Because I am even unable to open the website, what would be the peak revenue potential

Posts in category Value Pickr

Waaree Energies Ltd. – Is it just the Dawn? (26-11-2024)

Did they mention at what rate the sales will grow in the next 2-3 years?

All the GW projections looks good but would be helpful if we get an approx sales CAGR.

Microcap momentum portfolio (26-11-2024)

@visuarchie Thanks for making all the hard work and giving the community a flavor of momentum. I have been following the thread as well as other momentum strategies for quite a few years now. Eager to know that whether this strategy can be implemented in case of Microcap companies (Between 500Cr – 2000Cr.) . I believe the fluctuation in terms of price is quite high in those segment, but so is the risk-reward. Has anybody tried it ? In case , you have some verified result, the entire community may be interested.

Gokaldas exports — cup and handle/rising channel (26-11-2024)

- Q2 FY25 consolidated revenue grew by 85% YoY, including contributions from acquired entities.

- Standalone revenue growth (excluding acquisitions): 28% YoY.

- Consolidated EBITDA grew by 48% YoY, but margins were affected due to seasonality and currency impact in acquired entities (kenya).

- Generated INR 155 crores in cash from operations in H1 FY25.

- Strong order book and favorable market tailwinds.

- Revenue growth driven by export recovery, particularly to the US (+33% YoY growth).

- Consolidated EBITDA margin was 7% due to seasonality; standalone EBITDA margin at 11%.

- Management expects consolidated EBITDA margins to exceed 10% in the near term and reach 12% at steady state.

- Targeting annual revenue growth of 15%, supported by capacity expansion and strong demand.

- Consolidated production volumes: 14.95 million pieces in Q2; standalone entity contributed 8.1 million pieces.

- Standalone revenue capacity for Q2: INR 650 crores, with potential to reach INR 700 crores per quarter at full utilization.

- Madhya Pradesh Unit 2 expansion to contribute INR 175 crores annually .

- Leveraging global shift in sourcing from China, Vietnam, and Bangladesh to India.

- Strategic relationships with major global brands like GAP, JCPenney, Carhartt, and Columbia.

- Focus on growing market share with existing top-tier customers and diversifying product offerings.

- Approximately 80% of receivables covered under ECGC or supply chain finance programs.

- Consolidated inventory strategies supported by robust order book and capacity expansion plans.

Standalone EBITDA margins expected to improve by 1% YoY over FY26 and FY27.

Current facilities operating at full capacity; new expansions underway to meet demand.

Margins expected to improve as global inventory levels stabilize and demand strengthens.

Blended tax rate expected to remain around 22% due to tax benefits in specific locations.

Top five customers contribute 65%-70% of revenue, with significant runway for deeper penetration. - Investing INR 100 crores in FY25 for capacity expansions, including new units in Madhya Pradesh and South India.

- Enhancing vertical integration through investments in BRFL fabric processing to reduce lead times and improve cost efficiency.

- Increasing automation to boost productivity and operational efficiency.

- Strong demand for high-margin products like women’s fashion and sportswear.

- Seasonality and currency fluctuations, particularly in acquired entities.

- Freight costs and reliance on imported raw materials for certain operations.

- Madhya Pradesh Unit 2 construction to begin in Q3 FY25 and operational by H2 FY26.

- Incremental capacity expansions at Atraco and Matrix to increase consolidated revenue potential.

- Exploring leased capacities in South India for quicker expansion.

- 25% of standalone raw materials are imported, with higher reliance in Q1/Q2 for winter programs.

- Tariff changes and potential policy shifts in the US could further boost India’s export competitiveness.

- Order book remains robust, with strong traction in Q3 and Q4 driven by spring 2025 production.

- Management confident in maintaining growth momentum into FY26, targeting INR 1,250 crore annual run rate from new capacities.

- Expanding relationships with strategic customers for high-value products.

Risks: - Dependence on a few key customers (top customer contributes ~27%).

- Pricing pressure in a competitive global market.

Midcap Momentum Portfolio (26-11-2024)

Z Score and Sharpe Ratios does give different result.

Reason being Sharpe ratio is considering fixed value for ALL stocks- say Annual FD returns but Z Score is considering the mean of ALL the stocks and stddev too for ALL.

Scanned against last and considered 8.5% annual FD return for the sharpe ratio, and got 15 similar stocks out of 20.

No one is to judge which is better. Even if we backtest, with so much overlap and just 5% allocation, I dont think it will yield much of a difference over say 5-6 years XIRR.

That being said, Z score makes more sense as we are already ranking based on returns.

Sharpe might be better in long term strategies like mutual funds. but ranking each stock based on sharpe and exiting it the next week/fortnight/month because it fell short of returns to qualify the list doesn’t make sense. Momentum strategy is short term whcih we will be running for long term. So sharpe will make sense if our rebalncing frequency is quarterly or semiannually. OR we can incorporate that when our PORTFOLIO starts showing more volatility (and not any individual stock)

Am I making any sense here? ![]()

Windsor Machines Ltd (26-11-2024)

Earlier in the year the company was sold to Plutus investments and thereon more recently Madhu Kela amongst others and promoter participated in fundraise

business updates awaited

Screener.in: The destination for Intelligent Screening & Reporting in India (26-11-2024)

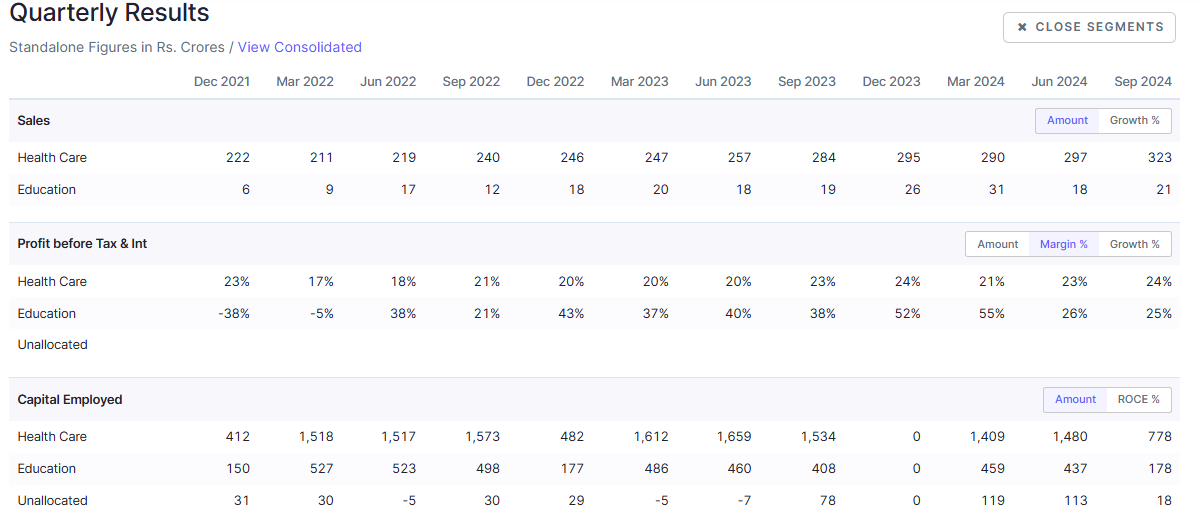

Hi @kowshick_kk, I am checking segmental data of KMCH on screener, in this it looks like capital employed data is not correct for Q1FY25 & earlier quarters (also annual numbers). Have also shared this on support but havent got any response, could you kindly look into this?

CC: @pratyushmittal

Tata Motors – DVR (26-11-2024)

Unless the car can do magical stuff or there is twist on the next part of the ad where a jaguar eats the ghastly models , nobody but Keir Starmers ardent and rich followers are going to buy it. Jaguar management somehow took Elliot Carver too seriously . Disregarding 95% for the sake of 5% may seem a good idea to politicians but hardly any man or woman will want to be seen driving a car so explicitly promoted for the LGBTQ+ .

Neuland Laboratories Limited – Transformation towards niche APIs? (26-11-2024)

8B99130C_1E34_4C42_B6A5_824642958A80_172126.pdf (415 KB)

Promoter buying small quantity at this valuations also

Sky Gold ltd. – Will it reach the sky? (26-11-2024)

Sharing the recent concall transcript

I hope you will find it helpful.

dr.vikas