Also – 1600 into 25% PAT * 30 PE

12,000 Market.

I don’t see any major reason to transition from a sleeping partner to an active partner for few years.

Also – 1600 into 25% PAT * 30 PE

12,000 Market.

I don’t see any major reason to transition from a sleeping partner to an active partner for few years.

HDFC’s price-to-earnings (PE) derating story from the last 3 years:

(Source: Finology Ticker)

Over the past 3 years, HDFC Bank’s stock has been trading within a range-bound territory.

Earnings Growth vs. Price Performance

From March 2021 to March 2024, HDFC Bank’s Earnings Per Share (EPS) significantly increased from ₹56.8 to ₹85.83. That’s an impressive growth of ~50%.

Despite this notable earnings growth, the stock’s 3-year price return is -2.61%.

According to financial theory, stock prices are heavily dependent on earnings growth.

Let’s Explore what are the Odds against HDFC

HDFC Bank is India’s biggest bank in terms of market cap. However, the strong pressure in the banking sector might be contributing to its inability to sustain levels above ₹1,750.

The average advances increased with small numbers:

On the other hand, the average deposits increased slightly:

In Q1 FY25, the growth fell short of expectations:

Seasonal variations and unexpected outflows from current accounts have also adversely affected deposit stability. While average deposits have remained steady, liquidity constraints have become a significant concern. They are witnessed by a shift of funds from fixed deposits to the Indian share market as investors pursue higher returns in equities.

Recently published data by CRISIL indicate that the household savings rate (net household savings/GDP) fell to a six-year low of 18.4% in fiscal 2023.

As a result, the overall profitability gets impacted due to increasing the cost of funds and leading to the Net Interest Margin (NIM) contraction.

Another major concern is the imbalance between loan and deposit growth. HDFC Bank’s deposits grew by 26.4% in the previous year, compared to a 55.2% expansion in the loan book. This disparity raises regulatory concerns.

The Reserve Bank of India (RBI) worries about the narrowing gap between loan and deposit growth rates. Thus, it is posing challenges for HDFC Bank to sustain its loan book growth without adequate deposit growth.

The liquidity challenges and competitive cost of funds affect not just HDFC Bank but also the entire private banking sector.

Banks play a critical role as the backbone of the economy. Yet, the recent Q1 FY25 GDP growth slowdown to 6.7% from 8.2% a year ago underscores the urgency for action.

It’s just a matter of time before the RBI and the Indian government implement a revival plan to address these structural liquidity issues. Although near-term pressures are expected to persist, they could be resolved within the next two to three quarters.

The real question is: will HDFC Bank seize the opportunity?

If the stock has to break and sustain above the crucial level of ₹1,800, it will require a solid quarterly result and an above-average deposit growth rate that outpaces its peers.

The stage is set, but time will only tell whether HDFC Bank rises to the challenge.

Corporate Governance Concerns at Kitex Overstated? Business Expansion and Capex Plans May Offer Safety?

Few of my points, done mainly during my investment time

corportae issues at kitex over stated! Expansion may offer safety for investors.pdf (142.4 KB)

Hi…

Aaron Industries was listed in September of 2018, and you can read their annual report of 2019-20, which includes their growth philosophy.

The market cap was barely Rs 20cr, but they were confident in their strategy and philosophy for growing. (Read past annual reports)

Few points to be noted in last 5 years about the performance of the company:

My only concern is that management doesn’t do con-calls and hence the information is limited. However, they used to respond any investor query over the email with full details in a timely manner.

Disclaimer: Invested from lower levels and biased. No buy/sell recommendation by any means.

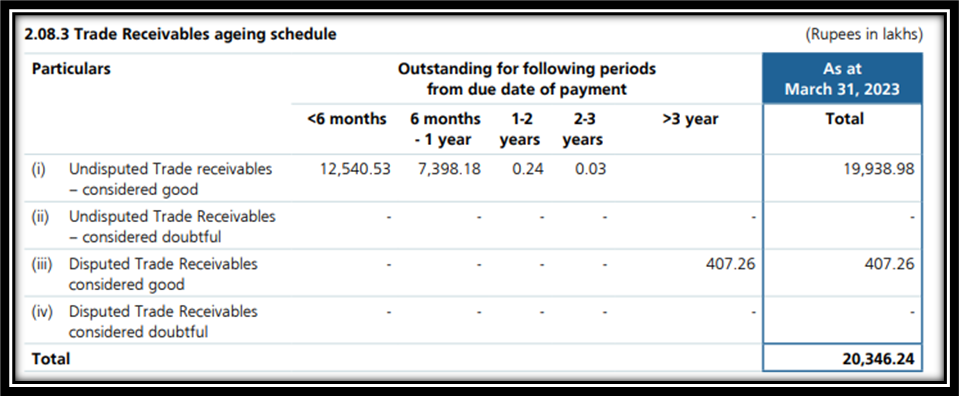

Is the trade receivables are that risky ?

A comparison of PAT v/s net cash operating activities

Kitex Garments 2019 2020 2021 2022 2023 2024 Total

PAT 71 103 54 124 57 56 465

CASH from operatiions 9 51 116 -10 295 -38 423

Based on the data, I don’t see any significant red flags suggesting profit manipulation, except for an investment in Kitex USA LLC, an associate company, amounting to ₹27 crore, which has impairment triggers but has not been written off in the books.

However, I don’t believe this sum poses a serious threat to the company’s existence or its ability to continue as a going concern.

Additionally, a review of their trade receivables shows that they are within a reasonable range, further supporting the stability of their financial position.

Disc – Sleeping investor from 150 – 200 range

@hnk_so The spirit of the forum is to do some work yourself and then ask for feedback or inputs. This is not a paid expert network providing insights to people who want to deploy money. All participants contribute to the work.

tried libgen? it usually has everything,

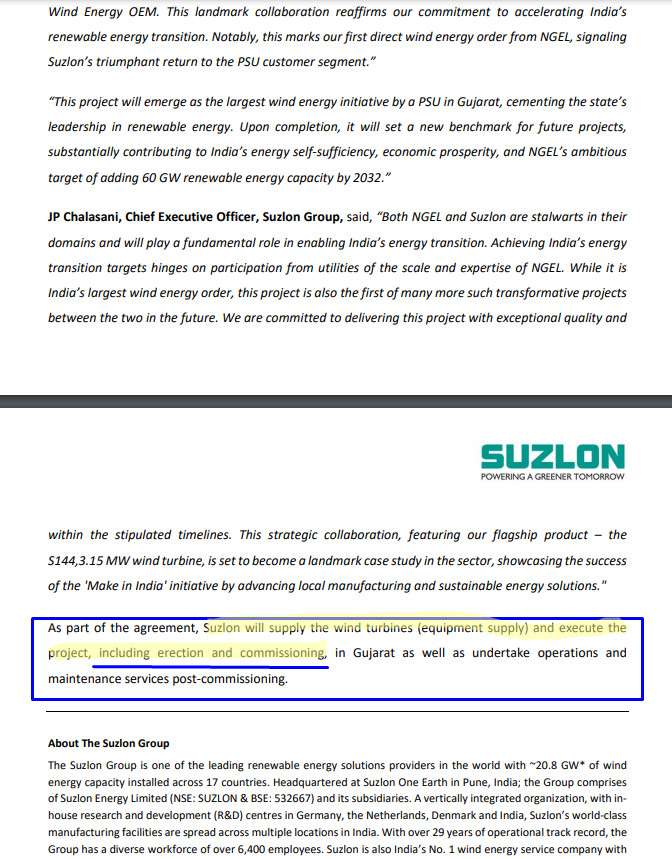

This would mean a lot of heavy duty cranes would be rented out by Suzlon. The question is whether Suzlon will rent out the ones by Sanghvi Movers Limited or do it in house?

Oh okay absolutely will definitely will be joining the next meeting you will have. Please do let me know if you I need to come prepared for any investment thesis that I may have or if it will be an open forum ? How long will the meeting be for ?

Looking forward to it !