Thanks for posting this, did BFS share quarterly results? I was under the assumption BFS would share half yearly in November.

Posts in category Value Pickr

Sirca Paints India Limited (09-09-2024)

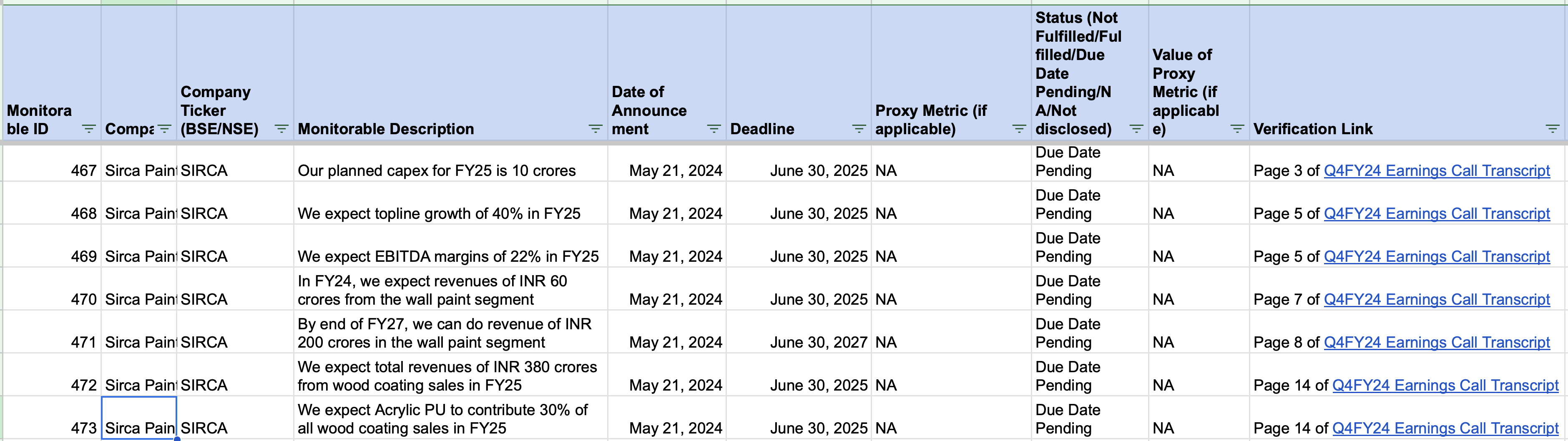

In the below tracker, I have started tracking important company goals for Sirca. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-42.xlsx (148.6 KB)

Rajesh’s portfolio (09-09-2024)

They have changed business pls look at annual report, the website should be functional in due course. I trust them fully as they have been fully transparent when things were going down, never misled.

Mazagon Dock: aptly called “Ship Builder to the Nation” (09-09-2024)

Mazagon Dock bags order worth ₹1486 crores from ONGC

Indigo Paints: Upcoming Star (09-09-2024)

Peak XV (formerly Sequoia capital) sells 22 pc stake in Indigo Paints to investors like Morgan Stanley, Mercer, HDFC MF.

Investing Basics – Feel free to ask the most basic questions (09-09-2024)

How attending AGM helped in your investment journey? I have tuned in (live/recorded) a few after the VC facility was made available, but most of them turn out to be a waste of time due to behavior of the management as well as minority shareholders. Do you have any good experiences about the AGMs? Request your views covering the name of the company, likables and decision worthy moments, & others. Thanks.

Investing Basics – Feel free to ask the most basic questions (09-09-2024)

How attending AGM helped in your investment journey? I have tuned in (live/recorded) a few after the VC facility was made available, but most of them turn out to be a waste of time due to behavior of the management as well as minority shareholders. Do you have any good experiences about the AGMs? Request your views covering the name of the company, likables and decision worthy moments, & others. Thanks.

Mangalam Organics Ltd. – A promising Pine chemistry story (08-09-2024)

Recently researched this stock and my views –

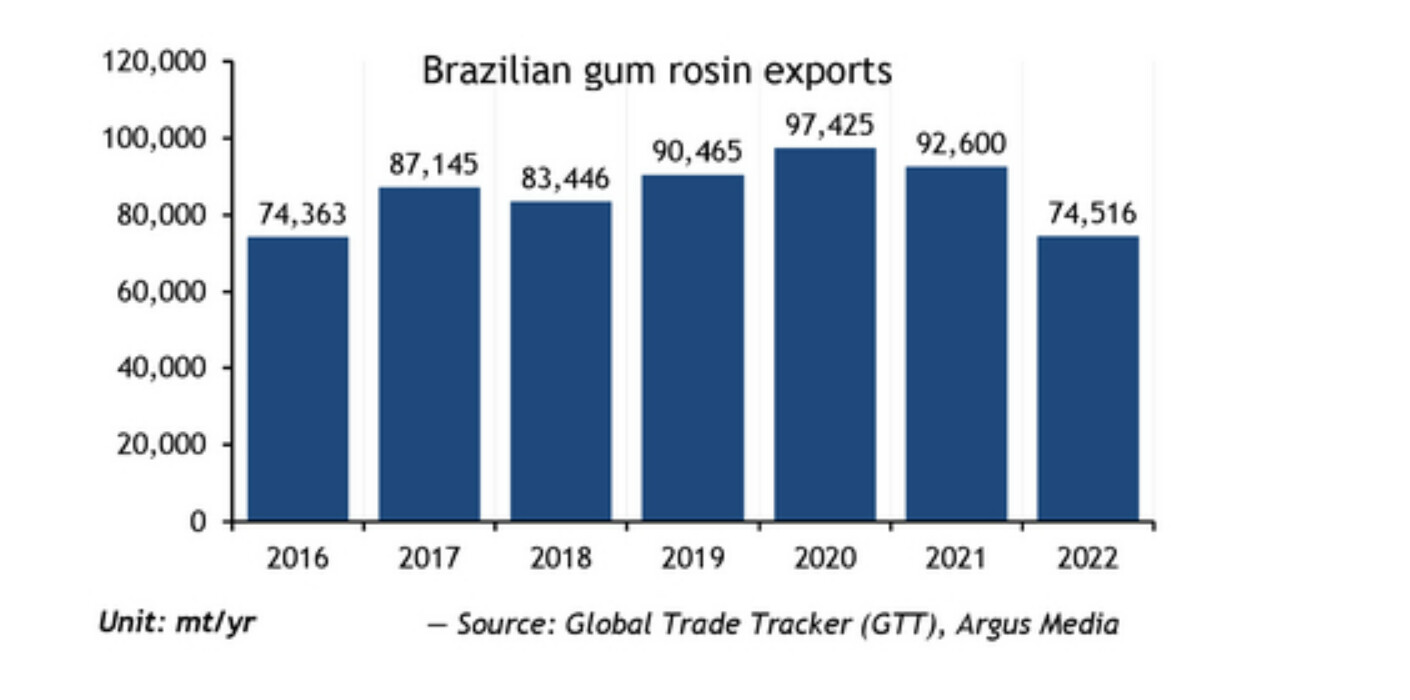

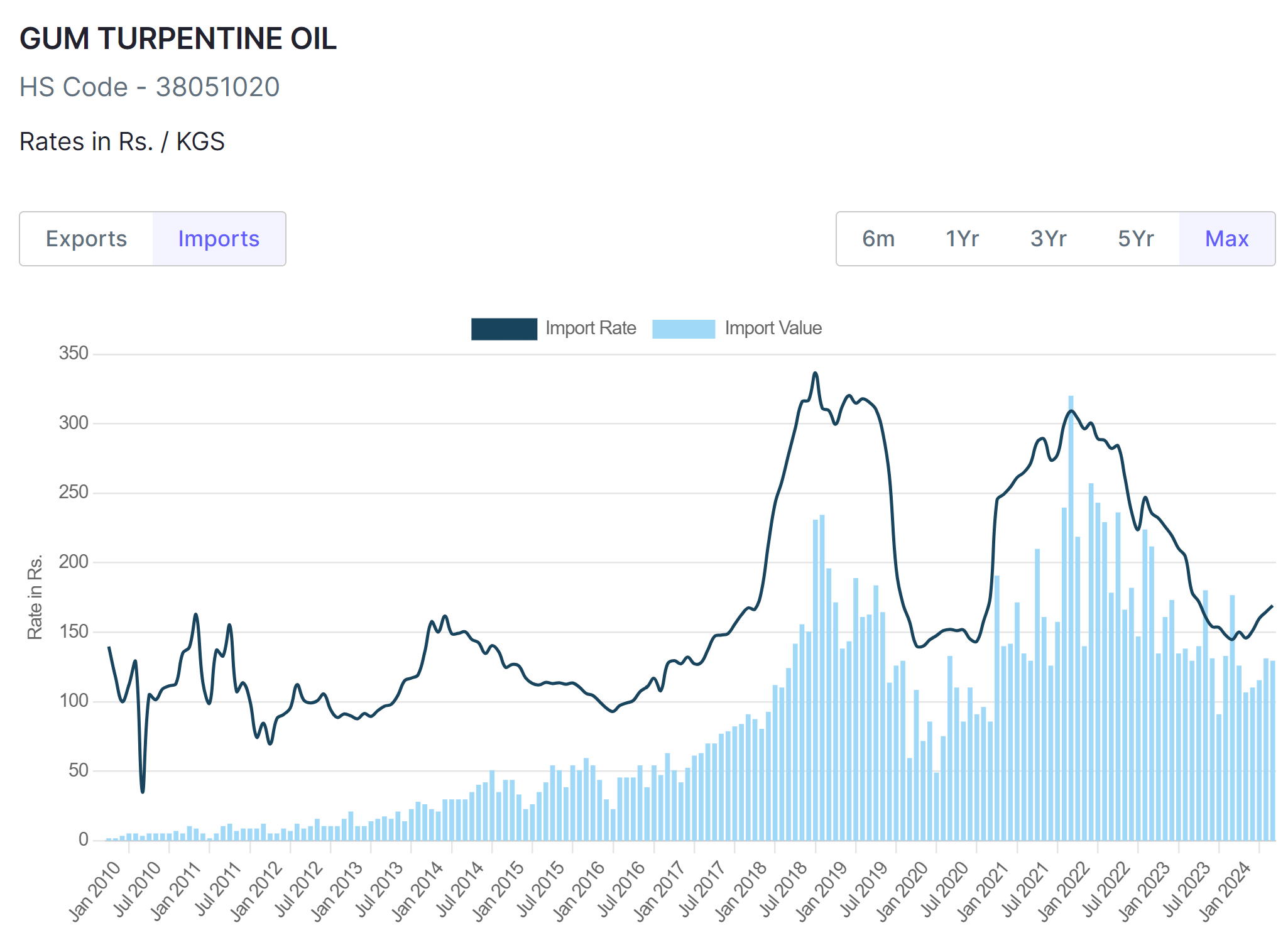

Pine Rosin (which comes from Pine tree tapping industry in Brazil) is going through a sharp downturn. Brazil pine oleoresin supply to fall further in 2024 | Latest Market News This has reduced supply of raw materials in the synthetic camphor supply chain. Lower Pine Rosin production implies lower Gum Turpentine which goes into Camphor production. This is why the cycle is turning. The last upcycle was from mid 2016 to mid 2018.

If we go through the article I shared above – “With selling prices sometimes below production costs throughout this year, many smaller pine oleoresin suppliers have ended forest lease agreements. Even if pine oleoresin prices increase, allowing for higher margins, it would take time for the producers which left the market to reactivate the forests and increase availability to the market. Reactivating a forest takes about six months as tappers need to prepare the extraction of the raw material months in advance, according to a source.”

Please note the exports of Pine Rosin now is the lowest in the last decade. Low exports coincides with cyclical bottoms in Camphor and Gum Turpentine prices.

Now, coming to why Mangalam Organics, the company’s retail products are growing at a rapid rate. A consumer brand with 160cr sales and growing 60% YoY is probably worth 500-700Cr in valuation, compared to the total market cap currently which is 550Cr. The company has also doubled capacity recently and capacity wont be a bottleneck in the upcycle. At peak capacity utilization in an upcyle, revenue will be ~800-1000Cr. If margins are similar to last upcyle which was around 20-25%, book value for Mangalam Organics will double in 2-3years. In last upcycle, the stock traded at 5-6x Price to Book Value at Peak. All this is contingent on the cycle turning for a few quarters.

SmallCap Hunter : Trying to find the dark horses with triggers (08-09-2024)

Any views or counter views on Trust Fintech and SA Tech Software ?

SmallCap Hunter : Trying to find the dark horses with triggers (08-09-2024)

The company looks strong on several fronts, including a low debt-to-equity ratio, significant fixed assets, and its highest YoY profit, with TTM profits continuing along the same trajectory.

However, the stock price is currently at an all-time high and appears to be in Stage 3 (consolidation at upper levels), which could be risky. If demand remains steady or grows, the Stage 2 (bull trend) may persist.

While profitability has dipped due to rising material costs, the company has managed to control other expenses. Additionally, 20-30% of its income comes from non-core sources.