S&P 500

Thanks sir for sharing this .C waves are brutal.

The following chart is US index . It is currently in C wave.

Hope this gives an idea on how C waves are good for bargain hunters.

S&P 500

Thanks sir for sharing this .C waves are brutal.

The following chart is US index . It is currently in C wave.

Hope this gives an idea on how C waves are good for bargain hunters.

Small correction:

At the moment 2M$ bond are being converted to shares @ 250rs.

= 652000 shares. (1 USD = 81.5 Rs)

= 0.065 cr shares

~0.96cr shares would be when the all FCCBs worth 30M$ would get converted. Which can eventually happen but hasn’t yet.

Wondering the same. Although I see no economical benefit to the promoter for selling. Mr Abdul has been selling his stake since last year at prices < 250 rs as well. Selling the shares just to buy FCCB and then getting it converted back to equity for what?

Disc: invested

The path forward is unclear. With low entry barrier in the industry, whether lalpath will grow at a pace which justifies it’s PE valuation.

Repeating the growth from COVID quarters is not possible.

Caplin Point FY22 Annual report highlights

FY 16 topline has become FY22 Bottom line. FY16 Topline 243 FY 22 Bottom-line – 308Cr

Operations target:

To backward integrate to KSM for 70% of US Products by FY24 to reduce costs.

Caplin Steriles has completed Pre mixed bags line, Filing will start in the US by Q4 FY23.

Capex

Invested over 355Cr in the last 5Years.

Will invest 500-560Cr Moving forward

300Cr in Expansion and maintenance

130Cr Oncology

100r API

Total R&D Spend(Capex+Opex) Stood at 20% of FY22 PAT.

Branded Generic Revenue share increased from 5% to 25% over FY12 and FY22.

African revenue doubled over 4years and focused mainly on branded generic products in Africa.

Asset light model where 55% of production is outsourced.

LATAM business:

In line to open its own distribution in Chile.

Filed 13 registrations in Mexico and 2 approved

44 Filed in Peru and approved 29

75 Registration in Chile and further 20 More in pipeline.

Have opened 33 retail chains and plan to take in to 50 by 2022 and in 2023 plan to launch a franchise model.

Online B2B Platform has grown 30%(trying to get exact numbers).

Caplin Steriles

75% is Own Products and 25% is CMO(contract manufacturing) for large players

API for caplin steriles will be organic and will come up in 18 Months.( previously they were planning to acquire API Plant in Vizag)

Expanding Caplin steriles 3 new lines, out of this 2 will be under a new unit and said new unit will have

provision to accommodate 4 more lines depending upon the demand in future.

Receivable Days and Inventory days

As company has entered tender business mostly government contracts thus having a longer receivable days and company has ventured into aggressive growth the where credit has to be given in terms of sales (previously an advance will be collected from customers and product will be supplied now this has changed) both of these factors were the reason the negative working capital has been changed.

Inventory days

The company has acquired and in process of acquiring its channel partners thus resulting in increasing the inventory days. Previously consignments in transit were considered as goods sold to channel partners thus reducing the inventory, since the company has acquired the channel partners only when the actual sales happen the inventory will be reduced.

However the company has maintained its inventory days significantly well below its peers and maintaining the receivable days/debtor days with its peers

Guidelines

20% Growth

30%+ Margins.

FY 22 topline will be FY 28 bottom Line – FY22 Topline 1300 CR

Will be under TOP 30 Indian Pharma Companies.

The Guideline is quite ambitious, the countries in which the companies operate currently have a combined population size of Tamil Nadu and they are entering Brazil and Mexico which have very large markets and expanding to other countries like Chile and Peru. Thus giving a revenue opportunity and entering regulated markets US & Canada etc.

Strategic partners: Eight road and F-Prime(A fund whose primary focus is Healthcare and technology) into Steriles gives more conviction.

2026 Guidance- LATAM Business revenue will double(LATAM & Africa revenue 1170 IN FY22) and Steriles will be 100 Million dollar (800CR REVENUE) Currently 130Cr. – Interview by COO Will double our topline in next 5 years: Caplin Point – YouTube

Disclosure: Invested

That period had covid revenue too, which may not be there going forward. And as @Tella asked if a comparative study with metropolis, thyrocare will give better picture. The analysis so far is good. Your finding of 23% ROE shows why Dr. Lalpath labs is industry leader.

For Our Regular Readers

We won’t be providing any stock updates on regular basis but would keep sharing our market views on time-to-time basis.

Our sir has told us not to be direct , not to say anything on SIP, PMS or keep-holding strategy. People don’t like that.

But we would be happy to answer any stock/marekt related query from our readers . Happy Selling ( for the time being, remember temporary bear market rally is over )

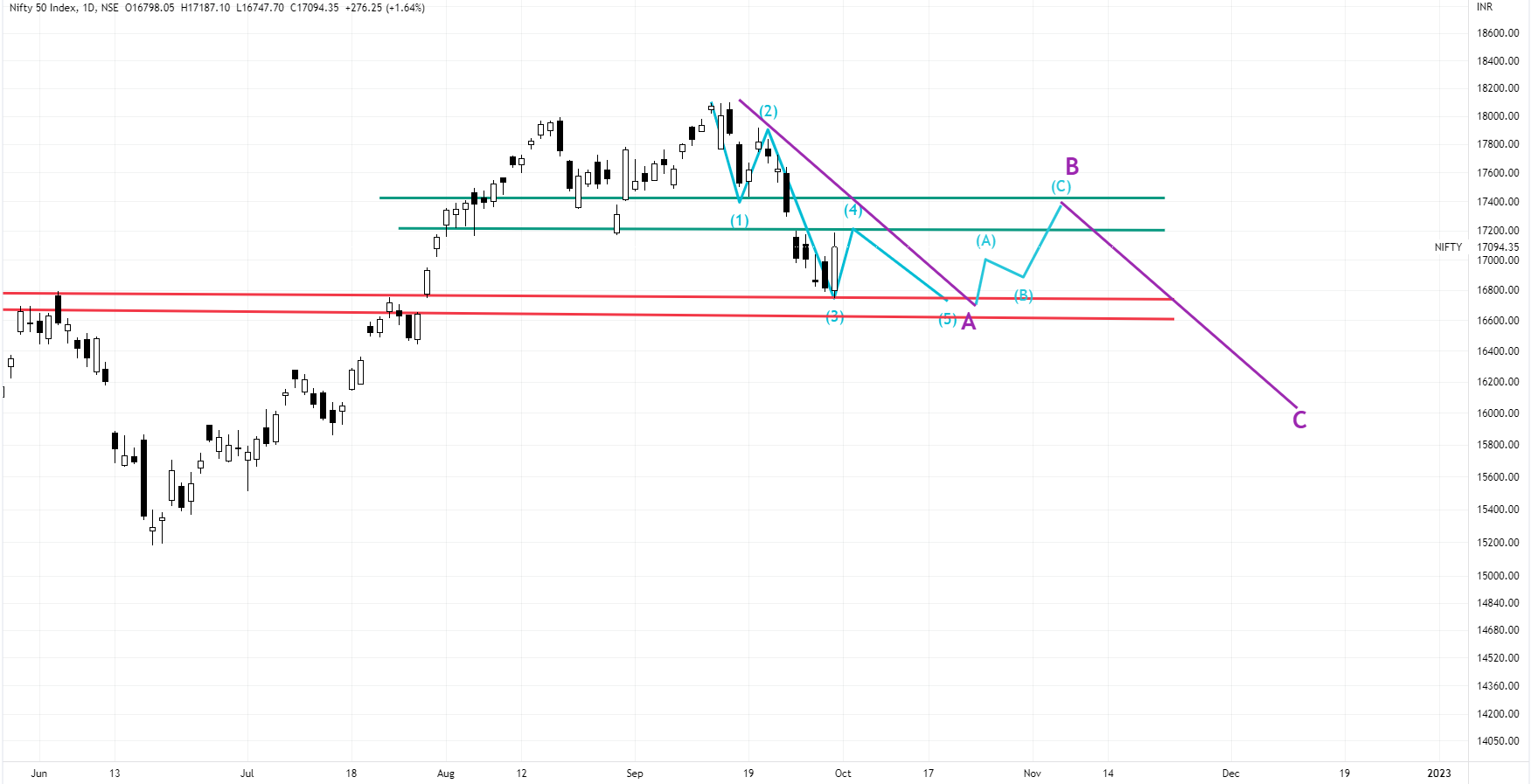

Nifty -Short to Medium Term Expectation

Short Term – Green Zone is important resistance zone for upside…if Nifty does not cross above 17430, we might follow this path . The skyblue lines can be likely the likely route.

Medium Term : Check the purple lines.

Long Term.…let’s review after 2 months whether we stop here or go to near to pre-Covid levels.

Historically Bear markets last 18 to 20 months in India . If we count from Oct 21, already 11 months are over. So best case scnario for bear market to end is April, 23.

Neuland labs was previously covered in another thread when it was undergoing its fall… It achieved its pattern target of 1000 and has been consolidating above that. Now it seems to be forming interesting confluence of patterns as shown in the following daily line chart.

First is obvious double bottom pattern with bottoms near 1000 and intervening peak near 1420. If and when it clears 1420 and pattern confirmation happens, pattern target can be 1800.

Secondly it has broken out of a small cup and handle pattern shown on right side of chart, with breakout above 1265, marked in dotted line. Pattern target for this pattern is 1470, (above the level needed to confirm a double bottom breakout)

Thirdly a symmetrical triangle breakout, marked on the chart, and a retest of both the breakouts, i.e from symmetrical triangle and cup and handle. Friday close was a good close, above 200 dema marked in fluorescent green.

disc: no positions… In watchlist. Posted for academic purpose as I have been following Neuland charts since a long time.

Even as the EV population grows, CNG vehicles are impacted due to rising cost of natural gas. The cost arbitrage was supposed to be a differentiator from petrol/diesel along with zero pollution. EVs have both these features. As such long term future of CNG vehicles and CNG stations looks bleak. Terminal value for any business related to CNG for automobiles needs to be reassessed. e.g vehicle tanks, CNG stations, cascades, etc.

Exited everything on August 15th.

Carrying only few postions in core portfolio : Tube Investment, Ingersoll Rand, Kennametal,Escorts,Poonawala Finance ,KPIT

Keeping a close watch.