Considering the date of the merger (Nov-Dec), there is a gap of 10-11% between IWEL and InoxWind.

As a strategy, can we switch more towards IWEL until the merger?

Maybe 75:25. Current allocation is 40:60 (IWEL:Inox)

Posts in category Value Pickr

INOX Wind (31-08-2024)

Ola Electric – Full Stack EV play? (31-08-2024)

Am trying to value OLA Electric, as Prof Aswath Damodaran says you can value any company by developing story.

1. The Story of OLA Electric

- Current Position : OLA Electric is currently a leader in the electric scooter (EV) market in India.

- Future Growth : It aims to expand leadership into the electric bike segment.

- Global Ambitions : Eventually, OLA plans to sell electric vehicles (EVs) globally.

- Battery Cell Advantage : While the revenue from battery cells is not directly considered, having an in-house battery cell supply could help OLA achieve higher margins due to cost savings.

2. Market Assumptions

- Two-Wheeler Market Size in India (2024) : 1.8 crore (18 million) units.

- Growth Rate of the Market : Expected to grow at 8% annually.

- Market Size in 2030 : With 8% annual growth, the total market is projected to be around 2.8 crore (28 million) units.

3. Electric Vehicle (EV) Penetration

- EV Market Share by 2030 : Projected at 40% of the total market, which is approximately 1.10 crore (11 million) EV units. Some industry reports predict an even higher market share.

4. OLA Electric’s Market Share Projections

- Domestic Market : Assuming OLA captures 33% of the EV market in India, this would equate to 36 lakh (3.6 million) units by 2030.

- Export Market : Assuming OLA captures 25% of the export market, this would be an additional 9 lakh (0.9 million) units.

- Total Sales Volume : Combining both, OLA’s total sales volume in 2030 would be 45 lakh (4.5 million) units.

5. Revenue Projections

- Average Selling Price : If the average price per unit is ₹1 lakh, the total revenue would be: 45 lakh units×₹1 lakh=₹45,000 crore

6. Profit Margin and Earnings

- Profit Margin Assumption : Assuming a profit margin of 10%, the profit would be: ₹45,000 crore×10%=₹4,500 crore

- Shares Outstanding : With 441 crore shares of OLA, the Earnings Per Share (EPS) would be: ₹10

7. Valuation and Price Prediction

- Price-to-Earnings (PE) Ratio : Assuming a PE ratio of 40 in 2030, the projected stock price would be: ₹10 EPS×40=₹400 vs CMP of ₹120.

Disc: Invested (as indicated in earlier post) and views are biased

Ranvir’s Portfolio (31-08-2024)

Sir what are your views on Premier energies valuation, if it list at around 800 and how do you see companies future growth?At what valuation should we look at this company as it is backward integrated and largest solar cell exporter of India and also planned for a capex.Solar is a sunrise sector and looking at our country’s power need going forward due to data Centres, EV , IOT etc.i think this is a sector worth investing.How do you think of this sector?

Availability of Solar is really good in India ( We have geographical advantage) and due to advanced efficiency tech. like- Topcon playing imp role in reduce solar cost.

Secular growth stocks & my portfolio (31-08-2024)

Should remove the absolute values for your own privacy. Just share the % allocation, etc. Don’t add your actual values in positions.

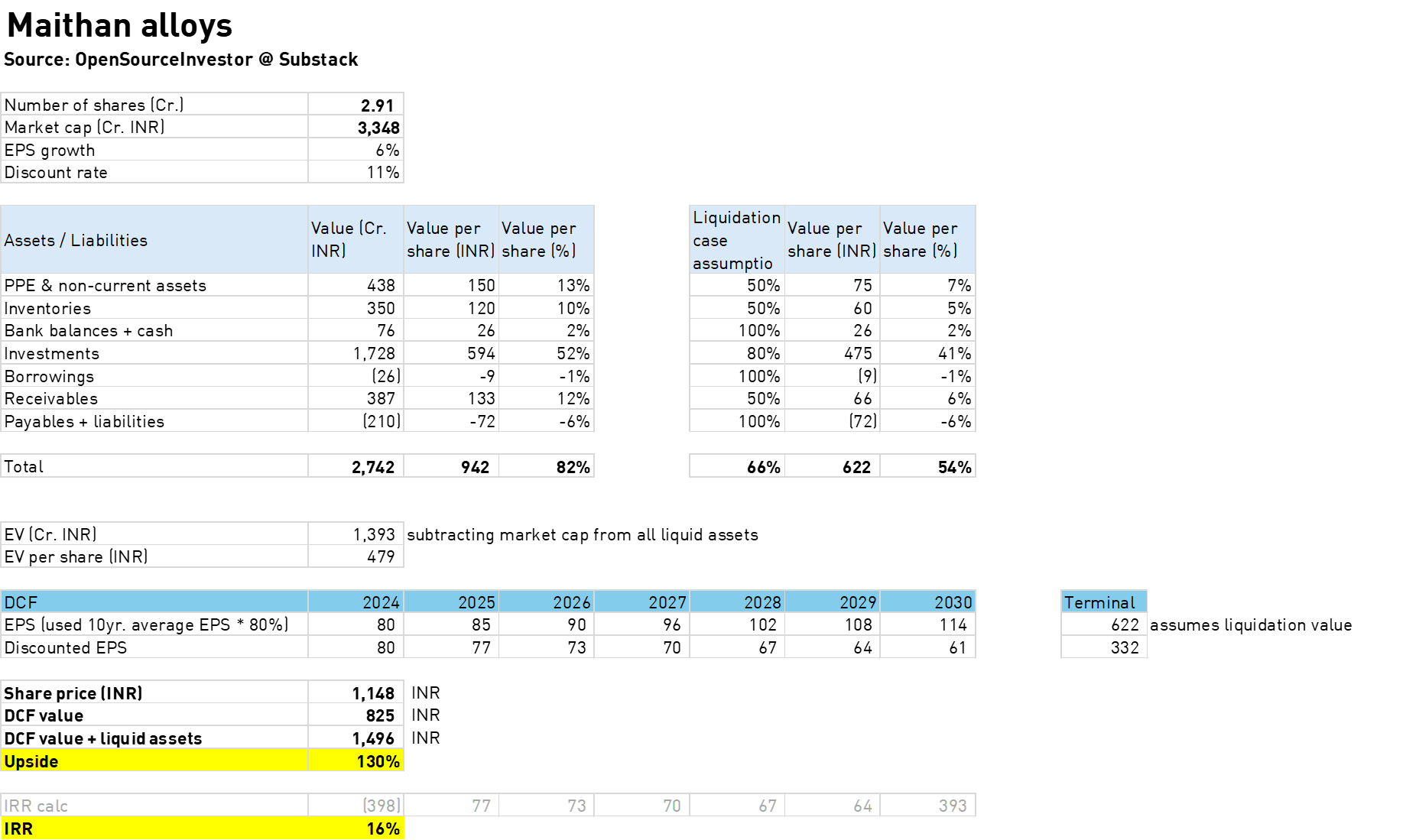

Maithan Alloys Ltd (31-08-2024)

I just had a look at Maithan Alloy’s current valuation and it looks interesting. But I have a similiar doubt to Mayank’s post above – the company seems to have completely shifted strategies to become an equity holding company, mainly investing excess cash in PSU stocks. Also their disclosure is pretty poor – their latest Q1 2024/25 quarterly report doesn’t even have a balance sheet (the most basic of financial statements!). So, will wait and watch until the annual report is released. Hopefully will be clearer then.

For now, I’ve based the below calculations on Q4 2023 quarterly report. If I use conservative estimates, the stock should provide ~16% IRR at these levels. However, I will wait for disclosures on the latest balance sheet and equity holdings before deciding to invest further.

Disc: invested; potentially biased

Cheers,

Sharad

OpenSourceInvestor

APL Apollo Tubes (31-08-2024)

APL has created significant wealth, i have personally benefited from it, imo, and whenever there are cyclical downturn or some issue with growth in business these thoughts do come in, but i feel the mgmt is competent and has created a strong business in an otherwise lacklustre sector. We should give it few qtrs to start delivering on what it has promised.

Globus Spirits (31-08-2024)

[Reason for yesterday’s jump. ] (https://indianexpress.com/article/india/ethanol-distilleries-can-buy-23-lakh-mt-rice-from-fci-govt-9540644/)

They can shift to rice from maize in a day! (but i dont think they will)

but Gain of around 5/- kg comparing Q1 Pur rate of rice.

Disc: Invested

Ola Electric – Full Stack EV play? (31-08-2024)

Yadea is world’s largest 2-Wheeler EV co from China, it has 28% market share globally and sells 60 million units in 80 countries. Globally top 5 2-W EV’s, all are from China. (Blame Bajaj, TVS for being too conservative).

Anyway, if we compare it with Indian EV

Y’s top model E8S 200 has max speed 65 km/h vs 116 km/h of ola

Driving range 150 km of Y vs 170 ola

Y started in 2001.

It’s difficult to find more info on tech spec of Yadea’s various mode, request @SA24 and others interested to colloborate to find some more data. Thx

Multi-themed Long Term Portfolio (31-08-2024)

(3/3)

-

Borosil Renewables: Biggest solar glass manufacturer outside China, stands to benefit if China’s dumping is stopped in India/US/EU.

-

Netweb Technologies: India’s only company having exp. in setting up supercomputers. Has massive opportunity in creating infra for upcoming AI wave.

-

RIR Power Electronics: Setting up new-tech SiC plant in Odhisa with state incentives, diversifying to provide solutions to various industries.

-

RPSG Ventures: Holding co of Firstsource Solutions IT company, owns “Too Yumm” brand, also owner of IPL team LSG and ISL team ATK MB, owns a luxury mall in Kolkata. Massively undervalued at the time of writing.

-

Shivalik Bimetals: Creates shunt resistors, which go in EV chargers, smart meters, basically every upcoming sector. See SOIC’s YT video on this stock for better understanding.

-

Tube Investments: Has presence in commercial EVs through TI Mobility. It’s subsidiary CG Power doing extremely good, also setting up Semiconductor fab.

-

NIBE Ltd: Recent player in defence sector, seems to have some political links, hence getting major orders without prior expertise. Has set up a new SOTA facility inaugurated by Naval chief. Should have good runway for future since currently only a small-cap.

Multi-Disciplinary Reading – Book Reviews (31-08-2024)

Recently finished What It Takes by Stephen Schwarzman, founder of Blackstone, one of the largest alternate investment management company in the world. Was always fascinated by the shear size of the company and their share in grade A retail real estate in India.

The book is an easy and enjoyable read, and I highly value biographies like this one. It reminds me of Phil Knight’s work, where the narrative flows effortlessly despite the surrounding noise, as if the universe itself is conspiring to help the author achieve their intended goals. For obvious reasons of the subject being finance, there has to be an other side to the story, on how his colleagues or competitors saw him throughout his life and would love to read King of Capital to understand that sometime.

Here are some excerpts from the book that I noted down:

- “There is a saying in finance that time wounds all deals. The longer you wait, the more nasty surprises can hurt you. I like to finish work quickly. Even if tasks are not urgent, I like to get them done to avoid the unnecessary risks of delay.

- “To be successful you have to put yourself in situations and places you have no right being in. You shake your head and learn from your own stupidity. But through sheer will, you wear the world down, and it gives you what you want

- “Everyone contributes to the discussion. Risk is systematically broken down and understood. Debate is full and robust. The same small groups of people, who know each other well, go over each investment applying the same rigorous standards. This unified approach to investing has become the backbone of the Blackstone way.”

- “The first was focus. If you ever felt overwhelmed by work, I said, pass on some of your work to others. It might not feel natural. High achievers tend to want to volunteer for more responsibility, not give up some of what they have taken on. But all that anyone higher up in the firm cares about is that the work is done well. There is nothing heroic or commendable about taking on too much and then screwing it up.”

- “The second way to maximize your chances of achieving excellence was to ask for help when needed”

- “The rewards of having a beautiful space that attracted the best people and gave our clients greater confidence in our abilities would far exceed the cost of paying a little extra to close the deal.

- “And the best way to get what you want is to figure out what’s on the mind of the person who can give it to you. ”

- “If you are going to start a business, I told them, I believe it has to pass three basic tests. First, your idea has to be big enough to justify devoting your life to it. Make sure it has the potential to be huge. Second, it should be unique. When people see what you are offering, they should say to themselves, “My gosh, I need this. I’ve been waiting for this. This really appeals to me.” Without that “aha!” you are wasting your time. Third, your timing must be right. The world actually doesn’t like pioneers, so if you are too early, your risk of failure is high. The market you are targeting should be lifting off with enough momentum to help make you successful.”

On to the next one which is The World for Sale