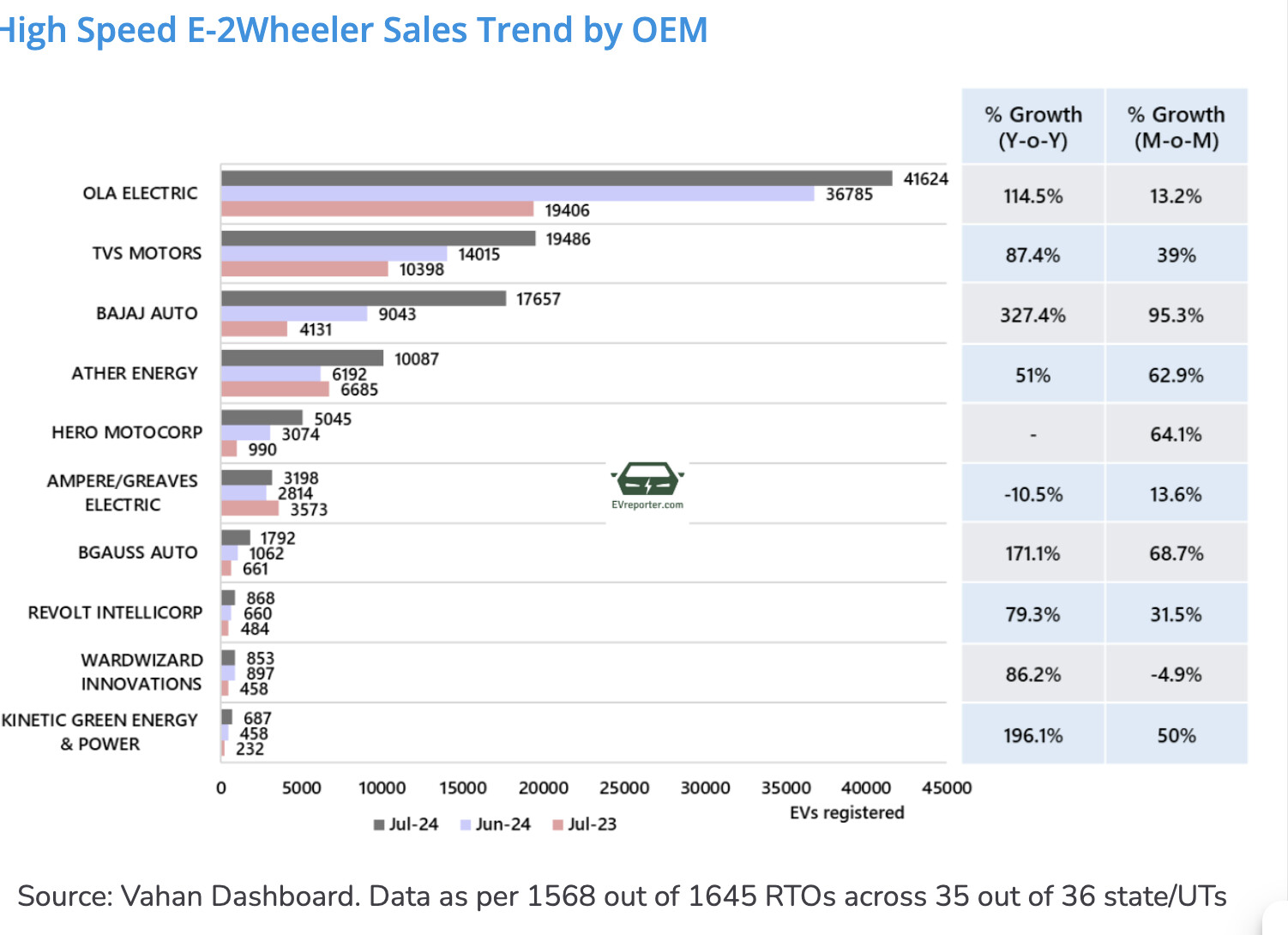

Based on the latest data for July 24 TVS Motors and Bajaj Auto are doing good growth.

Based on the latest data for July 24 TVS Motors and Bajaj Auto are doing good growth.

That’s due to IND AS 116, where lease liabilities are now considered a part of debt.

Remove that and debt to equity is around 1.

1 year : 2023-09-01

6 months : 2024-03-01

UFLEX , RTNPOWER → Out from List

Dhanuka , tidewater → IN into List

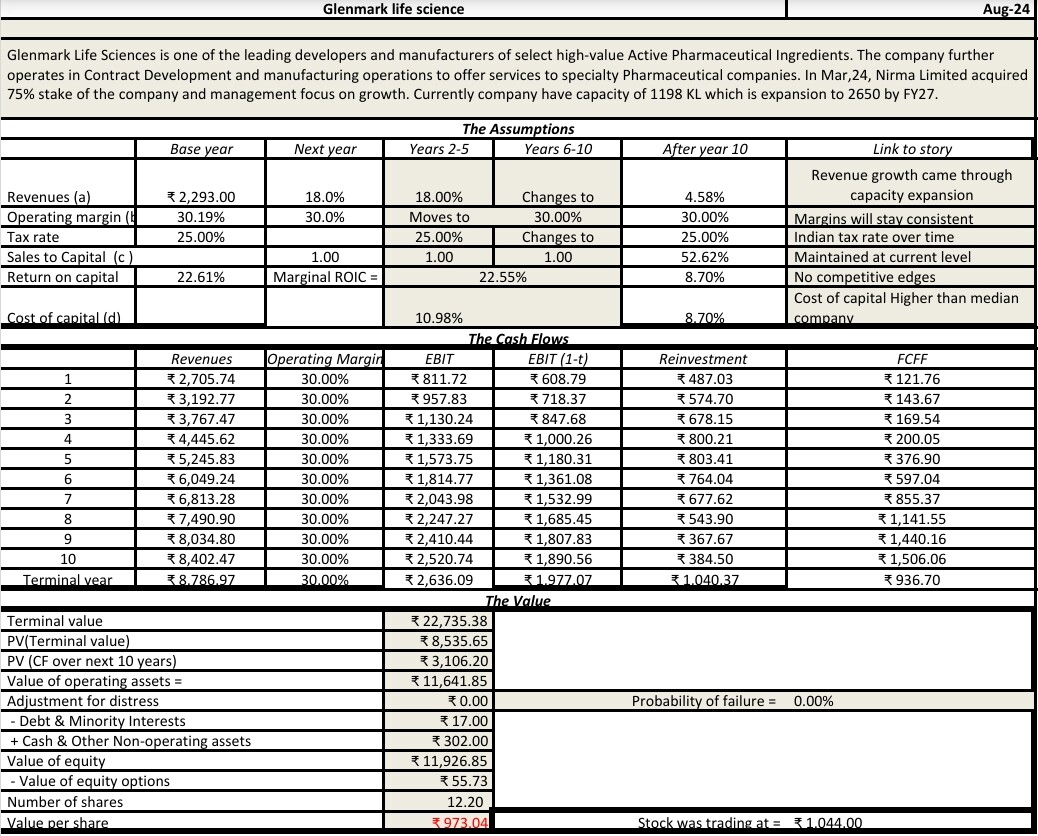

I try to value GLS with DCF.

Kindly give feedback.

Latest EV sales data and market share of players:

Electric 2W sales at 88,471 units in August rise 41% YoY | Autocar Professional

Ola’s market share is down, but still at 31%. In long term, seems like a safe guess would be 20-25% market share, as other players will definitely do some catch-up.

What increases Ola’s sales is the overall expanding EV market, which is up 41% YoY for the month of August.

I was doing some back calculation based on the management commentary. Following are the points, I have captured from the last earning call:

Free cash flow generation for the FY25 will be around 225-250cr

Cash equivalent as of fy24 was 262cr and at the end of fy25 should be 512cr.

EBITDA will be around 3.5x Net debt

Net Debt = Total debt – Cash and cash equivalent.

Net Debt as of q1 fy25 is 1862cr and at the end of fy25 should be around 1620cr. I am just deducting the anticipated cash flow of 250cr.

So, the EBITDA should be around Net Debt/3.5, i.e, 460cr

PAT= EBITDA(460cr) – Depreciation(120cr) – C G&A(14cr, 3-4% of EBITDA) – Interest cost(200cr)

PAT= 126cr

Cash flow = EBITDA(460cr) – C G&A(14cr, 3-4% of EBITDA) – Interest cost(200cr)

Cash flow = 246cr

This is precisely the cash flow number that management outlined in the last earning call; hence, this somewhat proves the fact that the EBITDA for fy25 should be 460cr.

The valuation of 21x is the bare minimum; from my understanding, as this is the average valuation of the last 12 months. Although, I believe over the next 2 years the valuation should re-rate and thereby match that of peers such as Chalet, whose valuation is 33x.

EV= 460×21=9660

Mcap = EV-NetDebt = 9660-1612 = 8048cr

77% upside from here, i.e, the share price could be around 366 from 207 as on today.

Disc: Invested and biased

Attended the AGM for 2023-24 held on Aug 31, 2024. My notes from the meeting are as follows:

There may be some mistakes in the above. You can directly go through the AGM proceedings from this link:

33rd Annual General Meeting of Ambuja Gujarat Exports Limited

Disclosure: Invested

Whilst I agree largely to what you’ve said, I see certain issues.

Company doesn’t seem to focus on the issues it has. Rather focus is bringing new sales. Ola E is often compared with Tesla. How both have build issues… But if we see the latest versions of Model Y, there is a significant improvement. I don’t see this attitude of improvement from Ola mgmt.

You’ve pointed out the OLA E has outperformed legacy 2W in EV sales. Imho, the first mover advantage is very slim in the 2W EV segment. Legacy makers will rush in with massive pockets and flood the market. So it’s only a matter of time, before we see Sales decline for OLA. As we witnessed for Tesla.

Mgmt team and leadership aren’t focusing on the right place. Marketing is not their role. Let the marketing team and leadership do that.

As for ICE being cannibalised… Let’s take a look at Ford F150.

The change was smooth. Not complete yet. I think it’ll be a balancing game. Net sales figures may not be amazing for these legacy companies. But revenue as a whole will increase at their standard pace. EV 2W will replace existing models in their own forte. Like- family focused ICE replaced by family focused EV.

Ola is a new entrant and disruptor in 2 wheeler mkt. There will be hiccups initially but how they navigate this teething period is important. So far it looks like they’re managing well. The problem with incumbent players is, their EV is cannibalising their own petrol 2 wheelers while Ola doesn’t have this problem and eating away everyone’s mkt share.

A little dated article showing Ola outselling the next 2 large players combined:

Hello @hitesh2710 sir,

Thank you so much for going through all the questions and answer them so patiently.

In one of your interview, you have mentioned one of the way to generate stock idea is to look for the recently listed companies in out of favor sectors.

Couple of names come to mind is India shelter (Finance) and Indegene (Pharma+IT) with good promotors and operating in industry with long runway.

Could you please suggest any other names that is on your radar?