these patents are just glitter with nothing adding to the balance sheet in the immediate future. maybe in the future the company will be able to monetize these patents. active triggers are atleast 2 years away.

not invested

these patents are just glitter with nothing adding to the balance sheet in the immediate future. maybe in the future the company will be able to monetize these patents. active triggers are atleast 2 years away.

not invested

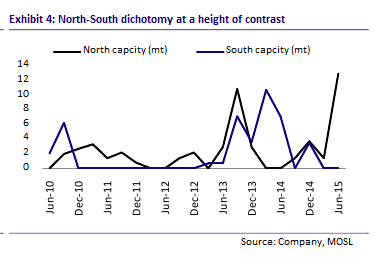

@madhug : adding some more to what Nikhil has explained. Low capacity addition was also due to the fact that B/S of most of these companies were affected in 2014 & 2015 and they were not able to add capacity meaningfully. Please check this exhibit below (Source: MOSL sector report)

Thanks,

Ravi S

Collective capex > more production > increased supply > (in case demand does not rise proportionately) price wars/ lower price realization due to demand-supply gap.

Please note, this may prove out to be a rumor but it seems more sensible path for cement companies in current economic conditions.

As a outsider to Cement Industry trying to comprehend what this means. Are you suggesting the industry works as a cartel? How does it matter for NCL who I understand from reading this thread sell through retail network and therefore there are no large/institutional buyers which is where cartels thrive?

NCL does look interesting. Not Invested.

New Target of 22,500 by Religare.

http://www.moneycontrol.com/mccode/news/article/article_pdf.php?autono=3005681&num=0

Sorry Ravi, can't help there since I'm from Maharashtra.

But it shall be easy to find out the prices. All one needs to do is visit a retail shop pretending to be a customer.

dinakaran,

As far as I recall PI Inds ROE have been in the range of 30%. Where did you get those figures? If they are from any sites like moneycontrol u need to verify again.

Best way of calculating these ratios is thru figures provided in Annual Reports or Statement of accounts provided in annual and six monthly results.

I am not able to post this in Kitex thread as it is undergoing maintenance. Kitex is indirectly involved in Panchayat politics and has supported formation of an independent party by name Twenty20. The panchayat elections are scheduled to be held in Nov 2015. The Kitex MD Sabu Jacob has nurtured this political independant outfit from grass root level by supporting them at various levels to raise their standard of living and from what I understand he has very good support from common man in that Panchayat. I think Sabu is taking a calculated risk here. None of the mainstream parties support him openly. They can't oppose him openly as the general public have recognized his contribution. If something goes wrong with the plant there, I am sure the political parties won't support him. Is there any other business doing similar work? As an Investor I am worried about the outcome. I will appreciate if anybody could share their thoughts on this.

Thanks @NikhilJain

Since you had mentioned that your father is in cement retail business, what are the current price trends? Are the prices stable/have they corrected? (in case you are from south)

I agree that this is an opportunistic bet as NCL looks mis-priced at current P/E and not a long term growth story.

Thanks,

Ravi S

hi

If u look at q1 results which had a lot of revenues coming from US, the following is the composition of revenues

US 46% 880 cr

India 25% 490 cr

Brazil 7% 134 cr

Eurpoe 12% 230 cr

ROW 5% 90 cr

Now coming to Brazil, how much the currency depreciates is to be monitored and then one has to think about what kind of problem torrent could have. Luckily for the company, this Brazilian thing comes at a time when US and Indian markets are firing on all cylinders for the co. And hence the actual impact shold be negligible. But if this problem continues beyond fy 16 then next year US may not be such a huge contributor to overall revenues and then the Brazil contribution could increase. But for that management has some time to react and take remedial action.

Another interesting aspect for this year is that

if u look at consolidated figures, PBT was 859 crores on which co paid a tax of 410 crores. (this is due to regulatory requirements bcos whatever is shipped (even though it is not recognised as revenues prior to actual sales) entails tax payment.) Management has categorically stated in concall that tax rate will be as per earlier year on an overall yearly basis. So till the company makes PBT of around 2050 for the year, it will need to pay a tax of 410 crores on ball park tax rates of 20% as per last year. Now co has alread paid the 410 crores and hence the incremental nearly 1200 crores of PBT will not attract much by way of tax and hence the figures for next few quarters could look much better than expected.

disc: invested.