@ashwinidamani

could you provide examples of Valuepickr hidden gems which failed on Point 1 and Point 2? thanks

)

@ashwinidamani

could you provide examples of Valuepickr hidden gems which failed on Point 1 and Point 2? thanks

)

Excellent write up and I think you are right. but sometimes it becomes difficult to exit your winners but as you said one need to be rational then emotional and also it is very difficult to sit on cash ( atleast for me ).

The company has announced that they may consider a buyback.

Since the promoter holding is already 74.18%, how does the buyback work ?

Views requested

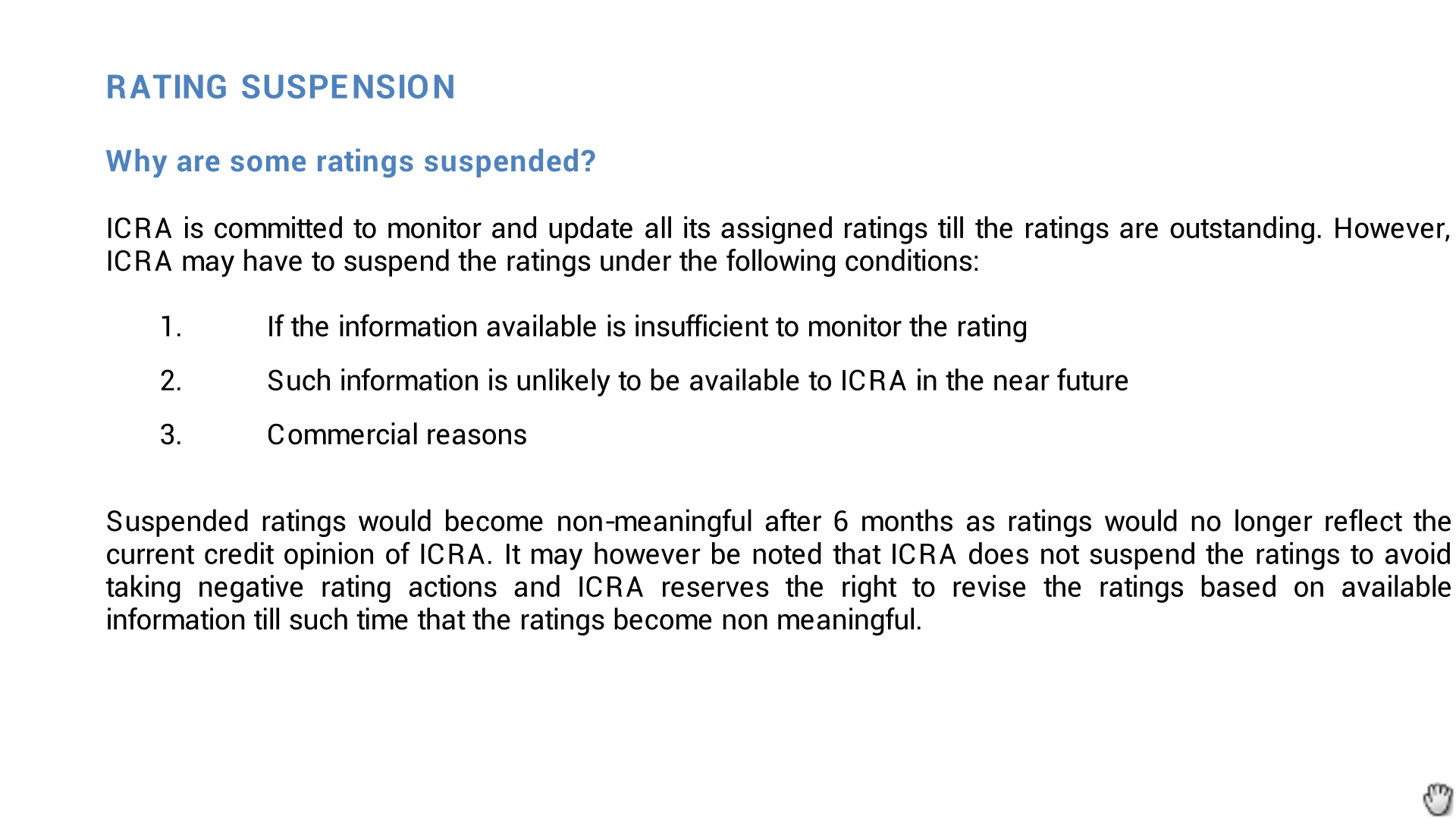

In bykes case the reason provided is insufficient information from the company.

One other case when suspensions happen are when the company decides to approach some other rating agency( discontinues existing one by not providing info).

Hope to get some clarification in the coming AR.

One need to keep in mind that Solar projects are very simple when it comes to implementation.

It involves just sourcing of panels and assembling it along with some minor civile work.

Would like to highlight that it has got No Entry Barriers

Reviewed the annual report of PI Industries….anyone interested in understanding the agri inputs sector should spend a couple of hours going through the MD&A in 2014 and 2015 PI Annual report

Agri Inputs

- Rice leadership is increasing for PI Industries. Nominee Gold expected to show continued growth for many years, and Osheen is well accepted to manage Brown Plant Hopper (BPH) in rice crop

- Two new agri input products – KEEFUN, an insecticide for vegetable segment initially launched on cabbage and okra (innovated in Japan, exclusive in-licensing agreement) and BUNKER, broad spectrum herbicide;

- KEEFUN will be extended to other crops and strengthen PI position in cotton and horticulture

- New pack of Biovita (specialty nutrition product) was launched, which was well received

- Key brands include NOMINEE GOLD, OSHEEN, KEEFUN, BIOVITA, KITAZIN, FORATOX, FOSMITE and ROKET

- Signed agreements to evaluate 10 new agri inputs for Indian markets

- Cautiously optimistic on agri inputs – dependant on monsoon pattern, performance of past product launches

Custom Synthesis

- 2 new molecules commercialized for CS exports (3 new molecules in FY14)

- Expect to commercialize 2 new molecules in FY16

- 8 new molecules progressed to the next stage of R&D

- R&D for Process improvements of 10 existing products undertaken to reduce cost

- Very bullish on CS potential and has a steady business with a large order book size

Other Key Points

- 170 crore investment in fixed assets, and R&D in FY15 (compared to 65 crore in FY14); Expected to invest 300 crores + in next 2 years on capex

- Jambusar SEZ facility is being enhanced with 2 new plants (CWIP shows 120 crore, compared to 35 crore in FY14), expected to get commissioned in H2 FY16 (Custom synthesis business)

- R&D facilities are being expanded - 2 story building is being constructed in Udaipur, which houses the current R&D facility

- Receivables increased significantly to 380 crore, vs 255 crore in FY14, resulting in Operating Cash flow coming down to 180 crore in FY15 from 216 crore in FY14; Doubtful receivables ~7 crore, which have been provisioned

- Due to the scheme of amalgamation of Parteek Finance with PI Industries, there has been no change in the paid up share capital and promoter holding remains the same as before the merger

- Internal auditor has been replaced to Grant Thornton from Protiviti

Absolutely! This is perhaps the best way to rebuild portfolio.

You can think of torrent pharma granules India cardila Healthcare ajanta pharma pi Industries.

When did VQ Moat Fund ever appear in the shareholding pattern filing to suggest that they have sold it off now? I searched since June 2014. Their name does not appear in any of them.

So their holding had always been something under the radar and never got published in official filings.

AGM Highlights uploaded by Avanti

Some extracts

PERFORMANCE OF FEED DIVISION:

First crop of Shrimp culture in current year is progressing well. There is healthy growth of 10-15%

because of increase in the area of culture, stocking density and continued conversions.PERFORMANCE OF SHRIMP PROCESSING & EXPORT DIVISION:

The division could not show much improvement in its performance during 2014-15 as the

exports to US in the 2nd half of the year were severely affected due to stringent checking of

each and every container of shrimp exported to that country for presence of antibiotic residues.

Because of this, there were inordinate delays in clearing of the consignments by USFDA with

additional expenditure to the exporters. As a result, exports to USA slowed down. Added to this,

as all of you know, the international prices of shrimps have been coming down almost

continuously.As an alternative, your Company developed new markets in Middle East, Europe and China

which enabled Company to maintain at the level of previous year's performance.

Current year, i.e. 2015-16 appears promising as the US Authorities reverted back to random

checking of the containers. Although the performance of this division in June’15 quarter is not

reflecting much of the positive development, in the coming quarter we believe, the exports will

gain momentum. The orders from new markets i.e. Middle East, Europe and China will also add

to the top line of this division and it is expected that this division will show improved performance

in the current year i.e. 2015-16.OUTLOOK

The future of this industry is attuned to grow at a steady pace of 10-15% and stay for a long time to come. USA continues to be a major export destinationfor Indian shrimps while new markets are being developed in Middle East, Europe and China.

Source http://www.avantifeeds.com/Notices/Chairman%20Address%20to%20Shareholders%20at%2022nd%20AGM.pdf