57% stocks of Nifty 50 are in Stage 2 .

That does not mean that one can jump in each of these stocks .

This strategy is purely for fresh entries and exits (during corrections).

57% stocks of Nifty 50 are in Stage 2 .

That does not mean that one can jump in each of these stocks .

This strategy is purely for fresh entries and exits (during corrections).

AGM FY2022 NOTES:

Ajay Anand,MD :

Achieved growth of 50% in revenue and 100% in Pat

Major capacity expansion was undertaken , considering we would hit peak capacity by 2022.

Made significant addition to the Mgt Team across functions over last 18 months to get us ready for the next big run.

over 95% of business comes from existing customers across different product lines and regions.

Have added many new products and lines in FY22 which is very satisfying and shall reap good rewards in coming years.

Questions from Ayush Mittal

Q.Visibility to double revenue from FY22 BASE?

In last 4 years co. has doubled its revenue.

Similar trends of the last few years is expected going fwd in next 3-5yrs.

All the building blocks are in place.

95% business come from existing customers and these are large retailers and the scope to deliver to them is quite large.

Capex

100crs plan has been disclosed and 65% has been undertaken and balance will be undertaken in next 12 months . All this expansion is brownfield.

Once this capex is over we will be able to 3x of our revenue.

Since we are multi product, multi factory, multi raw material kind of set up so there is no standard measure of capacity.

We had similar situations 3 yrs ago when we said that with existing capacities we can double our revenues and we delivered on it.

China+1

Its a reality.

If we go by the standard vision statement of the largest retailer of US.

They intend to more than Triple their purchases from India.

To quantify the largest retailer has intend to buy $10bn from India by 2027 from current $3bn.

US Inflation

Jobs and wage market is very healthy right now.

We have gone through 3 recessions in 2001,2008 & 2020 also. our mgt has gone through those last 3 recessions.

But the HOME IMPROVEMENT segment or merchandise segment where we belong generally do not see steep decline as compared to home interior or housing sector.

US unemployment is all time now

Not seeing any major issue there.

As against very high growth we will see moderate growth in this year.

On cancellations of orders

We didn’t face any cancellation of orders due to made to order business model.

We might not see high growth as of last year which was around 50-55% but we will see moderate growth.

Margins improvement– Operating Leverage has played out in last 2 years

Better product mix

Going fwd we don’t see any reasons why we should not sustain and grow margins as soon as our capacity utilization improve.

Margins are not there bcoz of China+1 but bcoz of inherent advantages of our business model.

Customer addition– We are yet to start business with some of the large retailers of the world. There are almost 5-10 large retailers across US with whom we are yet to start business with.

AGM FY2022 NOTES:

Ajay Anand,MD :

Achieved growth of 50% in revenue and 100% in Pat

Major capacity expansion was undertaken , considering we would hit peak capacity by 2022.

Made significant addition to the Mgt Team across functions over last 18 months to get us ready for the next big run.

over 95% of business comes from existing customers across different product lines and regions.

Have added many new products and lines in FY22 which is very satisfying and shall reap good rewards in coming years.

Questions from Ayush Mittal

Q.Visibility to double revenue from FY22 BASE?

In last 4 years co. has doubled its revenue.

Similar trends of the last few years is expected going fwd in next 3-5yrs.

All the building blocks are in place.

95% business come from existing customers and these are large retailers and the scope to deliver to them is quite large.

Capex

100crs plan has been disclosed and 65% has been undertaken and balance will be undertaken in next 12 months . All this expansion is brownfield.

Once this capex is over we will be able to 3x of our revenue.

Since we are multi product, multi factory, multi raw material kind of set up so there is no standard measure of capacity.

We had similar situations 3 yrs ago when we said that with existing capacities we can double our revenues and we delivered on it.

China+1

Its a reality.

If we go by the standard vision statement of the largest retailer of US.

They intend to more than Triple their purchases from India.

To quantify the largest retailer has intend to buy $10bn from India by 2027 from current $3bn.

US Inflation

Jobs and wage market is very healthy right now.

We have gone through 3 recessions in 2001,2008 & 2020 also. our mgt has gone through those last 3 recessions.

But the HOME IMPROVEMENT segment or merchandise segment where we belong generally do not see steep decline as compared to home interior or housing sector.

US unemployment is all time now

Not seeing any major issue there.

As against very high growth we will see moderate growth in this year.

On cancellations of orders

We didn’t face any cancellation of orders due to made to order business model.

We might not see high growth as of last year which was around 50-55% but we will see moderate growth.

Margins improvement– Operating Leverage has played out in last 2 years

Better product mix

Going fwd we don’t see any reasons why we should not sustain and grow margins as soon as our capacity utilization improve.

Margins are not there bcoz of China+1 but bcoz of inherent advantages of our business model.

Customer addition– We are yet to start business with some of the large retailers of the world. There are almost 5-10 large retailers across US with whom we are yet to start business with.

Was reading the last con call and the management still keeps eluding about restructuring plan, mentioning that everything is in pipeline, hiring bankers, etc.

What I am concerned about is at what price / valuation would they be willing to sell the GCC business? How will the proceeds be distributed among shareholders? Or is this going to be retained by the company? Also, what is the need to sell GCC business? That was their cash cow. Can anyone clarify on this plz?

The market is not discounting this uncertainty. I am surprised by that.

Disc: Invested and planning exit strategy based on restructuring plan.

Was reading the last con call and the management still keeps eluding about restructuring plan, mentioning that everything is in pipeline, hiring bankers, etc.

What I am concerned about is at what price / valuation would they be willing to sell the GCC business? How will the proceeds be distributed among shareholders? Or is this going to be retained by the company? Also, what is the need to sell GCC business? That was their cash cow. Can anyone clarify on this plz?

The market is not discounting this uncertainty. I am surprised by that.

Disc: Invested and planning exit strategy based on restructuring plan.

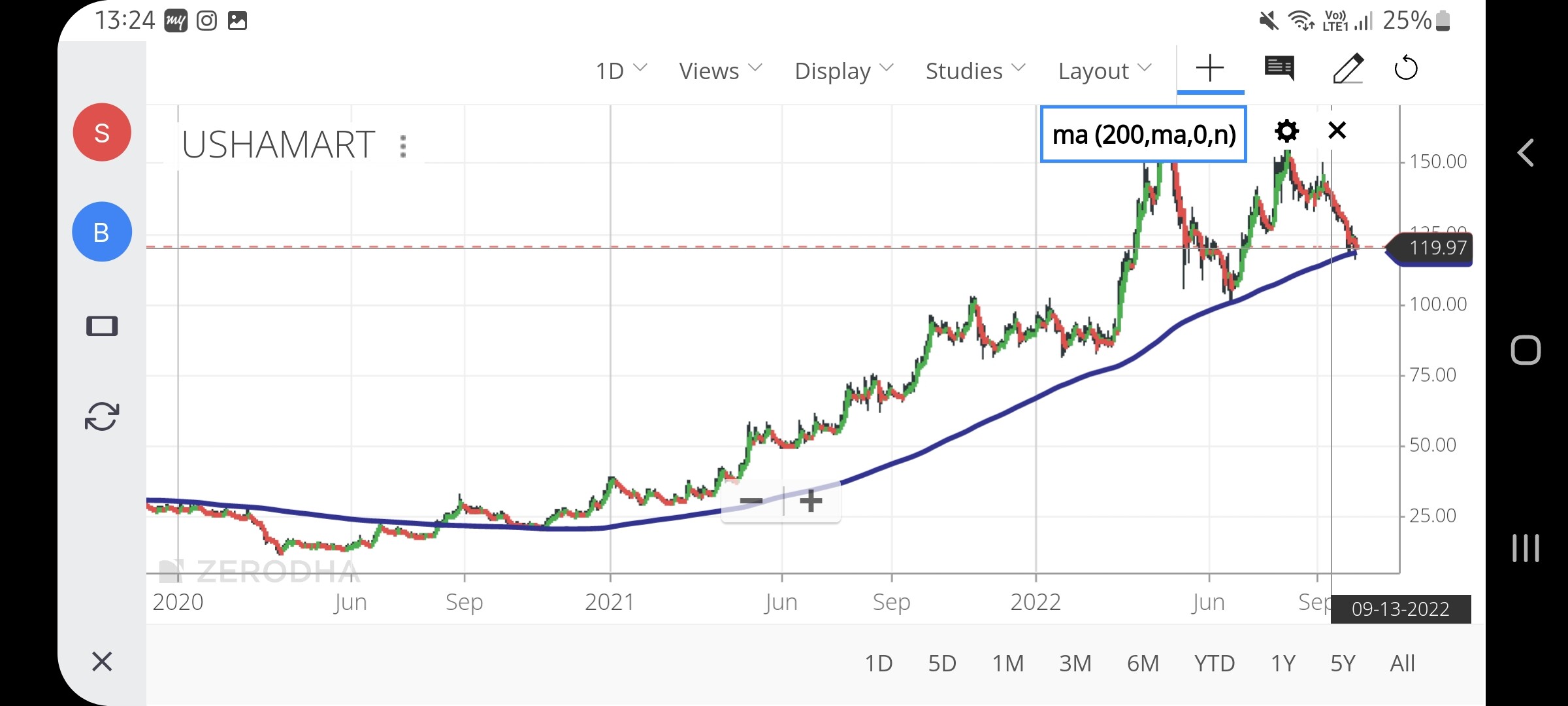

Mixing fundamentals with little technicals…

Standing at crucial juncture of 200 DMA.

Could this be a make or break below this level? Could it get too weak on technical levels if it breaks this level? Just asking for learning as it has not break 200 DMA from quite a long time now so if anyone has any views please share. Please see I have read business and know risks, etc Thanks

Mixing fundamentals with little technicals…

Standing at crucial juncture of 200 DMA.

Could this be a make or break below this level? Could it get too weak on technical levels if it breaks this level? Just asking for learning as it has not break 200 DMA from quite a long time now so if anyone has any views please share. Please see I have read business and know risks, etc Thanks

Edelweiss has raised $450 million through ESAF III funds.

Key Points from below:

I think AIF is where the action is as far as Edelweiss is concerned.

Edelweiss has raised $450 million through ESAF III funds.

Key Points from below:

I think AIF is where the action is as far as Edelweiss is concerned.

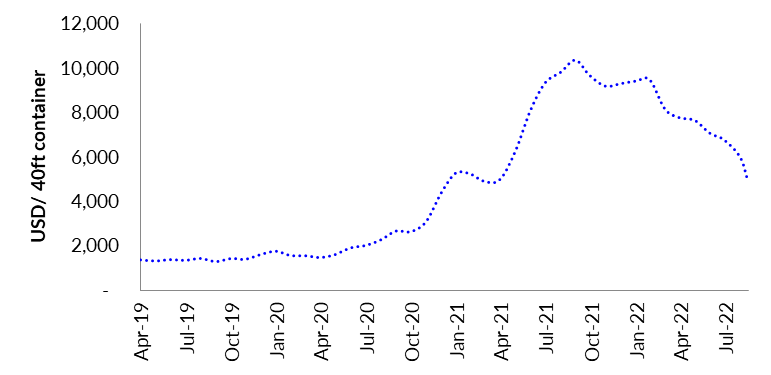

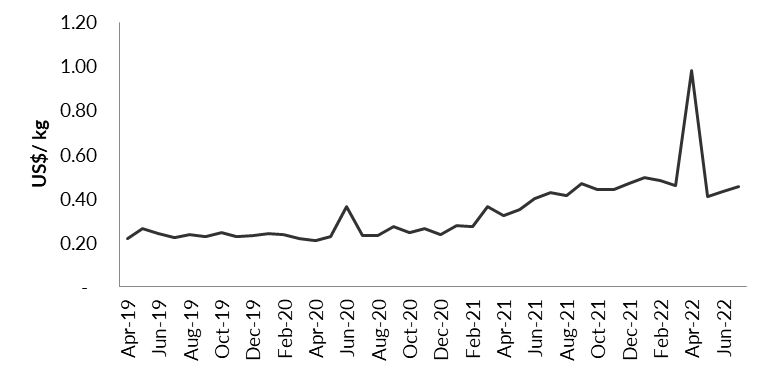

Though container freight costs have come down meaningfully, it is still 3.5x pre Covid levels and MDF import realizations are holding up. Stock is trading at a P/E of 10.9x after recent fall which is super cheap