Posts in category Value Pickr

Sharda Motors – Emission tailwinds or EV threat to exhaust systems? (30-08-2024)

Also the promoter holding in last quarter went down by more than 8%. Was there any reason shared by them? Not that they are obligated to.

The Anti-Portfolio (30-08-2024)

@vikas_sinha sorry for too many messages, wouldn’t post further as purpose of thread need to be maintained, please share your views on India glycol, after todays announcement and upcoming expansions, valuations looks lucrative.

RACL Geartech Limited (30-08-2024)

Not geopolitical issue, but weak consumer sentiment in West and high inventory of automobiles lying at dealers.

Piccadily Agro Industries Ltd (30-08-2024)

Piccadily Agro Industries Limited Gets Pan India Approval to Supply Its Marquee Brands

In Paramilitary (Central Armed Police Forces) Canteens

Indigrid InvIT: High yield on stable and predictable revenues (30-08-2024)

Thank you for sharing this… can you also add the yearly dividend each of these gave in the last FY for in a column?

Thanks

Goldiam International : A rare shareholder friendly and debt free Jewelry company (30-08-2024)

In contrast to various articles indicating correction in LGD prices , Goldiam management during Q1 concall has indicated that LGD price correction has stabilized and whatever news articles coming on correction in LGD prices are outdated. Management was confident about export business growth of 15-20% for FY.

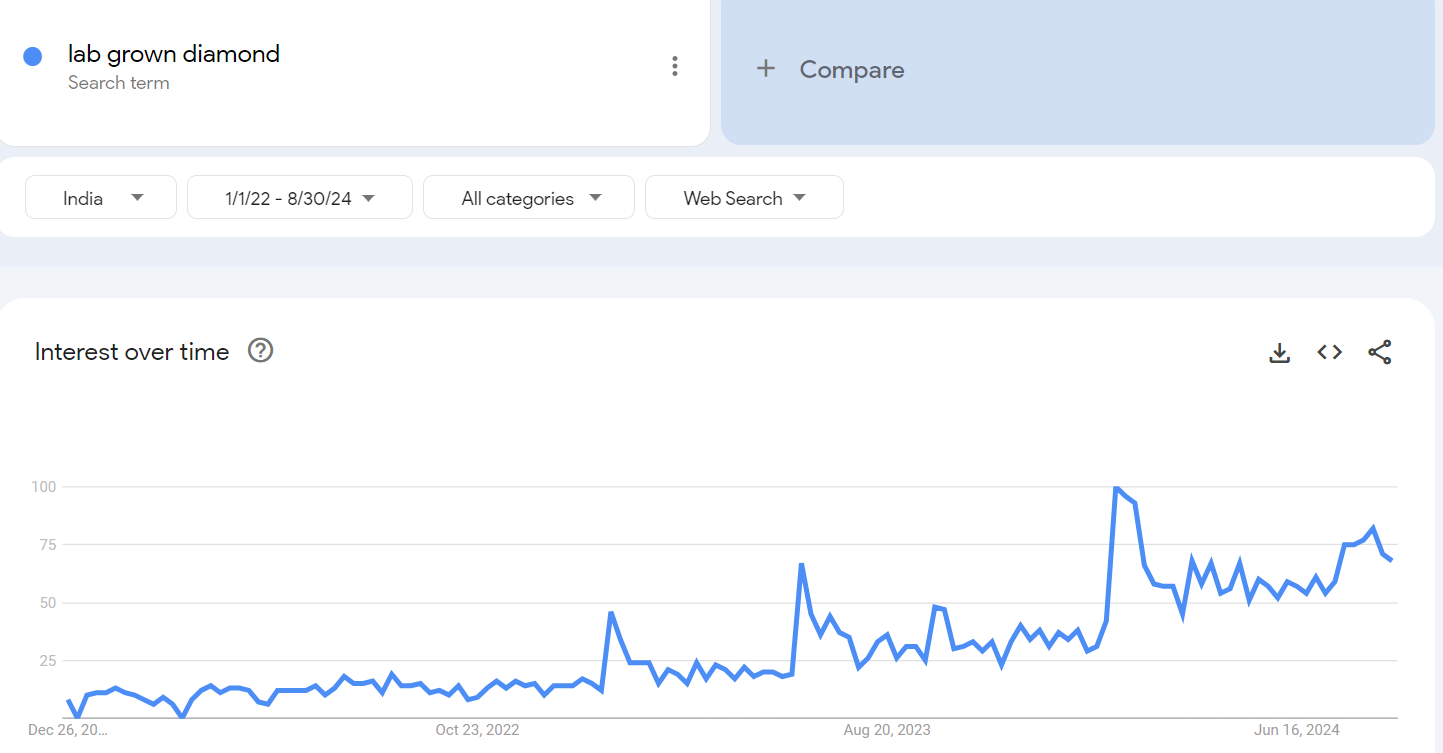

Goldiam also launching their own retail LGD business in India by brand “ORIGEM”. How this will pan out for them need to be seen. While LGD jewellery is well accepted among US customers, it may be early days in India. Google trends for the past 3 yrs does show that the trend for LGD in india is increasing as shown below:

Concall notes:

Q1 revenue increased by 40% and EBITDA margins at 20% grew by 43% yoy to 34Cr.

Share of lab grown diamonds increased to 68% of revenue.

Several production operations of LGD were shut and prices have stabilized. All articles coming on price correction are outdated and there is no hit on inventory like last year.

Current order book stands at 180Cr.

Most of our jewelry sales are done on a cost plus model which includes metal(gold), stone (natural or LGD) and labor.

Based on service capability, in house manufacturing, availability of style and design bank available with Goldiam should help to sustain higher margins profile in LGD.

Deep distribution ties with customers is a significant differentiating factor in this business. Entire business is built by improving designs and deeper penetration with US retailers.

Most of the LGD exported by Goldiam are of two carats or below.

There is significant headroom available for Goldiam to increase their share of revenue with US customers.

India B2C business:

Brand name “ORIGEM”.

Plan is to open 3-5 stores in Q3FY25 and goal is to become the largest organized retailer of LGD in India.

Target to open 15 to stores in metro + regions and follow omni channel strategy.

During the first phase all stores will be on the COCO model.

Targeting modern day customers shopping for occasions and daily wear.

B2C will have higher gross margins but there will be higher operating cost in the beginning.

Total capex per store will be around 4cr. ( inventory of 3cr, store deposit of 50 lac and store fit out cost of 5o lac).

Breakeven on per store basis will be at 30 lac/month.

Funding for the B2C will be from cash on books( has 300cr) and partly from gold metal financing.

Discl: Invested recently(3%)

IRCTC: a necessity, a monopoly (30-08-2024)

I would tend to agree with you. Stock Price seems to be factoring in all good things at current CMP of 930 and P/E of 60+.

If GOI imposes any new policy restrictions in terms of convenience fee reduction, private players to participate in Online ticketing etc. then whether this premium valuation remains is the key concern.

Stock is on my watch list.

Caplin Point Laboratories (30-08-2024)

Marcellus exited from Caplin in March 2021. Now they again seem to show intrest in it.