I can’t recall the reasons but must be around management and compliance

Posts in category Value Pickr

Dr Lal PathLabs a well recognised brand in the Diagnostic Sector (30-09-2022)

How is it placed when compared to its nearest competitor like Metropolis Healthcare… This will bring out the reasons for higher PE for Dr Lal

Dr Lal PathLabs a well recognised brand in the Diagnostic Sector (30-09-2022)

How is it placed when compared to its nearest competitor like Metropolis Healthcare… This will bring out the reasons for higher PE for Dr Lal

Dr Lal PathLabs a well recognised brand in the Diagnostic Sector (29-09-2022)

Dr. Lal PathLabs: A look at the ROE of the company 2022

Dr. Lal PathLabs: Return On Equity Analysis

The Oracle of Omaha, Warren Buffett, famously said, “The best investment you can make is an investment in yourself. The more you learn, the more you will earn.” With this in mind, in this article, we will look at how we can use Return On Equity to gauge a company’s profitability and how efficient it is in generating profits.

How is ROE calculated?

The basic method of calculating ROE is:

Return on Equity = Net Profit ÷ Shareholders’ Equity

But this method does not tell the whole story. We should also look at how efficiently the company is using its assets and what is the company’s debt level relative to equity, because a high debt level relative to equity may also make ROE appear high. So, we can use the DuPont ROE formula to analyse the ROE in a better way.

DuPont ROE = (Net Income/Net Sales) * (Net Sales/Total Assets) * (Total Assets/Total Equity)

DuPont ROE = (Profit Margin * Total Asset Turnover * Equity Multiplier)

Let’s look at Dr. Lal PathLabs’ income statement and balance sheet, and then we will calculate the ROE.

Required data from the Standalone income statement and balance sheet of Dr. Lal PathLabs for the year ended 31 March 2022 and 2021.

Return on Equity calculation using basic ROE formula:

Return on Equity (2022) = 3,440.54 ÷ 14,764.69 = 23.30%

Return on Equity (2021) = 2,801.06 ÷ 12,170.85 = 23.01%

Sorry I am not able to bring table here. See ROE table

As we noted above, the basic ROE formula and DuPont Formula provide us with the same answer. However, by using DuPont analysis we can see that the company is using its assets efficiently to generate high revenue and the company is also able to turn a good percentage of revenue into net profit. Here we can also see that the equity multiplier of the company is also not so high. It means that the assets are mostly funded by equity and retained earnings and the company does not use so much debt.

Now, to know whether an ROE of a company is good or bad, we will compare it with its industry average. The average ROE of companies in the healthcare industry having similar market capitalisation as that of Dr. Lal PathLabs is approximately 18%. So, the ROE of Dr. Lal PathLabs seems more impressive when compared to the average ROE of its peers.

Conclusion:

Although Dr. Lal PathLabs does use debt, its debt level is still low. The company has a high return on equity of 23.30%. It means the company is reinvesting its retained earnings efficiently to generate a high rate of return. This has caused substantial growth in the earnings of the company. The net Profit of the company has grown from Rs.168.00 crore in 2018 to Rs.344.10 crore in 2022.

Dr Lal PathLabs a well recognised brand in the Diagnostic Sector (29-09-2022)

Dr. Lal PathLabs: A look at the ROE of the company 2022

Dr. Lal PathLabs: Return On Equity Analysis

The Oracle of Omaha, Warren Buffett, famously said, “The best investment you can make is an investment in yourself. The more you learn, the more you will earn.” With this in mind, in this article, we will look at how we can use Return On Equity to gauge a company’s profitability and how efficient it is in generating profits.

How is ROE calculated?

The basic method of calculating ROE is:

Return on Equity = Net Profit ÷ Shareholders’ Equity

But this method does not tell the whole story. We should also look at how efficiently the company is using its assets and what is the company’s debt level relative to equity, because a high debt level relative to equity may also make ROE appear high. So, we can use the DuPont ROE formula to analyse the ROE in a better way.

DuPont ROE = (Net Income/Net Sales) * (Net Sales/Total Assets) * (Total Assets/Total Equity)

DuPont ROE = (Profit Margin * Total Asset Turnover * Equity Multiplier)

Let’s look at Dr. Lal PathLabs’ income statement and balance sheet, and then we will calculate the ROE.

Required data from the Standalone income statement and balance sheet of Dr. Lal PathLabs for the year ended 31 March 2022 and 2021.

Return on Equity calculation using basic ROE formula:

Return on Equity (2022) = 3,440.54 ÷ 14,764.69 = 23.30%

Return on Equity (2021) = 2,801.06 ÷ 12,170.85 = 23.01%

Sorry I am not able to bring table here. See ROE table

As we noted above, the basic ROE formula and DuPont Formula provide us with the same answer. However, by using DuPont analysis we can see that the company is using its assets efficiently to generate high revenue and the company is also able to turn a good percentage of revenue into net profit. Here we can also see that the equity multiplier of the company is also not so high. It means that the assets are mostly funded by equity and retained earnings and the company does not use so much debt.

Now, to know whether an ROE of a company is good or bad, we will compare it with its industry average. The average ROE of companies in the healthcare industry having similar market capitalisation as that of Dr. Lal PathLabs is approximately 18%. So, the ROE of Dr. Lal PathLabs seems more impressive when compared to the average ROE of its peers.

Conclusion:

Although Dr. Lal PathLabs does use debt, its debt level is still low. The company has a high return on equity of 23.30%. It means the company is reinvesting its retained earnings efficiently to generate a high rate of return. This has caused substantial growth in the earnings of the company. The net Profit of the company has grown from Rs.168.00 crore in 2018 to Rs.344.10 crore in 2022.

The harsh portfolio! (29-09-2022)

With a sharp price drop in RACL Geartech, I have increased its position size from 1% to 2% and changed its basket from being a deep value bet earlier to now being a cyclical bet. As cash position was anyway zero, I have reduced position size in Manappuram Finance from 4% to 2%. Interestingly, I didn’t have to sell shares of Manappuram to reduce the position size, the sharp cut in stock prices did the job ![]()

Last couple of years have been really good for RACL with strong earnings growth coming in on the back of continued sales growth and expanding margins. Market has also recognized the same and stock has moved up a lot and doesn’t trade at very cheap multiples anymore. From a near term perspective, RACL can be adversely impacted due to on-going European energy problems. However, the management seems very confident of achieving 20%+ sales growth while maintaining margins over the next 3-years. If that happens, I expect their PAT to reach 45-50 cr by FY25 (20%+ EPS growth on FY22 base). However, valuations are also fair at 20x earnings. Given the risk reward, I have still not made it a full position and limited exposure to 2%. Updated folio is below and cash remains at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (5%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

The harsh portfolio! (29-09-2022)

With a sharp price drop in RACL Geartech, I have increased its position size from 1% to 2% and changed its basket from being a deep value bet earlier to now being a cyclical bet. As cash position was anyway zero, I have reduced position size in Manappuram Finance from 4% to 2%. Interestingly, I didn’t have to sell shares of Manappuram to reduce the position size, the sharp cut in stock prices did the job ![]()

Last couple of years have been really good for RACL with strong earnings growth coming in on the back of continued sales growth and expanding margins. Market has also recognized the same and stock has moved up a lot and doesn’t trade at very cheap multiples anymore. From a near term perspective, RACL can be adversely impacted due to on-going European energy problems. However, the management seems very confident of achieving 20%+ sales growth while maintaining margins over the next 3-years. If that happens, I expect their PAT to reach 45-50 cr by FY25 (20%+ EPS growth on FY22 base). However, valuations are also fair at 20x earnings. Given the risk reward, I have still not made it a full position and limited exposure to 2%. Updated folio is below and cash remains at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (5%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

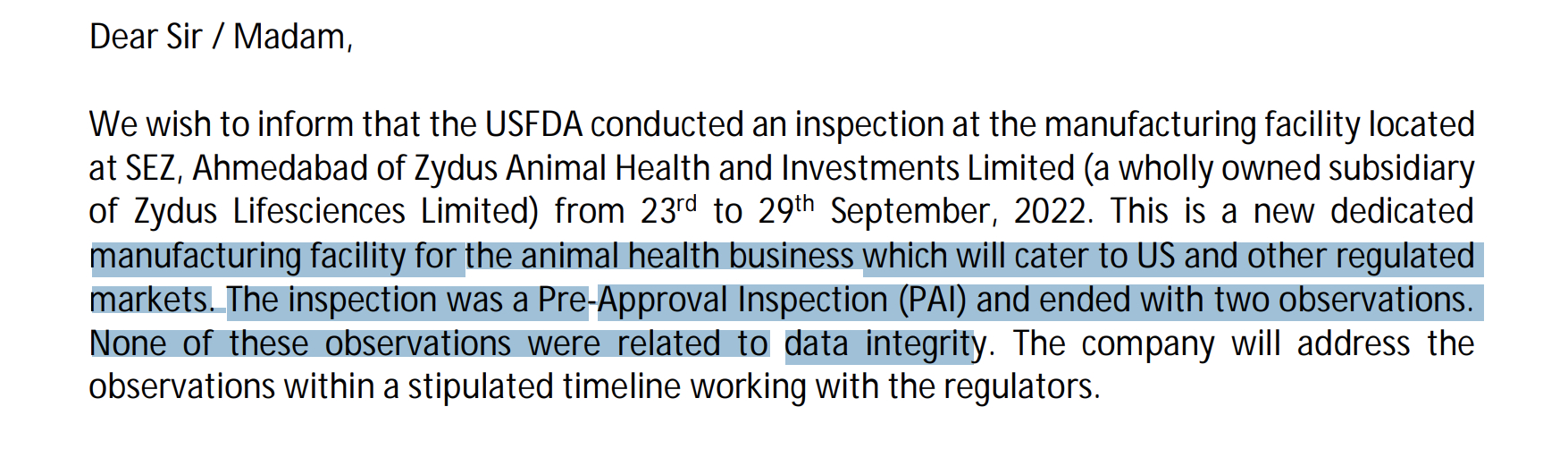

Zydus Lifesciences (Erstwhile: Cadila healthcare) (29-09-2022)

Its good to see that Zydus has started filing products in animal healthcare division for the US. Earlier, they had divested their Indian healthcare business to focus on regulated markets.

Disclosure: Not invested (no transactions in last-30 days)

Zydus Lifesciences (Erstwhile: Cadila healthcare) (29-09-2022)

Its good to see that Zydus has started filing products in animal healthcare division for the US. Earlier, they had divested their Indian healthcare business to focus on regulated markets.

Disclosure: Not invested (no transactions in last-30 days)

Modison metals (29-09-2022)

Management had a recent investor interaction where they talked about their business and growth ambitions. It was a very good interaction.

https://www.youtube.com/embed/3EVm8jhk8qU

Disclosure: Invested (position size here, no transactions in last-30 days)