Can anyone please share how is the experience for the users of Zaggle? On the Google Play Store, the average rating is 3.7, and in the last two months, the maximum rating is a 1-star rating.

The customer churn ratio is negligible. So, that says that clients are happy with Zaggle but the Play Store reviews are saying some other story. Can anyone please throw some light on this

Posts in category Value Pickr

Zaggle_A platform to address pain points for enterprises (08-09-2024)

Caplin Point Laboratories (08-09-2024)

Annual Report FY24:

• Today we have 30,000+ distribution touch points in the LATAM market alone.

• Today we address 36 therapeutic areas of treatments that cover 65% of the WHO’s essential drug list.

• Our branded generics have increased from 5% of our revenues in FY12 to 25% of revenues in FY24, in emerging markets.

• We invested over `500 Crores in R&D between FY14 and FY24. While our R&D spend stood at 4.5% of our revenues in FY24 we were not hesitant to increase it to 10.9% in FY19 when it was the need of the hour.

• Consistently building, an increasingly end-to-end integrated business: Our strategy has been to be in control of our business value chain to the greatest extent possible. By being present across the value chain, we will be able to reach markets better, deliver better products, sell higher volumes, gain better margins, establish knowledge might and keep innovating as per the need of the hour. Today Caplin is present right from the production of certain KSMs and APIs to Clinical Research (CRO) to Innovative and branded Generics Production to Owned ANDAs and to maintaining a robust distribution network.

• Filed Company’s first Emulsion injection for the approval of USFDA with a partner

• 90 products registered in Chile which had shown a growth of 37% in comparison to the previous year in revenue terms.

• Completion of registration of 25 oncology products with 50 more product registrations in the pipeline in LATAM market, particularly in Nicaragua and El-Salvador.

• Company receives major orders for Speciality products from LATAM. Orders would be serviced using CMOs initially, before moving to own high potent site in the next few months.

• Company has filed several products in non-US markets such as Canada, Australia, Mexico, South Africa, China etc. Some approvals and launches are expected during the current financial year.

• “As a company we focus on Good Distribution Practices and fondly call it GDP – A mainstay of our success”

LATAM:

• Key to our continuous growth in Latam has been our ability to understand the changing dynamics on a firsthand basis because of our local presence in these countries. The first thing we understood going into FY 2024 was that the COVID-related business was coming to a quicker end than other companies were able to foresee. We continued to keep an eye on our stock positions and also the stocks at our wholesalers and retailers, especially on these products to make sure that we never had an impacting expiry issue or a sales return issue.

• While most of our competitors turn to even copy the color of our tablets and our boxes, they fail to understand that price is not the only motivator for a local retailer.

That’s the main reason we continue to launch newer products and innovative drug delivery systems that smaller countries in Latam are not used to. We launched 9 different products in pre-filled syringes. We launched 35 other molecules in OSD, soft gels and injectable in FY 2024.

• We have successfully registered 24 oncology products in Central America and they contributed to $3.2m in sales during the financial year.

• We have 50 products in the pipeline which will get us desirable margins in the next two years.

• CHILE: Two countries we are banking on for the next financial year are Chile and Mexico. We have around 90 products registered in Chile and have won Cenabast contracts for 15 products that will be going through to FY 2025. Chile has shown a growth of 37% in comparison to the previous year. We have recently appointed a country head for Chile to head our local operations. Previously, we were exporting to importers but with a basket of 90 products, we believe that it’s the right time that we started being closer to our customers in Chile as well.

• MEXICO: We exported our first million dollars to Mexico in 2024. We may only have 7 products registered but there are 23 in pipeline which will eventually be approved before the end of 2024 or early 2025. We have also struck deals with 4 large Chinese companies that have FDA or EU approvals for oncology, penicillin and Cephalosporin preparations for Mexico. In total we are yet to file around 50 products in Mexico from our own facilities and these Chinese partners. Our soft gel facility in Puducherry passed INVIMA inspection which means that we will be able to register our fastmoving gelcaps also in Mexico.

• VENEZUELA: We have our eyes set on Venezuela too for 2025. We will be filing 50 fast selling molecules in that country based on our previous experience. The regulations are slowly changing in this country, which is for the better for companies focusing on selling quality products at affordable prices. Previously, anyone with a freesale certificate could export to Venezuela through an import permit. The MOH is putting a restriction on such permits, and it will be only through permanent sanitary registrations that a company would be able to export into Venezuela. We will be well prepared when that law comes into existence in 2025.

• When we started two of our own retail pharmacies in 2008 in Guatemala as an experiment, little did we know that this experiment would lead to such a huge advantage in having a say in future product launches. Although we couldn’t reach the magic number of 50 retail stores this year, we managed to open 4 more to reach 45 retail stores. We have a database of 46,000 chronic patients who are affiliated to our loyalty program by name “plan confianza caplin” where we give them the third month prescription for free if they purchase the first two months.

• Caplin aims to complete further expansion (under a separate FEI number), within the next 18 months, where 4 more production lines will be added. This unit will have the highest levels of automation and will be digitalized entirely from day one.

• There is no alternate to having “skin in the game”, especially when it comes to growing a fledgling business, and one where the variables are numerous in number. Our chairman has been at CSL facility managing overall strategy and operations for the last couple of years and we’re glad to report that the result is in plain sight for everyone to see. The same is well appreciated by the numerous auditors who have visited the facility.

• Total employees – 2625 (vs 1275 yoy)

Total workers – 2257 (vs 611 yoy)

Investment in the ancillaries, or ancillaries of ancillaries-vendors of famous companies (08-09-2024)

Leverage is one of the riskiest ways to go. You are right.

Kitex Garments Limited (08-09-2024)

Strengths and Challenges at a Glance !

Macfos Limited- A niche E-commerce Company (08-09-2024)

High profitability of Macfos is attracting competition.

https://nsearchives.nseindia.com/corporate/DRONE_02092024134722_DroneHubOnline.pdf

Quote “Drone Destination has launched a new e-commerce Drone Hub platform offering drones, drone parts and consumables, avionics and BIS-approved drone batteries for the drone industry. This new business vertical shall ensure timely supply-chain support to the Indian drone eco-system and offer customers with efficient after-sales service.”

Ranvir’s Portfolio (08-09-2024)

IKIO Lighting –

Q1 FY 25 concall and results highlights –

Sales – 127 vs 108 cr

EBITDA – 17 vs 23 cr ( margins @ 13 vs 21 pc )

PAT – 12 vs 14 cr

Completed Block -1 of Greenfield expansion of 2 lakh sq ft in Q4 FY 24. Commercialised the same in May 24. Expected to complete Block – 2 of another 2 lakh sq ft by Mar 25. Have started construction for block -3 of another 1 lakh sq ft. Combined capex spend for all three blocks is around 200 cr with a total yearly revenue potential of 1000 cr ( incremental. It may take 3-4 yrs to reach optimum capacity utilisation for all 3 blocks )

ODM Listing segment grew both on YoY and QoQ basis. Performance in domestic mkt was flat. Export sales were aided by exports to Gulf region, inventory reduction in US for company’s RV products

EBITDA margins impacted due to front loading of expenses like higher employee expenses ( up 40 pc YoY ) due completion of new Greenfield Capex. Expect significant contribution from this facility in H2. This facility is also producing 2 new products – earphones of various kinds and smart watches

In addition to RV business in US, have started supplying Industrial and Solar products to energy service companies in US

Gross margins were stable Ex-US operations. As US operations stabilise, expect gross margins to normalise going fwd

Company maintains FY 25 guidance of 20-25 pc revenue growth for FY 25 with EBITDA margins ranging between 20-22 pc !!!

Company has already started backward integrating the wearables and hearables segments. Company is also looking at the design aspects in these segments. Aim is to keep the RoCE high, even if there is some margin dilution

Seeing descent pickup in the LED lighting industry in FY 25 after a difficult FY 24

Company believes that they are an electronics manufacturing and design company at heart. Lighting is the biggest chunk of their business – that’s a different matter. It’s their electronics manufacturing and design DNA that makes them confident of venturing into wearables and hearables. Anything to do with – plastics + metals + electronics – they r good at it and they r capable of doing it in-house

Disc: hold a small tracking position, biased, not SEBI registered, not a buy/sell recommendation

Responsive Industries: Luxury Flooring Brand? (08-09-2024)

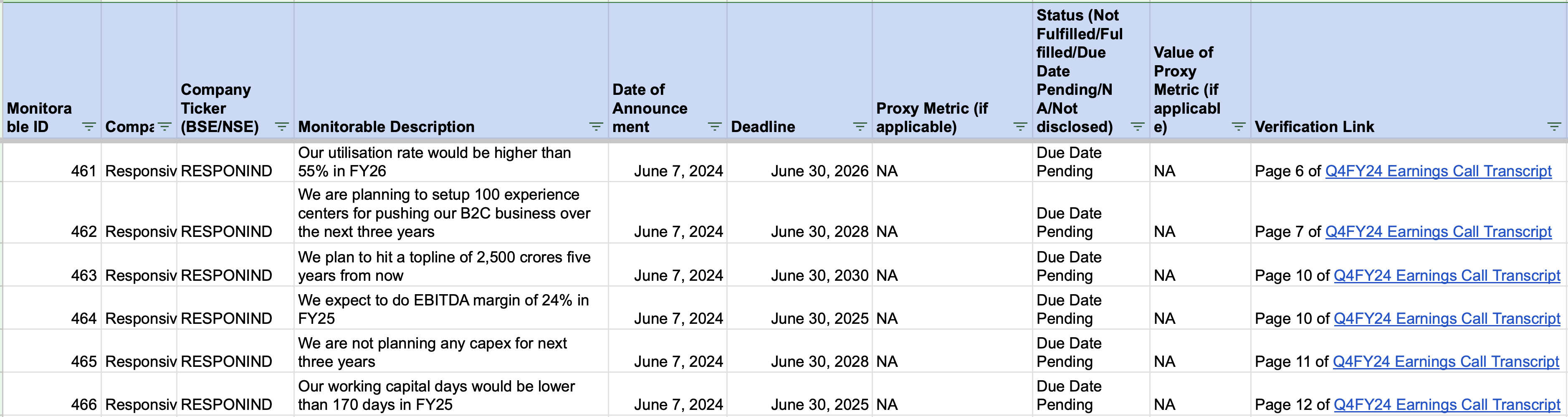

In the below tracker, I have started tracking important company goals for Responsive Industries. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-41.xlsx (148.2 KB)

52 week highs and all time highs strategy (08-09-2024)

Weekly

daily

Gujarat Fluorochemicals has broken out of a triangle consolidation (orange lines in the weekly chart and blue lines in the daily chart) over the last one year approx.

The management has guided for better revenue Q3 onwards of this year.

The LFP plant under the battery segment is going to be commissioned this quarter. The fluoropolymers vertical will start seeing numbers from the second half of this year.

disc: Not invested yet.

ValuePickr Surat (08-09-2024)

I’m interested, sent you a DM. thanks!

HBL Power: Signs of change (08-09-2024)

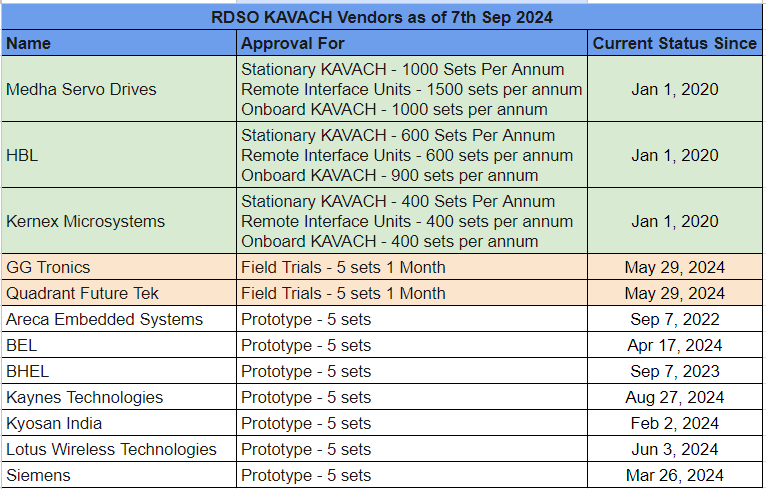

I downloaded the latest list of all RDSO approved vendors for KAVACH. I was surprised to see that all vendors, including Medha, HBL and Kernex, are listed as “developmental” vendors and not “approved” vendors.

Among developmental vendors there are 3 different levels of approval:

- Development Vendor with supply capacity limit – Medha, HBL and Kernex

- Development Vendor for field trials only – GG Tronics and Quadrant

- Development Vendor for prototype only – 7 companies. See the table below.

The actual PDF downloaded from IREPS website is attached.

KAVACH Vendor Directory 07-Sep-2024.pdf (2.6 MB). I have extracted and distilled the information in the table below.

Approval Has Capacity Limits

So as you can see, not only are there 3 different levels of approval, the final approval also has a limit on capacity. Apparently RDSO also assesses supply capacity per annum. In one of the interviews the Railways Minister Ashwini Vaishnav also talked about awarding contracts based on manufacturing capacity. So now it all makes sense.

I am not sure how long does the process from field trial to final approval take. GG Tronics and Quadrant received the go ahead for field trials on 29th May 2024. As of today they have approval only for 5 sets of KAVACH (which means KAVACH for 5 station side equipments, 5 trackside and 5 onboard locomotives). So it appears to me that these 2 companies are not competing in the currently released tenders. The other 7 companies – big names like BEL, BHEL, Siemens etc. are not even eligible. I may be wrong, someone needs to cross check.

KAVACH Will Keep on Evolving

Also, as I mentioned before, everyone is a “developmental” vendor now. No one is an “approved” vendor yet. This means the KAVACH systems will undergo further changes. Currently it is at version 4.0 (previous was version 3.2). So it looks like the whoever is on the latest version will always have an advantage as far as eligibility for tenders is concerned. What I mean to say is – lets say a company has approval for ver 3.2 and wants to go for ver 4.0, then there will be some time lag due to RDSO’s testing and evaluation process. The tenders released are always for the latest version and if a new tender arrives before the company has received the approval for the latest version then they will not be eligible for the tender.

What would be the reason behind RailTel signing the “exclusive” MoU with Quadrant? I understand the MoU part, but not the “exclusive” part. Quadrant has a lot to gain out of an exclusive tie up with RailTel, but I am not sure if RailTel has. Logically speaking RailTel should be open to working with any RDSO approved KAVACH vendor. Anyways a MoU is not a binding legal agreement, so I would not read too much into it. The timing is also suspicious, just 1 month before they filed the DHRP.