Hi Chetan. Cyclical they could be, but OIL India is a very good company. If you ignore the noise on the channels, which stock isn’t down by 10-30% these days? As OIL has come down from 733 to 664, the fall is of some 14%. To me this appears reasonable.

Of course, if I had entered it right before the slide started, it would have given me cold sweat too.

I am not tracking it any long, but to me it seems like a safe bet.

Posts in category Value Pickr

Oil India- has its time come? (06-09-2024)

Piccadily Agro Industries Ltd (06-09-2024)

Its best to obtain clarification bcoz paid-up capital can be considered to be just (the number of shares x Face Value). Any share sale premium goes into reserves & surplus under other equity.

SWAN ENERGY LIMITED (SEL): The company focussing on sectors with strong tailwinds (06-09-2024)

Operational Review for each business vertical of Swan Energy Limited based on the annual report for the fiscal year 2023-24:

1. Oil & Gas Division

Overview:

The oil and gas segment was a major contributor to the company’s revenue, reflecting Swan Energy’s strategic positioning in this sector. The global energy market’s volatility was effectively leveraged to enhance both output and revenue.

Key Developments:

- Revenue Contribution: This division contributed significantly to the 249% year-on-year increase in consolidated revenue, reaching ₹5,01,714.60 lakhs.

- FSRU (Floating Storage Regasification Units) Deployment: The deployment of FSRUs allowed the company to capitalize on the rising demand for liquefied natural gas (LNG). These units are pivotal to Swan Energy’s strategy of becoming a key player in the global LNG market, allowing flexible transportation and regasification of LNG, reducing bottlenecks in supply.

- Future Growth Potential: With the completion of the Swan LNG project expected in the next fiscal year, the division is set to further strengthen its presence in the oil and gas sector. Once operational, the project is expected to generate a new stream of steady revenue.

Challenges:

- Global Market Fluctuations: Despite the rise in revenue, the oil and gas division faced market challenges due to fluctuating global oil prices. However, Swan Energy mitigated these risks through strategic sourcing and FSRU deployments.

- Logistical Issues: The volatility of oil prices and geopolitical instability caused some logistical challenges, but the company responded with strategic adjustments to its operations.

2. Shipyard & Defence Division

Overview:

The acquisition of Reliance Naval and Engineering Limited (RNEL) in January 2024 marks Swan Energy’s foray into the defense and shipbuilding sectors. This acquisition is a critical move toward diversifying its operations.

Key Developments:

- Acquisition of RNEL: The acquisition, through the National Company Law Tribunal (NCLT) process, allows Swan Energy to enter the defense shipbuilding and repair sectors. RNEL’s strategic location and infrastructure provide a competitive advantage for Swan Energy in the defense sector.

- Restoration and Job Creation: Restoration efforts are underway to bring the shipyard to full operational capacity. Once fully functional, the shipyard is expected to create over 4,000 direct jobs, which will be a significant boost for the company’s industrial workforce.

- Strategic Importance: The defense sector is a growing market in India, and Swan Energy’s entry into this vertical positions it to tap into government contracts for naval and defense-related shipbuilding and repairs.

Challenges:

- Infrastructure Restoration: The process of restoring the shipyard to full capacity involves significant investment and time. This is a key focus for the coming year.

- Integration into Operations: Integrating the new acquisition into Swan Energy’s broader operations is a complex process that will require strategic coordination across departments.

3. Real Estate Division

Overview:

Swan Energy’s real estate division continues to focus on premium real estate developments in key Indian cities, with strong sales and potential future growth.

Key Developments:

- Completion of Cardinal One, Bengaluru: The division obtained the Occupation Certificate for Cardinal One, a significant milestone that will allow Swan Energy to proceed with the sale of inventory in the upcoming fiscal year. The project is expected to see full sales in the next year, contributing to revenue growth.

- New Developments: The company is actively exploring new real estate opportunities in Mumbai and Bengaluru, two of India’s most lucrative real estate markets.

- Land Assets: The company plans to utilize its large land holdings in Mangaluru and Bengaluru for future projects, potentially contributing significant long-term value.

Challenges:

- Real Estate Market Volatility: Although the real estate market has been recovering, it remains sensitive to economic conditions, interest rate fluctuations, and regulatory changes. Swan Energy will need to navigate these risks as it expands its real estate footprint.

4. Veritas Petroleum Division

Overview:

The Veritas division focuses on the petroleum products segment, which delivered solid performance driven by market disruptions and increased demand for petroleum products in India and Southeast Asia.

Key Developments:

- Revenue Growth: Veritas clocked a revenue of ₹3,85,455.36 lakhs, showing strong growth driven by the company’s ability to leverage industry disruptions and meet demand. The net profit margin improved from 4.4% to 4.8%.

- Bulk Sourcing and Optimization: Enhanced bulk sourcing strategies and optimized asset utilization were key to Veritas’ profitability, allowing the division to reduce costs and improve operational efficiency.

- Geographic Expansion: The division has capitalized on opportunities in Southeast Asia, a growing market for petroleum products, by delivering consistent and timely services.

Challenges:

- Market Disruptions: While the division benefited from market disruptions, volatility in crude oil prices and global supply chain issues posed significant challenges. The company responded with a focus on cost management and strategic sourcing.

- Environmental Regulations: Stricter regulations around the environmental impact of petroleum products could increase operational costs in the future, requiring proactive adjustments.

5. Textile Division

Overview:

The textile division remains a critical part of Swan Energy’s diversified portfolio. Despite sector-specific challenges, the division showed resilience by maintaining operational efficiency.

Key Developments:

- Capacity Utilization: The division operated at optimal capacity during the year, focusing on maximizing output despite challenges in the broader textile sector.

- Cost Management: Through effective cost management strategies, the textile division managed to improve its EBITDA margins. This was achieved by reducing operational wastage and improving procurement processes.

- Market Positioning: Although facing global headwinds in the textile industry, Swan Energy’s textile division has retained a competitive position in the market, supplying high-quality textile products.

Urban enviro waste management (06-09-2024)

Investor presentation

URBAN_06092024131053_Letter_NSE_Investor_presenatation.pdf (6.3 MB)

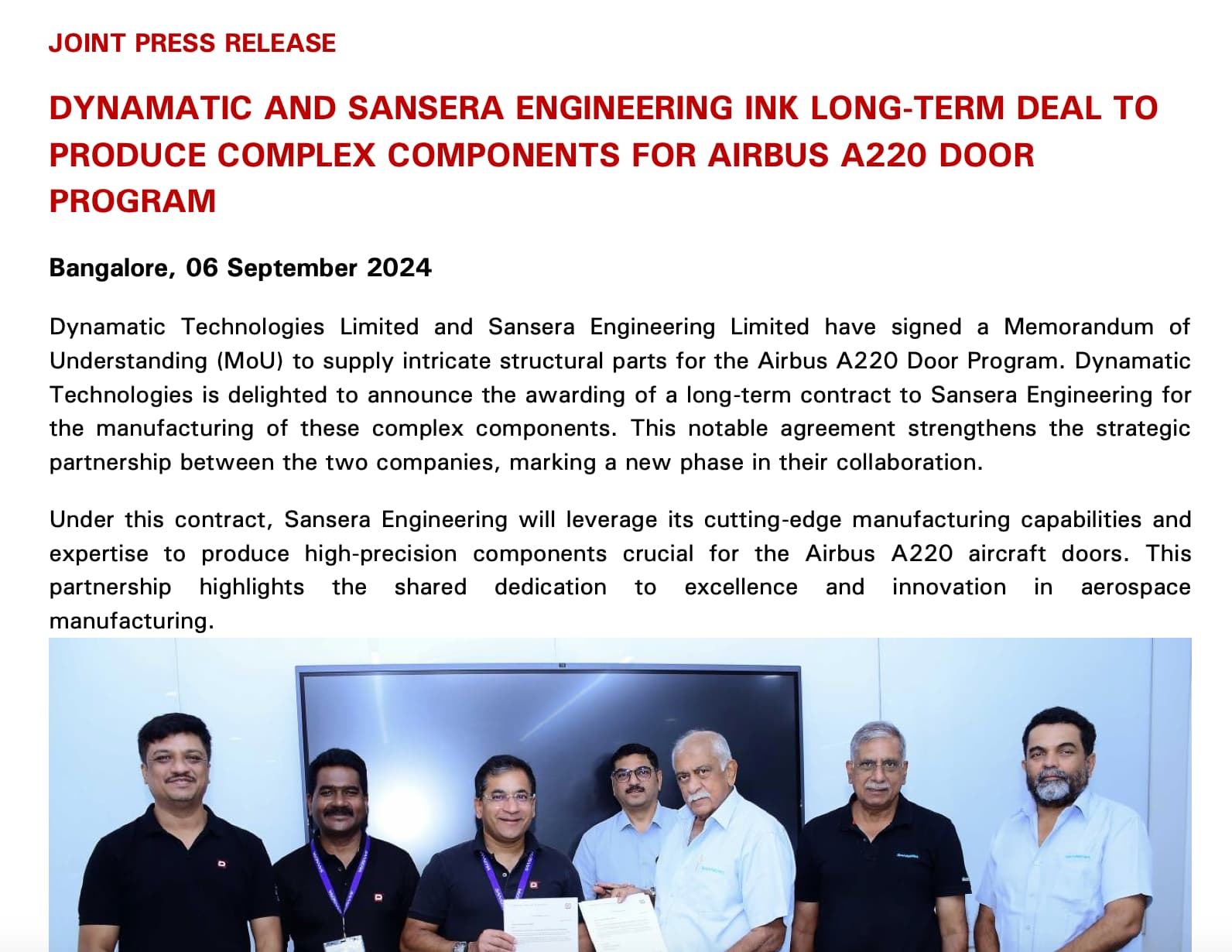

Sansera Engineering (06-09-2024)

DYNAMATIC AND SANSERA ENGINEERING INK LONG-TERM DEAL TO PRODUCE COMPLEX COMPONENTS FOR AIRBUS A220 DOOR PROGRAM

Hero Motor – Leader in two wheeler (06-09-2024)

I think this would be a market wide hit.

There will be a big battery revelation. This big new battery compound will solve many issues(obv, bringing with it a new set of challenges).

But the only question is when will this revelation happen. Will it already be too late. Or will it be after the whole 1st gen of all EV gets to become useless.

Only time will tell.

Luckily I’m not in the market for any 2 wheeler.

Medplus Health Service second largest pharmacy retailer (06-09-2024)

Two interviews of the CEO on media explains his philosophy, how he built the company, mistakes along the way and vision going forward quite well. These are quite old though. I have summarized them and also provided the link to the original talk below.

Madhukar Gangadi @ TiE Hyd Healthcare BootCamp for Healthcare Startups

- Was able to start in 2006 with 48 stores in 4 months with initial borrowed capital

- Plan is to add 1000 stores a year for many more years to come in the future

- Initial sales strategy was to go to corporates and sell them discount cards which were additional discounts over an above offered to general public

- Entered Bangalore market pretty early post Hyderabad and burnt a lot of money as the openings were too fast

- Expansion in Hyderabad was easy as had many personal connections which worked and made the task easier. However in Bangalore and Chennai this did not work as there was no connection

- In a retail business scaling up via a cluster based approach is far better and profitable as well

- Tried the experiment of putting up clinics and pharmacy adjacently but failed because stores are not well built and thus difficult to get good name doctors to come to these clinics

- Failed in Medplus beauty which was launched at the start of the ecommerce stage but suffered cash burn and this was not able to take off as it was earlier than the business should have been

- For a chronic patient medicine is basically a commodity as they are buying it every month

- Facing resistance in terms of non validity of e prescription which has made it difficult but still able to sell online due to the omnichannel model

- Main reason for existence of branded generic in India is because it enforces quality of manufacturing

- The medicine is not just about chemical composition but also because of the way the medicine is made and the efficacy it will have

- 24×7 opening of stores makes no financial sense and cannot be done on a full scale model considering the costs. In an emergency situation hospital is better than a medicine shop

TiE Leadership Series by Mr. Madhukar Reddy, Founder & CEO – Medplus Health Services Limited

- Second son in the family and first son is an engineer

- Till 2019 from 2005 used just Rs 260 crores of capital post which Premji Invest put in Rs 200 crores and post that in the IPO in 2021 end raised Rs 600 crores

- Auditor has been Big 4 and Warburg Pincus was on board and also invested for a long time

- From 2011-19 the company had raised just Rs 100 crores including both debt and equity

- Promoter mentions multiple times company would have gone bankrupt but funding came in at the right time since inception

- CTO was one of the initial hires who helped build all softwares in house and that is now helping in save licensing costs for softwares

- Since Day 1 have been very clear that Medplus as a brand should be known only for value pricing and not fancy stores

- Better to focus on one good idea as capital is limited, energy that a human being can devote is limited and small things that entrepreneurs keep doing eventually are not successful

- Promoter admits that he too is guilty of falling under the excitement of starting a business from an exciting idea but his ultimate understanding is that all of this is a waste of time and a promoter must focus on just one business

- In a retail business profitability is not a challenge but scale is

- Differentiates with Apollo in the sense that Medplus is not fancy and just provides value

- Apollo is backed by a big company and hence was able to grow faster than MedPlus for some time and has fancy stores while MedPlus is more functional with best price and frugal operating structure

Piramal Pharma Limited (06-09-2024)

Piramal Pharma was discussed by Sajal Kapoor in the recent Twitter space.

How not to Invest! #Biosecure #Sajal Kapoor #Aditya Khemka #Prince #AI

Please watch from 24 minutes on the timeline.

Solara Active Pharma Sciences – Pure Play API (06-09-2024)

Sajal Kapoor discussed Solara Pharma in the recent Twitter space.

https://www.youtube.com/watch?v=1OFHKI_LCWY&t=80s

Please watch from 18 minutes on the timeline.