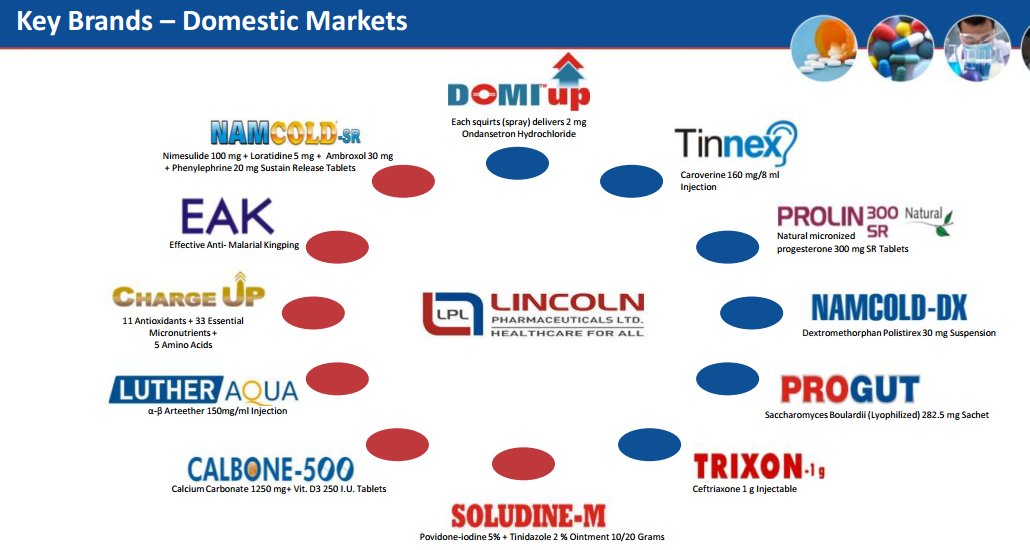

The below snapshot also has the list of their brands. Are these run-of-the-mill products which doesn't give this company an edge? (sourced from their investor presentation)

Thanks,

Ravi S

Disc - No positions in Lincoln

What you are buying in this major correction ? PF readjustment! (04-09-2015)

Great thread started. I have bought MT educare and dish tv in the correction. I feel these two companies do not have anything to do with the markets outside and fundamentally they are a domestic story...so i feel any correction in these two is worth taking a look at.